Deducting Business Expenses – Which Expenses are Tax deductible?

Tax filing season is here. As an owner of a startup or small business, what types of business costs or expenses are allowed or are considered tax deductible? I get asked the question by my clients “can I deduct that as a business expense on my taxes?” In this blog post, I would like to go over some of the rules to think about for determining which expenses are legitimate write-offs. The IRS states “to be deductible, a business expense must be both ordinary and necessary. An ordinary expense is one that is common and accepted in your trade or business. A necessary expense is one that is helpful and appropriate for your trade or business. An expense does not have to be indispensable to be considered necessary.” So if you notice the wording that the IRS emphasizes about what makes a business expense eligible for being deductible, the two words “ordinary” and “necessary” seem to be pretty important.

Tax filing season is here. As an owner of a startup or small business, what types of business costs or expenses are allowed or are considered tax deductible? I get asked the question by my clients “can I deduct that as a business expense on my taxes?” In this blog post, I would like to go over some of the rules to think about for determining which expenses are legitimate write-offs. The IRS states “to be deductible, a business expense must be both ordinary and necessary. An ordinary expense is one that is common and accepted in your trade or business. A necessary expense is one that is helpful and appropriate for your trade or business. An expense does not have to be indispensable to be considered necessary.” So if you notice the wording that the IRS emphasizes about what makes a business expense eligible for being deductible, the two words “ordinary” and “necessary” seem to be pretty important.

Expenses Must be Ordinary & Necessary

When the word “ordinary” is used, it is referring to what would be considered a normal expense that a business would take in a particular profession or industry. Some deductions such as software, insurance, office equipment, computers and supplies would be considered ordinary expenses. Ridesharing platform drivers such as Lyft or Uber drivers (who are not actual employees and considered self-employed for tax filing purposes) would take the standard IRS mileage deduction, commissions paid, vehicle maintenance, tolls and parking fee deductions. This Forbes columnist, Brian Thompson, mentions that an exotic dancer or adult entertainment actresses may be able to deduct the expense of getting breast implants, where someone working as a real estate broker would most likely not be able to. The second part of IRS tax code language definition “necessary” of business expenses. What they are referring to are expenses that are “appropriate” and “useful” for business or trade. Normally when you think of the word necessary you might associate to mean required or imperative. The expense needs to be helpful.

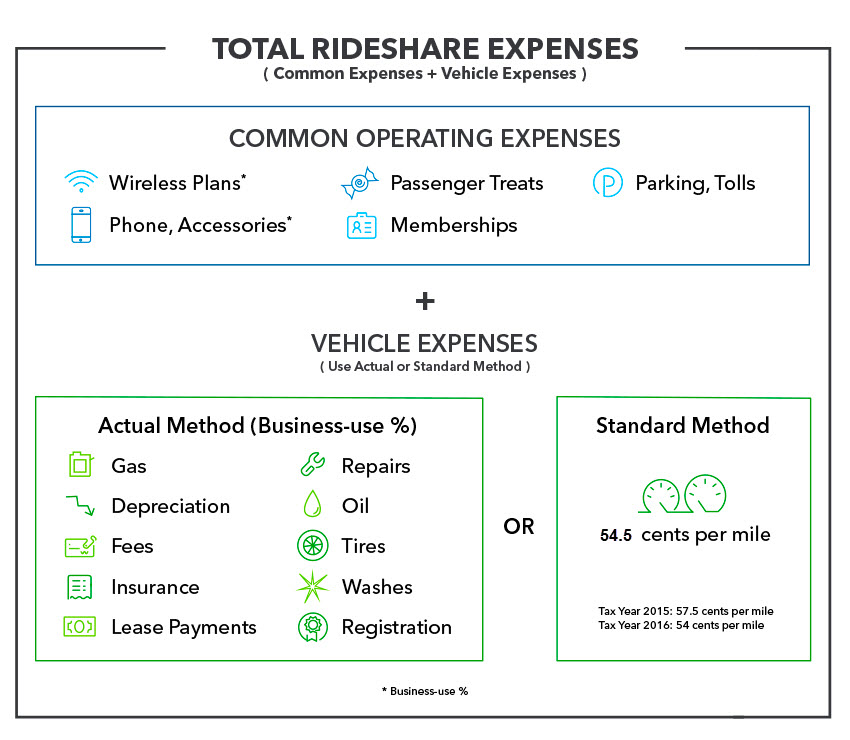

Image credit Turbo Tax

Image credit Turbo Tax

Common Self-Employed Business Expenses

There are several common tax deductible small business expenses that are not specific to one type of industry in particular.

Business Travel

The IRS allows you to be able to deduct expenses for traveling away from your “tax home” for business. What they mean is where is your place of business mostly conducted from? Do you work from an office, out of a coworking space, or do you have a home office? Flying to Costa Rica to meet with a resort owner to take professional photos and develop their website may be considered business travel.

If you need to travel for work you may be able to deduct airfare, train tickets, taxi, Uber or Lyft expenses, as part of a business trip. IRS Publication 463 has more details, but the expenses can also include baggage claim fees, hotel lodging and some meals. Check with your CPA more about what is your “tax home” to be safe.

Car and Truck Expenses

If you drive to your office each day, the daily or ordinary commuting mileage to and from your home to the workplace are not allowed to be deducted. Although as mentioned earlier for the Uber driver you can deduct vehicle expenses (gas, repairs, upkeep/ maintenance); or just take what is known as the standard mileage deduction, which is based on the miles that you drive (58 cents/mile for 2019). Other expenses can include tolls, rental cars and parking fees for business travel such as going to a client’s office for a meeting. There are caveats to deciding which one to take, contact a tax professional for more details.

If you drive to your office each day, the daily or ordinary commuting mileage to and from your home to the workplace are not allowed to be deducted. Although as mentioned earlier for the Uber driver you can deduct vehicle expenses (gas, repairs, upkeep/ maintenance); or just take what is known as the standard mileage deduction, which is based on the miles that you drive (58 cents/mile for 2019). Other expenses can include tolls, rental cars and parking fees for business travel such as going to a client’s office for a meeting. There are caveats to deciding which one to take, contact a tax professional for more details.

If you are a security intercom installer or a self-employed contractor then most likely you use a vehicle, such as a truck, pickup or van for business usage. Keep records.

Office Space Rental Expenses

The cost of renting space for your business, an office, coworking space, retail storefront, or factory is an ordinary and necessary expense which is fully deductible.

Office or Business Supplies Expenses

Save your receipts for software, pencils, paper, tissue etc. You can deduct any of these supplies from your bottom line. The cost of items used in a business (power tools for a contractor) and you can also opt for using the de minimis safe harbor election for you to deduct the cost of tangible property (ie computers, office furniture) if they are under $2,500 rather than depreciating them. Then the items are treated as non-incidental materials and supplies. They are deductible expenses when bought or furnished to clients.

Depreciation

This deduction is an allowance for the cost of buying property for your business. It includes the Section 179 deduction for equipment purchases up to a dollar limit ($1,000,000 million in 2018; $1,020,000 in 2019). Certain other limits also apply. The depreciation category also includes a bonus depreciation allowance, which is another type of write-off in the year costs are paid or incurred. The limit is 100% for property acquired and placed in service after September 27, 2017. Barbara Weltman wrote a good list in Small Business trends.

Employee and Contractor Labor Pay

Paying W-2 employees, which can include salaries, wages, bonuses, commissions, and taxable fringe benefits, are deductible business  expenses for the business. Many small businesses will hire freelancers, sub or independent contractors to help grow their startup venture. The cost of such contract labor is deductible. Be sure to issue Form 1099-MISC to any such contractor you pay more than $600 in a year (if payment is made to the contractor via credit card or PayPal, it’s up to the processor to issue them the Form 1099-K, but you may want to send your own 1099-MISC for personal protection). If you have LLC entity then payments to partners and other LLC members are not wages and are not deductible (they are owners).

expenses for the business. Many small businesses will hire freelancers, sub or independent contractors to help grow their startup venture. The cost of such contract labor is deductible. Be sure to issue Form 1099-MISC to any such contractor you pay more than $600 in a year (if payment is made to the contractor via credit card or PayPal, it’s up to the processor to issue them the Form 1099-K, but you may want to send your own 1099-MISC for personal protection). If you have LLC entity then payments to partners and other LLC members are not wages and are not deductible (they are owners).

Loan Interest and Fees

If you borrowed money or took out a loan to start or fund your business, (a line of credit used in a construction business as an example) then any fees or interest paid on that is deductible. One rule is your loan must be a legitimate loan from a legitimate lender. You cannot borrow money from friends that you may or may not fully repay and deduct your interest payments to them. For 2018, businesses with average annual gross receipts in the three prior years of more than $25 million ($26 million in 2019) are limited in the percentage of interest that’s deductible. If you take out a loan to purchase a business or a percentage of it, then it is treated differently. You must differentiate business interest from an owner’s investment interest or passive activity interest, which is not a business deduction. A Forbes contributor Jared Hecht mentions “If you want to buy another business but don’t expect to actively run it, that’s considered an investment, not a business expense, so the loan is not deductible.” Speak to tax professional about specific situations.

Insurance

Insurance used specifically for your business such as liability, employee insurance, workers comp, E&O insurance are deductible business expenses. What is not deductible would be getting disability insurance for lost income, the IRS would consider that a personal expense.

These are a few examples of standard or common business expenses, of course, there are many other ones. The IRS 1040 Schedule C the 18 page instructions pdf can give you a better idea of what you can deduct and what is not allowed.

Business Expense Cautions or Things to Watch out For

So most of this article has talked about fairly obvious and straightforward deductions for taking business expenses. Here are a couple of areas to be careful of.

Taking Large Expenses

While the tax code itself contains no “too big” limitation, courts have ruled that it is inherent in Section 162. As an example, it could be reasonable for a large apparel company such as Under Armour or Lululemon to purchase or lease a private Jet to travel frequently to its different clothing manufacturing plants. The recent tax reform bonus depreciation allows for businesses to purchase a private jet to deduct 100% of the plane’s cost immediately. If you are hot startup such as Theranos was until the scandals, this might have been ordinary and necessary for the CEO to travel with. But a regular restaurant owner who wants to fly to Florida to meet with their Avocado supplier probably not.

“Hobby Loss Rules” You Must Own a Business

It may sound like I am joking but some people try to take business expenses without having a business. Forbes Columnist Anthony Nitti wrote a post about “The Top Tax Court Cases of 2018: Reunited With The Hobby Loss Rules And It Feels So Good” after he saw description about the misleading write off benefits of “becoming a Beachbody coach” in a forum. He mentions the “hobby loss” rules, found in Section 183, As many side hustlers, fitness coaches or consultants may end up finding out that, sometimes the IRS may view certain activities that are not entered into “with the intent of making a profit.” and if this happens then the activity is a hobby rather than a business. So before the tax reform the hobby expense was itemized as “miscellaneous itemized deductions on Schedule A” but if you are categorized as a hobby now, the TCJA eliminated “other miscellaneous itemized deductions.” So as Brian Thompson points out the IRS looks at many factors such as:

- Do you put in the necessary time and effort to turn a profit?

- Do you have the necessary knowledge to succeed in this field?

- Do you depend on income from this activity?

- Have you made a profit in this activity in the past, or can you expect to make one in the future? (has not made a profit for 3 of the last 5 years etc)

Mixing Personal Expenses with Business Expenses

The IRS wants you to understand that you can’t deduct any type of personal expense even if you own a business. Personal expenses could be anything categorized under living, personal or family. These are considered personal and are not deductible as a business expense, for example, premiums for any life or disability insurance. And if you do have an expense, that could be mixed such as travel or perhaps home office utilities, the IRS rule is for you to divide the costs between both. So everybody uses their cell for business and personal use, if you use it for work during the week you can split it up as 70 business use, 30 personal use.

Capital Expenses Cannot Be deducted all at Once

Capital expenses such as the purchase of long-term capital assets, like vehicles, machinery and equipment, When you invest in your business, and you buy office furniture, new computers, land, buildings and other large items. As you are making a long term investment to cover startup costs and improvements to your facility, these costs can be depreciated (extended over the life of the asset), but they can’t be deducted in one year. Since you will probably be using them for more than one year as well, the IRS asks you to spread your deduction for them over multiple years as well.

The Laugh Test

Frederick W. Daily of Nolo mentions ”tax professionals frequently rely on the so-called laugh test: Can you put down an expense for business without laughing about putting one over on the IRS?” He went on to mention an example. “Henry, an accountant, deducted his yacht expenses, contending that because the boat flew a pennant with the numbers “1040,” it brought him professional recognition and clients. The matter ended up before the tax court. The court ruled that the yacht wasn’t a normal business expense for a tax professional, and so it wasn’t ordinary or necessary.” In short, the yacht expense was personal and thus nondeductible. (Henry v. CIR, 36 TC 879 (1961).) In the example above, the tax court laughed the accountant and his yacht out of court.”

Conclusion

I hope you’ve found our small business expense tax deduction guide helpful. As always, it’s best to make sure to learn the fundamentals and then seek out trusted CPA advisors to help you navigate the details. The TCJA includes and enacts substantial changes to the U.S. tax system- such unprecedented changes have not been seen since 1986. Contact our office and receive the help you require to obtain answers to questions so your business can operate faster, smoother and more efficiently. Contact us for a free consultation.

{kind=link}