new research finds that tax-cuts for bottom 90 percent of earners boosts job growth

A fascinating new study recently reported on by Economic Research Reporter Clark Merrefield from Harvard Kennedy School’s Journalists Resource, discovered that job creation and employment increases when taxes are cut for the bottom 90% of income earners. This finding is contrary to popular supply-side economics theories of the past 35 or 40 years.

A fascinating new study recently reported on by Economic Research Reporter Clark Merrefield from Harvard Kennedy School’s Journalists Resource, discovered that job creation and employment increases when taxes are cut for the bottom 90% of income earners. This finding is contrary to popular supply-side economics theories of the past 35 or 40 years.

A Princeton University economist Owen Zidar has written an investigative paper titled “Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth and Employment” in the Journal of Political Economy looking at economic data from the 1980s through the 2000s.

Since the days of Reagan, the Republican political argument in favor of cutting regulations and income taxes on large corporations, entrepreneurs and wealthy investors all hinges on the idea that they are real drivers of economic growth. It assumes that they will invest the extra cash from tax savings into expanding their businesses, buying new factories, upgrading equipment, technologies, operations and hiring more workers to create new jobs. And that all of this expansion will trickle down to workers, of which employees will then spend their wages that drives consumer demand for goods and economic activities.

(Image credit: Investopedia)

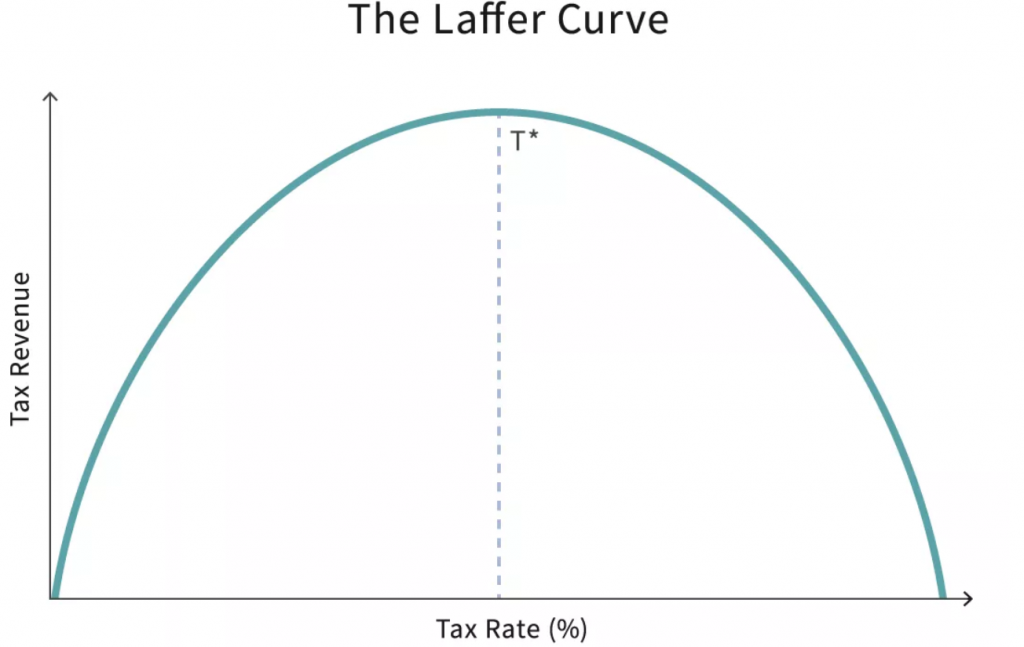

American economist Arthur Laffer, an advisor to the Reagan administration, developed a bell-curve style analysis called the “Laffer Curve” that studied the relationship between tax rates and total Government tax revenue. Investopedia states that “Laffer’s idea that tax cuts could boost growth and tax revenue was quickly labeled “trickle-down.” This so-called “trickle-down economics”, or “trickle-down theory,” is based on two assumptions: All members of society benefit from growth, and growth is most likely to come from those with the resources and skills to increase productive output. The author Clark Merrefield describes a more literal analogy of an “image of water moving from high to low ground, unable to fight the irresistible force of gravity, saturating one and all.” Princeton University economist Owen Zidar research paper combines past academic analyses and new real-world experiments to challenge the idea that tax cuts work anything like waterfalls.

The employment effects of tax cuts for different bracket income earners

Clark Merrefield points out that the “trickle-down” selling points (it’s so good for the economy, that it will boost growth and offset any losses from the cuts) were used by the Trump administration. In November, 11 2017, former White House economic advisor Gary Cohen made the case for the Trump tax reform TCJA, speaking with CNBC:

“When you take a corporate tax rate at 35 percent and move it to 20 percent, and you see what’s happened over the last two decades to businesses migrating out of the United States, migrating profits out of the United States, migrating domicile out of the United States, and hiring workers out of the United States, it’s hard for me to not imagine that they’re not going to bring businesses back to the United States. We create wage inflation, which means the workers get paid more; the workers have more disposable income, the workers spend more. And we see the whole trickle-down through the economy, and that’s good for the economy.”

Mr. Zidar found in his research that job growth is actually more likely to come when Congress cuts taxes for people earning a living somewhere below the high earner income tax brackets. .

“In fact, the positive relationship between tax cuts and employment growth is largely driven by tax cuts for lower-income groups and the effect of tax cuts for the top 10 percent on employment growth is small,” Zidar wrote in his research paper that was published in June 2019.

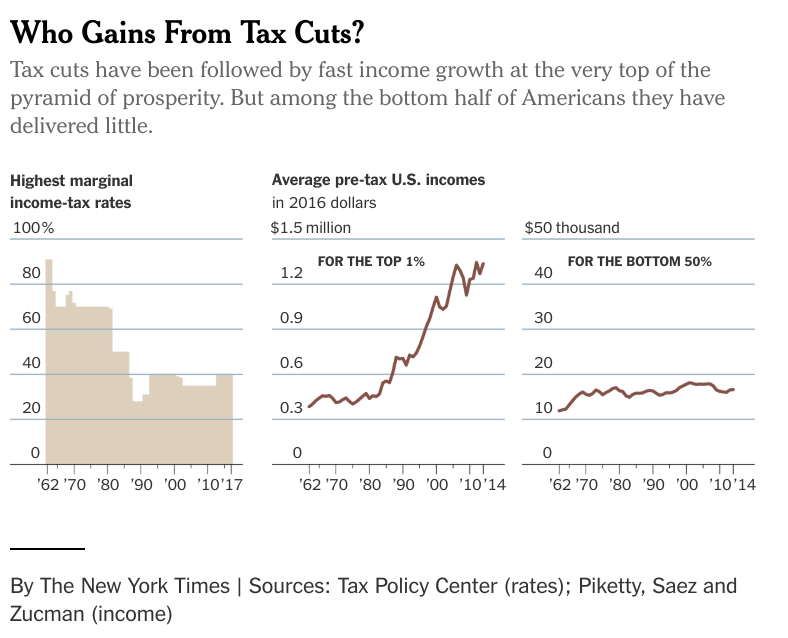

According to statistical tax data from the Tax Policy center, the biggest Federal tax cuts went to top marginal tax income earners during the 1980s and in the 2000s, while taxes increased for the middle class, and decreased for lower-income earners during the 1990s. In his paper, Mr. Zidar examined tax data from 1980 to 2007, and made use of variations across a number of different states (not all states have the same median income numbers) to explore how tax rate changes to different groups of income earners actually affect employment outcomes.

His data findings uncovered that a tax cut equal to 1% of a state’s GDP for the bottom 90% of income earners resulted in 3.4 percentage points’ growth in the number of people employed in the state for the next 2 years. And on the opposite income spectrum, almost no change was found in employment growth increases for the equivalent tax cut for the top 10% income earners.

Author Clark Merrefield referenced an example from Zidar’s research analysis “say a state has an annual GDP of about $100 billion — roughly the size of New Mexico’s economy. A tax cut totaling $1 billion is enacted favoring the bottom 90% of earners. Two years later, the state would expect to see job growth in the range of 3.4 percentage points compared with the year before the tax cut.”

Princeton Professor Zidar told him in an email “If cuts at the bottom encourage more people to work — since working is now more beneficial — economic activity will be higher.” He further went on to say “If cuts at the bottom are spent at a higher rate, then demand for goods and services throughout the economy will increase more and generate more activity. This higher activity can also stimulate more investment.”

Zidar’s research paper noted that a tax increase that equaled out 1% of a state’s GDP on the bottom 90% of income earners reduced labor force participation by 3.5 percentage points and hours by 2%. And the same 1% tax increase on the top 10% earners did not affect those numbers.

He also found that a tax increase equal to 1% of a state’s GDP on the bottom 90% of income earners reduced labor force participation by 3.5 percentage points and hours by 2%. The same tax increase on the top 10% didn’t affect those numbers.

For his paper, he did not include the tax reform changes of the 2017 TCJA, but he did mention that labor force and employment fluctuations could have had different outcomes if the tax rate changes from the 80s up till now had been more substantial.

He uses an analogy of saying it’s hard to know what will happen in outcomes after a category 5 hurricane, if you have only gone thru a category 1 or 2. Meaning, “It might be the same, but sometimes there are fundamental differences in responses based on the size of the shock.

It’s Zidar’s opinion that there is no economic data or evidence to support the theory that “trickle-down economics” works for the benefit of society the way some people claim it does.

(Image credit: The Balance )

(Image credit: The Balance )

What are the returns from the Trump Tax Reform law of 2017?

Zidar mentions that President Trump praised the trickle down theme after Congress and he signed and passed into the Tax Cuts and Jobs Act, which reduced taxes and many economists believed it benefited corporations and business owners more than individual salaried workers.

Trump said during a speech at the Sheffer Corporation back in February of 2018 about the reform, “when I signed the tax cuts six weeks ago, it set off a tidal wave of good news that continues to grow every single day,” He also went on to preemptively say “before the ink was dry, companies were announcing thousands and thousands of new jobs and enormous investments to their workers.”

Now, currently the US still has pretty low unemployment rate, but a large aspect of the Trump administrations argument for passing the TCJA tax reform was going to spur large corporations who had moved offices overseas to suddenly bring money back in a major way. Unfortunately, private reinvestment into new jobs and factories has not gone been as robust as it was predicted to be, according to a paper titled “U.S. Investment Since the Tax Cuts and Jobs Act of 2017” published by economist authors in the International Monetary Fund. News publication Axios reported that the companies that did bring their profits back to the US — the 2017 bill reduced repatriation taxes (a tax holiday on trapped profits) — used it more for stock buybacks instead of capital expenditures.

In a New York Times article titled “Trump’s Push to Bring Back Jobs to U.S. Shows Limited Results” reported that Trump’s claim that “those selling shares will soon invest their proceeds from the buybacks into start-ups, business expansions or other forms of economic activity.” According to NYT’s article, data shows that those tax law changes have encouraged multinational companies to shift hundreds of billions of dollars in profits to their American operations, essentially for accounting purposes, through a process known as repatriation. Brad Setser, a senior fellow at the Council on Foreign Relations stated that flow of money “doesn’t mean all that much,” Mr. Setser said. “You’re not in any way seeing a shift in real activity back to the United States.” The CFR tracks international investment flows, of which he mentioned that relatively few pharmaceutical companies were moving plants and activity back to the United States from countries like Ireland or Switzerland. Pharmaceutical imports from those countries actually rose in 2018, he noted. So it remains to be seen if more companies will really bring back and open new operations that lead to substantial job growth.

The author Clark Merrefield mentioned that the second quarter of 2019, according to recent data from U.S. Bureau of Economic Analysis, shows a deceleration in real GDP in the second quarter primarily reflected downturns in inventory investment, exports, and nonresidential fixed investment. This can be translated that companies were potentially expecting to have fewer customers, so they are holding less goods and raw materials in stock. A senior fellow of the Urban-Brookings Tax Policy Center, named Steve Ronsenthal, examined retirement and tax data before the TCJA of 2017 was passed, and he made a comment about the lower repatriation tax relief (one-time 15.5 percent tax rate on liquid assets (and 8 percent on illiquid assets) of US-based companies foreign profits coming back. He stated, that \ “would mostly benefit high-income U.S. taxpayers and foreigners, not U.S. workers.” The Tax Policy Center is considered to be a bipartisan think tank that analyzes tax law policy.

According to a report called “Tax Reform Made Me Do It! ”, published in the Tax Policy and the Economy Journal, they had analyzed the first-quarter 2018 earnings conference calls from 424 companies listed on the S&P 500 index to examine how the companies said they were going to spend the extra cash they were going to save in the 2017 tax cut reform. They found that:

- Only 22% said they were going to increase investment of any kind because of the TCJA legislation

- Around 4% of firms said they would pass tax savings down to their workers

- And only 2% attributed their share repurchase plans to the TCJA reform bill

They also mentioned in a regression analysis that the companies who expected a larger expected-tax-savings from the corporate rate cut were the ones most likely “to announce payments to workers and plans to increase investment.” The authors also noted that “companies with a Political Action Committee that donates more to Republican candidates are also more likely to announce benefits to employees.”

Data and research on trickle-down tax policy on the economy

The author Clark Merrefield examines a wide range of data and research looking back several decades and seems to come to the conclusion that trickle-down economic policies usually end up benefiting the upper echelon of top income earners more than middle-class wage earners. If we take a look at the tax cuts that President Ronald Reagan passed in 1981 as well in 1986, income tax rates in general have been dropping for the past few decades, (which most people who say is a good thing), and it did contribute to boosting GDP growth to 3.5 percent (along with the Fed’s interest rate cuts) in the short run of his two terms, but also played a role according to the NYT in escalating income growth inequality by the 1% and the middle class over the long term. If you look at what happened to workers who fall into the bottom half of the tax income brackets, they ended up making less in real dollars towards the end of Reagan’s second term then they were at the beginning of the 80s.

In the 1994 Lynn A. Karoly, a professor and senior economist at Rand Corporation contributed to a research paper titled “Tax Progressivity and Income Inequality,” which found that more than 2⁄3 of the rising overall income inequality from the post-war low in 1968 to 1989 occured during the 1980s. In July 2018, a professor named Jennifer Luchs-Nunez published a research paper titled “ Market and Firm Reaction to Targeted Tax Benefits: Evidence From the Tax Reform Act of 1986“ in the University of Connecticut School of Business that investigated the tax Reform Act of 1986 that was targeted to some steel manufacturing firms. The author’s research found that firms receiving the refund proceeds used it to pay down debt in the years following [the tax cuts], rather than to increase capital assets, cash holdings, payouts to shareholders, acquisitions, or new employment.” Other research examined data on U.S. income spanning decades from 1962 to 2014 the World Wealth & Income database, found that all the tax cuts passed in these periods did not really have a significant effect on the overall income share for wage earners in the bottom half of income distribution.

In the 1994 Lynn A. Karoly, a professor and senior economist at Rand Corporation contributed to a research paper titled “Tax Progressivity and Income Inequality,” which found that more than 2⁄3 of the rising overall income inequality from the post-war low in 1968 to 1989 occured during the 1980s. In July 2018, a professor named Jennifer Luchs-Nunez published a research paper titled “ Market and Firm Reaction to Targeted Tax Benefits: Evidence From the Tax Reform Act of 1986“ in the University of Connecticut School of Business that investigated the tax Reform Act of 1986 that was targeted to some steel manufacturing firms. The author’s research found that firms receiving the refund proceeds used it to pay down debt in the years following [the tax cuts], rather than to increase capital assets, cash holdings, payouts to shareholders, acquisitions, or new employment.” Other research examined data on U.S. income spanning decades from 1962 to 2014 the World Wealth & Income database, found that all the tax cuts passed in these periods did not really have a significant effect on the overall income share for wage earners in the bottom half of income distribution.

Montclair State University economist Edmond Berisha wrote a paper in the Economics Bulletin titled “Trickle Down? A little bit” and he stated, “Claims that trickle-down economics lift all income shares through lower taxes are not supported by the empirical findings.”

Kansas state tax reform experiment: “A cautionary tale for all future tax cuts”

The economic research reporter Clark Merrefield points to a study published back in 2010 in the American Economic Review, by two economist professors from University of California, Berkeley. And according to these professors, (which examined the historical macroeconomic effects of tax legislation) concluded that there really only 4 main reasons that most tax (cut or raised) changes happen:

- Balancing the economy

- Paying for government spending

- Shrinking an inherited budget deficit

- Promoting long-term growth

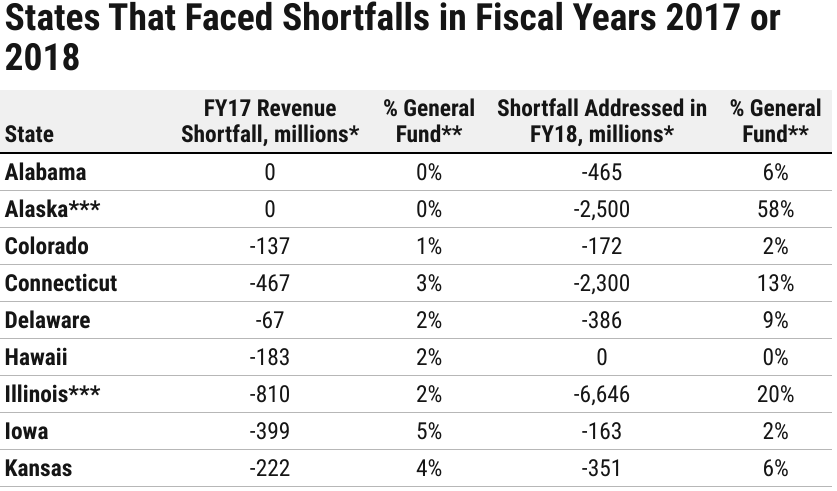

He goes on to cite an example, when Sam Brownback, the then Governor of Kansas in 2012, passed a massive corporate and personal income tax cut reform package. His tax cut in Kansas targeted pass-through firms rather than C-corporate firms. The tax program lowered the state tax rate on pass-through business income to zero. He says that Mr Brownback claimed the tax cuts would confront a looming deficit, where he wrote Op-ED in the the Wichitaw Eagle, where he said the tax cuts would “pave the way to the creation of tens of thousands of new jobs, bring tens of thousands of people to Kansas, and help make our state the best place in America to start and grow a small business.” Lofty and ambitions promises. The only problem is, less than two years later, the tax reform did not boost investment or stimulate employment growth like he had hoped, according to an analysis published Public Finance Review in 2017 titled “The Short-term Effects of the Kansas Income Tax Cuts on Employment Growth.” Shi Qi, an economist at College of William and Mary, and Don Schlagenhauf, an economist at Federal Reserve Bank of St. Louis, published a paper in the Society of Economic Dynamics, which analyzed data from the Kansas Department of Revenue, and concluded “The Kansas Tax Experiment is widely reported as a dismal failure, and a cautionary tale for all future tax cuts.” These economists also made a comment about the tax cut choice of targeting “pass-through entity” firms (which face tighter capital constraints and a decline in capital formation) rather that C-corporate firms. “In contrast, a lower corporate income tax rate leads to an expansion in the C corporate sector resulting in an increase in output, consumption, and capital formation. Moderate job growth follows.”

And as the Kansas economy began to slow down and the state government faced a fiscal $350 million revenue shortfall crisis, in 2017 a supermajority of the Kansas legislature repealed the tax cuts over Brownback’s veto, according to reporting by CNBC. A year after the repeal was enacted, Kansas is now running a budget surplus. In addition, it improved its ranking on CNBC’s 2019 America’s Top States for Business, by going from a 35 to 19 this year.

{kind=link}