New Revenue Recognition Standard: Effectively Managing Accounting Change

Significant changes to revenue recognition for financial accounting are almost here.

Significant changes to revenue recognition for financial accounting are almost here.

Nobody ever said that change is easy. But, the most successful businesses constantly embrace change. One of the biggest changes to the accounting world will soon take place, and businesses will have to adapt if they want to thrive in the future.

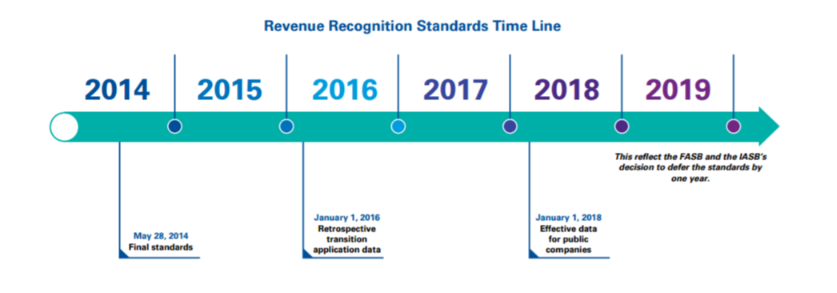

On May 28, 2014, the FASB (Financial Accounting Standards Board) and the (International Accounting Standards Board) issued new accounting standards intended to replace existing U.S. GAAP (Generally Accepted Accounting Principles) and IFRS 15 (International Financial Reporting Standard) guidelines. These new guidelines introduced a new revenue recognition and cost model—ASC 606, Revenue from Contracts with Customers . The effective date for the new guidance is January 1, 2018 for calendar year of public companies and January 1, 2019, for calendar year of nonpublic standards, early for years that begin on or after January 1, 2017.

The new revenue recognition standards will impact virtually every organization that enters into contracts for the delivery of goods or services – which affects how and when revenue is recognized. According to the American Institute of CPAs, the new standard has the potential to affect every entity’s day-to-day accounting, as well as the way business, is executed through contracts with customers. ASC 606 will eliminate current transaction and industry-specific guidelines under U.S. GAAP rules and replace them with a principle-based approach for determining revenue recognition.

The new standards are expected to significantly affect revenue recognition practices in the software technology, telecommunications, aerospace and defense, media, real estate, contract manufacturing and life sciences industries.

Almost all industries within the targeted scope of guidance will be required to make changes, in some form, in order to be compliant. Implementation of the new revenue recognition standard is not limited to financial reporting only. In addition to changes in accounting positions and policies, an organization should anticipate modifying information technology (IT) systems, business processes, and internal controls prior to the effective date of the standards.

Almost all industries within the targeted scope of guidance will be required to make changes, in some form, in order to be compliant. Implementation of the new revenue recognition standard is not limited to financial reporting only. In addition to changes in accounting positions and policies, an organization should anticipate modifying information technology (IT) systems, business processes, and internal controls prior to the effective date of the standards.

The objective of the new guidance is to establish the principles to report useful information to users of financial statements about the nature, amount, timing, and uncertainty of revenue from contracts from customers

All of these changes can have a significant effect on company’s tax positions, compliance, and planning. Therefore, it is important for the organization’s tax function to understand and plan for the impacts of the new financial accounting standards well in advance of any changes made to accounting policies, IT systems and processes, and controls.

It Could Impact:

- Timing of revenue recognition

- Profile of margins on contracts

- Systems and processes including data collection

- Contract negotiations with customers

- Revenue based metrics

- Debt covenants and employee rewards schemes

- Disclosures in annual reports

———————————————————————————————————————-

If you have:

- Multiple goods or services in a contract

- Contracts that span more than a year

- Contracts with variable consideration

- Licenses or royalty arrangements

- Costs to obtain or fulfill a contract

- Contracts that change throughout the term

- Compensation or debt linked to revenue

-

"Companies with even moderately complex customer contracts are going to find that the new rules will have extensive impacts best dealt with by software designed specifically to handle the new requirements"

CEO of Huckabee CPA

Tax Impacts – The Sleeper Issue

A change in revenue for financial accounting purposes ( e.g., a change in the timing or character of revenue) may have a large impact on your organization’s tax data, processes, controls and tax compliance, planning and reporting. It is quite common for a company to use one or more tax methods of accounting that may approximate or rely heavily on, revenue recognition policies and methods used for financial reporting purposes.

A change in revenue for financial accounting purposes ( e.g., a change in the timing or character of revenue) may have a large impact on your organization’s tax data, processes, controls and tax compliance, planning and reporting. It is quite common for a company to use one or more tax methods of accounting that may approximate or rely heavily on, revenue recognition policies and methods used for financial reporting purposes.

Under the revenue recognition standards, a company could be required to unbundle contracts for goods and services that have historically been treated as a single unit of account for financial accounting purposes. Said companies will be required to allocate revenue to each performance obligation based on stand-alone selling prices of each revenue obligation, and potentially accelerate or decelerate each revenue stream as compared to existing accounting policies. Therefore, changes to the underlying financial accounting methods, and possibly the processes, data and IT systems used to support such methods will require a significant overhaul. This would include a careful evaluation of the effects on tax accounting positions, policies and calculations.

The impact on a company’s tax function is not only limited to potential changes to federal income tax methods(i.e. timing issues).There are a number of additional areas that will have to be carefully considered

The following covers the some of the potential tax implications of changing to the new financial accounting standards:

Federal Tax

- Potential changes in timing of revenue recognition for financial reporting that will require accounting method changes for tax purposes; potential impact on net tax liability

- Tax may not be able to use the method adopted under the new financial reporting model and might need to identify and create a new book-to-tax difference (Schedule M); potential impact on net tax liability

- Impact on data availability, processes and controls used to support existing or new accounting methods

- Need or opportunity to harmonize all tax reporting systems with new or augmented enterprise resource planning (ERP) systems or new revenue recognition models to be used for financial accounting purposes

Executive Compensation

- Perform metrics for long term bonus compensation grants may be affected by the new standards.

- Section 162(M) performance-based compensation arrangements may need to be reworked or rethought under the new regulations.

- If incentive compensation is tied to revenue or earnings, the plans may need updating. This does only pertain to commissions. Consider if your executive incentive compensation is tied to revenue, margins or net income, and how this might impact the structure of your compensation plans.

Accounting for Income Taxes

- Adjustments to temporary differences as of the date of adoption (retrospective vs cumulative method)

- Changes in accounting may impact pre-tax book income, which may indirectly impact the effective tax rate

- New or different temporary differences may impact deferred taxes

State and Local Taxes

- Potential effects of determining revenue based on apportionment factors used for calculating state income expense and used for determining the applicable rate used for measuring state deferred income taxes

- Federal tax implications will flow through to the state tax base in most circumstances

Indirect Taxes

- Impacts on state liabilities in gross receipt tax states (e.g. acceleration or deferral of income under new standards)

- Potential issues as tax authorities seek to reconcile revenue identified in accounts against indirect tax invoices and filings

- Newly created performance obligations may be subject to sales and use taxes in contrast to prior guidance, which permits aggregation (e.g., software vs services)

- The potential effects of using revenue-based apportionment factors for calculating the deduction of value added tax (VAT) and indirect taxes incurred on costs (usually companies can only take a credit for VAT and other indirect taxes incurred on costs if they can link those costs to specific revenue)

Foreign Tax and US Taxation of Foreign Operations

- For local country reporting purposes, some foreign jurisdictions will require a change to the new model, while others may maintain local statutory accounting, or allow for an optional adoption of the new standards.

- Potential effects on the amount and timing of income recognition for controlled foreign companies, which could impact earning and profits, foreign tax credit pools ( and repatriation planning), the calculation of Subpart F income tax liabilities (including the potential need to record deferred tax liabilities on Subpart F income expected to be realized in the future)

- Potential effects on deferred tax liabilities recorded on outside basis differences for which the indefinite reversal criterion cannot be met

Transfer taxes

- Change to amount and timing of revenue recognition, could affect intercompany transfer pricing policies and amounts, particularly when the prices are set or tested using revenue or profit based formulas.

- Companies may need to consider whether their strategies and documentation supporting transfer needs to be revised or updated to account for the new standards.

Tom Huckabee, CPA can help your organization develop a plan and timeline to identify, assess, and address the important tax implications associated with a company’s implementation of the new recognition revenue standards by assisting with:

Assessing the impact on tax reporting, process, systems, and planning; 2016 for public companies, 2016 to early 2017 for private organizations

Assessing the impact on tax reporting, process, systems, and planning; 2016 for public companies, 2016 to early 2017 for private organizations Designing the solutions that address these impacts; 2017 for public companies, 2017–2018 for private organizations

Designing the solutions that address these impacts; 2017 for public companies, 2017–2018 for private organizations Implementing a future state, including process and IT enhancements; January 1, 2018 for public companies, January 1, 2019 for private organizations

Implementing a future state, including process and IT enhancements; January 1, 2018 for public companies, January 1, 2019 for private organizations

Conclusion

A robust assessment phase, aligned properly to a company’s financial accounting assessment and implementation efforts is important to lay the framework of a successful project.

The new revenue recognition standard takes effect for most companies in 2018, and time is running out. It’s important to start the tax assessment early to ensure that tax issues and needs are addressed and communicated within the organization as the company designs and implements changes to its accounting data, processes and IT systems to accommodate the new financial revenue accounting recognition standards. Here is a technical accounting revenue recognition guide from PWC on every aspect of this subject. Get ahead of the process, nail down a revenue recognition implementation plan and push for resources necessary to get this project underway. If you have any questions about the new standard or if you need assistance with the implementation process, feel free to contact us for a consultation.

![]()

{kind=link}