Tax Reform: House Tax Cuts and Jobs Act Bill Passed in The Senate

On December 2, 2017, the modified Senate Tax Cuts and Jobs Act (H.R. 1) was passed in its chamber with a vote, almost entirely along party lines, of 51-49; the sole Republican dissenter being Senator Bob Corker of Tennessee.In order to accomplish a favorable vote, Republican leaders were forced to make significant concessions behind closed doors to gain the votes of a holdout and fence-sitter legislators in their own ranks. Among these significant concessions was the decision to maintain the corporate Alternative Minimum Tax (AMT). Corporations and their lobbyists alike were blindsided by this compromise which was not included in the final Senate Finance Committee version of the bill. Also included fairly unexpectedly in the approved Senate Tax Cuts and Jobs Act (H.R. 1) is the benefit to write-off equipment for five years’ phasing out, rather than immediate elimination; particular details concerning the reshaping of the international business tax code by shifting from a deferral system to a territorial system and pass-through business specifics. Repealing the corporate AMT would have permitted businesses to use myriad deductions and/or credits for the following and more:

- Research & Development (R&D)

- Intellectual Property

- Equipment Spend

The inclusion of the corporate AMT would basically snare corporate America and prevent it from claiming deductions, and effectively enforce a flat tax with no loopholes that could be used to circumvent taxation. With the AMT’s most prominent victims being tech companies with heavy R&D, utility companies, and banks that claim credits for investing in troubled American areas, the AMT could also undermine incentives for international tax-restructuring as it relates to credits for intellectual property. With the R&D credit, a critical pro-growth tool, incentive in doubt, consequences are uncertain at this time and the prospect of having a universally competitive tax code is at risk.

Trade-Offs

Senate Republicans retained the corporate AMT as a way to raise revenue to pay for an expanded pass-through deduction and a tax break for state and local property taxes. The AMT requires some businesses to pay a 20 percent rate if they are eligible for too many tax breaks.

Senate and House leaders are already hashing out and negotiating differences so to reconcile and reach a middle-ground between their differing versions of sweeping tax reform change, hoping to deliver a final bill to President Trump to sign into law by 2017 year-end. An obvious key contention point will be the corporate AMT, which is repealed in the House version but kept intact, with a higher exemption amount, in the Senate version.

Blackstone CEO: Tax bill is a ‘game changer’ from CNBC.

![]()

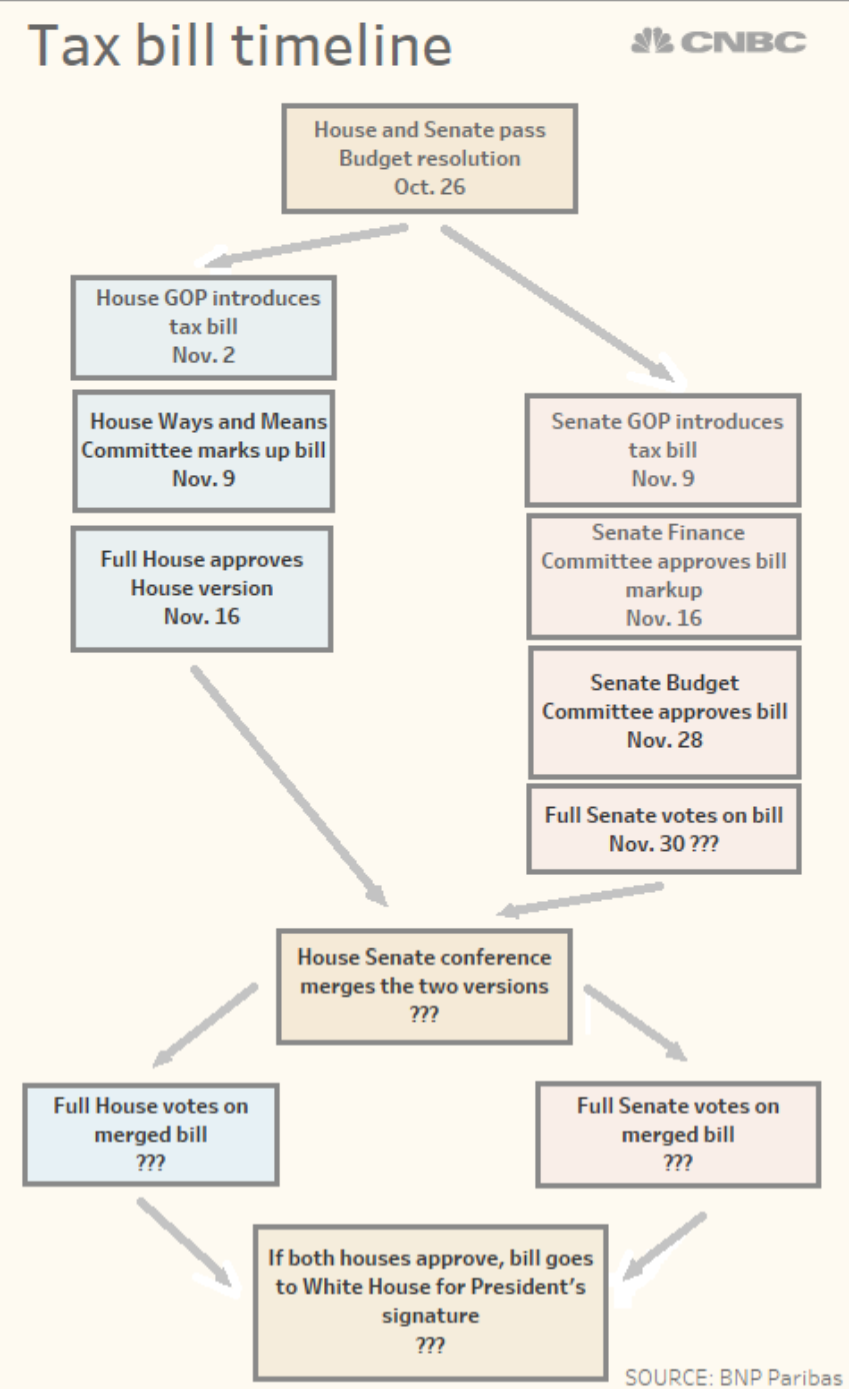

Yet another pivotal step in the process towards the Tax Cuts and Jobs Act bill becoming law, and resulting in sweeping changes to the American tax code, occurred on November 29, 2017. This step was the United States’ Senate voted along party lines to advance the Republican tax reform bill to debate on its floor of which it passed. The previous day, November 28, 2017, the Senate Budget Committee approved the GOP Tax Cuts and Jobs Act. The aforementioned critical approvals came on the heels of the GOP’s proposed legislation’s favorable vote in the United States House of Representatives, and a similarly favorable vote by the Senate Finance Committee for its respective version of the tax reform bill, both of which occurred on November 16, 2017.

Yet another pivotal step in the process towards the Tax Cuts and Jobs Act bill becoming law, and resulting in sweeping changes to the American tax code, occurred on November 29, 2017. This step was the United States’ Senate voted along party lines to advance the Republican tax reform bill to debate on its floor of which it passed. The previous day, November 28, 2017, the Senate Budget Committee approved the GOP Tax Cuts and Jobs Act. The aforementioned critical approvals came on the heels of the GOP’s proposed legislation’s favorable vote in the United States House of Representatives, and a similarly favorable vote by the Senate Finance Committee for its respective version of the tax reform bill, both of which occurred on November 16, 2017.

Currently, the bill is the subject of a 20 hour hectic and fiery debate in the Senate concerning amendments to the Tax Cuts and Jobs Act. Also known as having a Vote-a-Rama, the Senate will then vote on each of these proposed amendments, one by one. Any approved changes to the bill would then be integrated into the Senate Tax Cuts and Jobs Act, and then a final vote on the bill in its entirety will occur in the Senate. A Senate approval would then move the bill forward to intense negotiations with the House and the emergence of a final bill based on these negotiations. The final bill will then need to be voted on and passed by both the House and Senate for the presentation of final bill to President Trump.

,

,Obstacles to Success in the Senate

Concurrently, as the Tax Cuts and Jobs Act moves along the process, Republicans are trying to confirm that they have secured the necessary votes for passage. Party leaders are vigorously pursuing behind-closed-door deals so the Tax Cuts and Jobs Act will pass a Senate full chamber vote. Undoubtedly, substantial bill alterations are being raised as possible amendments to the Senate proposal. Debate concerning the tax code overhaul is limited to no more than 20 hours and will be immediately followed by a vote-a-rama, which is a marathon series of votes on the amendments that were brought to the table during that 20 hour period.

Compromising with Undecided GOP Senators

GOP leaders are placing heavy emphasis and attention on members of their own party who appear reluctant to support the Tax Cuts and Jobs Act. For Republicans, the focus is really just on Republican Senators, instead of focusing on Democrat Senators, who the GOP has all but written off as lost causes when it comes to voting for the passage of the Tax Cuts and Jobs Act.

Republican Senate leaders have once again found themselves in a precarious position whereby they are at risk for alienating some of their members during the process of trying to appease other Republican Senators. As a result of the GOP’s compromising and persuasion efforts, a handful of Republican Senators, who had previously doubted the bill, actually voted for the bill’s passage to the Senate floor for debate. It is important to know that this does not mean that those Senators plan on voting for the actual bill when the full Senate chamber vote occurs on a final and revised plan.

Certain Republican lawmakers had voiced their skepticism about issues, including tax cut generated deficits, pass-through businesses treatment and the stipulation that Obamacare’s individual mandate would be repealed.

Possibly the largest big-ticket item being debated is the addition of a “trigger” mechanism into the Tax Cuts and Job Act. The type of trigger mechanism being described here would be one that allowed for the raising of taxes should the United States’ economic growth fail to generate its anticipated revenue from the tax overhaul. Created and designed to appease Senators with particular federal deficit concerns, the trigger has garnered resistance and criticism from numerous GOP senators. Sens. Dean Heller (R-Nev), David Perdue (R-Ga) and Thom Tillis (R-N.C.) have all noted that the trigger mechanism inclusion in the bill is not to their liking. However, a majority of the GOP lawmakers have insinuated that their opposition to the trigger will not make them vote against the bill.

GOP holdout Senator Bob Corker (R-Tenn) voted for the advancement of the bill to debate on Senate floor, but this was only after agreeing to an extremely tentative deal. This deal did actually include a fiscal “trigger,” to put Corker at ease with his concerns about the the Tax Cuts and Jobs Act’s effect on budget deficits. Although specific details have not been released, it appears that the trigger mechanism stands to raise taxes if American economic growth fails to generate as much revenue as expected from the tax code overhaul. The addition of the trigger clause also appears to be helping win the support of Senator Jeff Flake (R-Ariz) and Senator James Lankford (R-Okla), as both Senators are extremely concerned about compensating for the estimated $1.5 trillion in costs that come along with the Tax Cuts and Jobs Act. An interactive graphic from the New York Times illustrates this idea very well.

How past income tax rate cuts on the wealthy affected the economy

Under the GOP’s recently released framework, the top income tax rate would return to George W. Bush-era levels. The GOP has historically claimed reducing the top tax rate will create economic growth, but that hasn’t always happened.

Including the increase of a the tax deduction for pass-through businesses is another area of contention, where tweaks are being made to appease Senators who are undecided or on-the-fence. Senator Ron Johnson (R-Wisc) is advocating more reduction on the tax burden assumed by pass-through companies, which currently pay taxes based on individual rates. Johnson’s argument is that pass-through companies will be treated unfairly, compared to corporations. After assurance that these concerns would be addressed by the Senate or in the Senate’s joint bill with the House of Representatives, he voted to pass the bill to the Senate floor.

Another issue being addressed is the elimination of the federal deduction that allows state and local taxes to be deducted from federal filings.

Senate Bill Popularity Considerably Strengthened

As mentioned, a whirlwind of final-minute deal making assisted in the garnering of the support of a few key Republican lawmakers who had expressed concerns about the $1.5 trillion package, particularly its treatment of small businesses and its effect on the deficit.

Turnaround of such a rapid nature highlights the extreme pressure Republicans are up against to pass a tax code bill and finally notch an unprecedented legislative win during their first year controlling both the White House and Congress. In order to help push the bill forward, President Trump visited Capitol Hill for a lunch meeting with Republican Senators, where he made promises to some lawmakers and admonished other lawmakers.

At the White House later in the day, Trump said, “I think we’re going to get it passed…and it’s going to have lots of adjustments before it ends, but the end result will be a very, very massive — the largest in the history of our country — tax cut.”

At the conclusion of the luncheon, Republicans emerged increasingly more optimistic about the Tax Cuts and Jobs Act’s fate and played down the concerns that had threatened its passage.

Senate Floor Decision Process

The Senate 52-48 party line passing of the Tax Cuts and Jobs Act, as part of standard procedure, has triggered the bill’s full Senate chamber floor debate. Republicans are aware that significant alterations to the proposed legislation need to be made before a final Senate full chamber vote- that is what they are doing just now. The Senate floor is open for up to 20 hours of debate for the introduction of proposed amendments to the Tax Cuts and Jobs Act, as it stands in its current form.

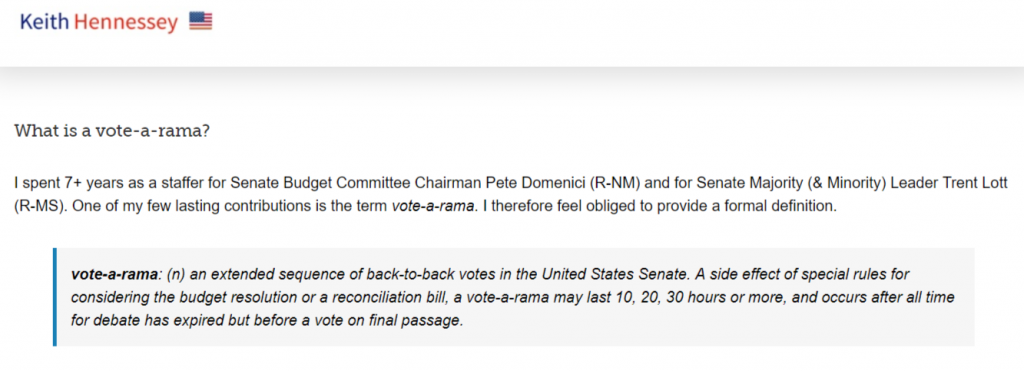

What is a Vote-a-rama?

A vote-a-rama is a grueling marathon tradition during which each amendment or change to a bill proposed in the 20 hour Senate floor debate is voted on. While the tax reform bill is not subject to a filibuster, all changes and amendments must be germane and consecutively voted on without any legitimate or real debate.

During the vote-a-rama process, each and every amendment and change is considered and voted on for roughly 10 minutes until all amendments have been heard and voted upon. A vota-a-rama is a notoriously exhausting process of which a majority of Senators have said makes it nearly impossible to comprehend what is actually being considered.

The term vote-a-rama was coined by Keith Hennessey, a one-time seven-year staffer for the Chairman of the Senate Budget Committee and Senate Majority (then Minority Leader.) Hennessey’s technical definition is shown in the below image.

Hennessey’s further mentions that, “The vote-a-rama is an unusual cultural institution within the Senate. All 100 Senators are on the floor, in the cloakrooms, or right outside the Senate Chamber for hours and hours upon end. Another 100-ish staff are packed onto tiny staff benches in the rear of the Chamber, one for Republican staff and another for Democratic staff. Everyone is usually exhausted during the vote-a-rama, which comes near the end of an arduous and usually conflict-ridden legislative battle.”

Hennessey’s further mentions that, “The vote-a-rama is an unusual cultural institution within the Senate. All 100 Senators are on the floor, in the cloakrooms, or right outside the Senate Chamber for hours and hours upon end. Another 100-ish staff are packed onto tiny staff benches in the rear of the Chamber, one for Republican staff and another for Democratic staff. Everyone is usually exhausted during the vote-a-rama, which comes near the end of an arduous and usually conflict-ridden legislative battle.”

For Hennessey’s full description of a vote-a-rama, click here.

What is the “Reconciliation” Method?

With 52 seats in the Senate, Republicans can only stand to lose two votes if they want to pass the Tax Cuts and Jobs Act with a simple majority which, under certain budget rules, is required. This, of course, assumes all Independents and Democrats vote against the proposed legislation.

Fast-tracking the tax legislation through the Senate without support from Democrats, Republicans are going to use a budget process known as reconciliation. Essentially, this stipulates that, rather than needing 60 votes to maintain the bill’s forward momentum, the 52 seats held by Republicans can proceed to a vote and pass the legislation with a simple majority of 51 votes.

What is the Byrd Rule?

The Senate’s reconciliation process is contingent on two qualification terms. The first qualification is that the bill must meet the terms of an adopted budget resolution. The second qualification is that the bill must adhere to rules created by and named for the late Robert Byrd, the West Virginia Democrat who served as Majority Leader from 1987 to 1989.

The House plan has already passed the first test. The 2018 fiscal budget resolution does not allow a tax bill to add over a total of $1.5 trillion to deficits over 10 years, and the Joint Committee on Taxation’s initial assessment of the measure puts the Tax Cuts and Job Act cumulative shortfall at $1.41 trillion during the next decade.

In 2027, a red flag is raised, as analysis completed by a nonpartisan joint committee shows that the Tax Cuts and Job Act will contribute $156 billion to a 2027 budget shortfall- this is a virtual guarantee that the deficit will rise in 2028. The possibility of such an event happening would trigger the Byrd Rule. The Byrd Rule would give Democrats an opening to raise an objection to the bill on the Senate floor. An objection raised on the Senate floor would then require 60 votes for passage.

“The bill has a massive Byrd Rule problem,” said Bill Hoagland, a previous Republican Senate Budget Committee staff director.

The corporate tax rate of 20 percent would likely have to return back up to 35 percent in the 11th year of the bill, in order for the bill to comply and be in accordance with the Byrd Rule.

For more on the United States House of Representatives Committee on Rules Majority Office’s Byrd Rule, click here.

Aligning of House Bill & Senate Bill

If the Senate chamber passes its own respective tax reform bill, legislators must then reconcile their plan with the entire separate legislation passed by the House. The chambers must decide how to treat multiple key differences, particularly the treatment of popular state and local tax deductions.

Republican lawmakers have different priorities, depending on whether they are a member of the House or Senate. For example, the Senate tax reform bill has individual income tax cuts denoted as temporary. It also delays the implementation of the corporate tax cut by one year. A full repeal of an Affordable Care Act provision requiring most people to have health insurance coverage or pay a penalty is also an issue.

The House of Representatives’ bill also cuts the corporate tax rate to 20 percent, down from 35 percent. On the individual side, the House bill collapses the amount of tax brackets to five from seven and transitions the United States of America to an international tax system so to be more in line with the rest of the world. Elimination of many popular deductions, including one for state and local taxes is also part of the House plan.

Practically doubling the existing standard deduction that taxpayers claim on their tax returns are also included in the House version. Incidentally, the House version also increases the child tax credit to $1,600 per child from $1,000. Contrastly, the Senate bill, increases the child tax credit to $2,000 per child and reduces the top marginal tax rate to 38.5 percent, from 39.6 percent. The House keeps that 39.6 percent top marginal tax rate for the wealthiest.

Additionally, a full repeal of the estate tax is not included in the Senate bill but the House bill scraps the so-called death tax entirely. In the Senate plan, individuals tax cuts will expire at the end of 2025; those reduced and restructured individual tax rates in the House plan would be permanent.

The state of the deductions for state and local taxes (SALT) from federal filings is also a huge issue that needs to be reconciled. Opposition from Republicans in high tax states like California, New York, and New Jersey, all of who have constituents that rely heavily on SALT deductions have been very vocal. The House bill does permit the deduction of up to $10,000 in property taxes, but certain Congressional members simply do not believe that this concession is good enough to compensate for a significant portion of SALT deduction elimination.

Republicans in the Senate have also added an extremely controversial provision to their bill: the repeal of the Affordable Care Act’s (ACA) individual mandate. This provision was added to increase revenue.

“We’ve got a long road ahead of us,” Speaker of the House, Paul D. Ryan (R-Wisc) notes.

Conclusion

The full-service accounting firm of Thomas Huckabee, CPA services the San Diego, California area. Our CPAs and accountants provide professional help and advice to clients, as those clients navigate the present tax code and any alterations to that code which may be made into law. Contact us to learn more about the accurate and efficient services we can offer our clients.

{kind=link}