4 strategies to change your companies culture of managing working capital

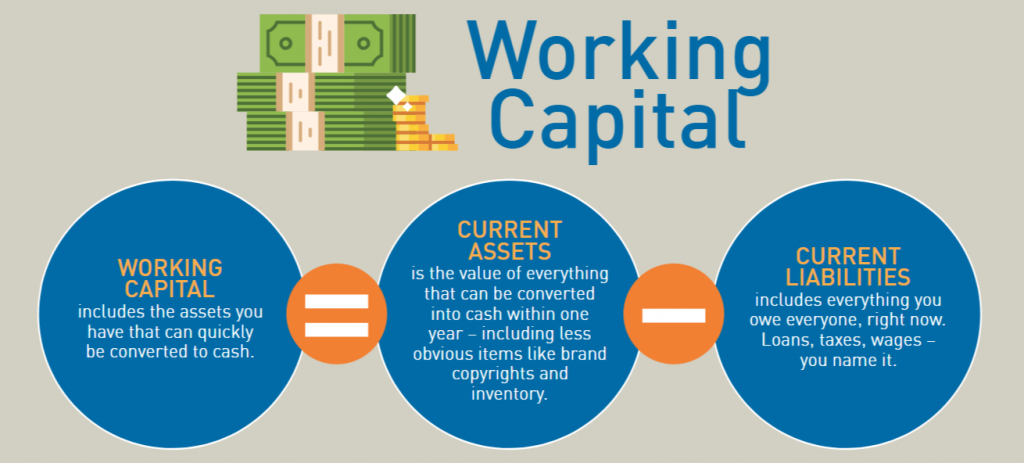

Managing working capital, or operating liquidity (the speed at which assets can convert into cash), has always been crucial to the long-term financial health of top companies.

Managing working capital, or operating liquidity (the speed at which assets can convert into cash), has always been crucial to the long-term financial health of top companies.

Capitalizing on opportunity requires a cultural shift. Prioritizing working capital allows companies to make strategic investments, which in turn drive operational efficiencies and reduce overhead. Conversely, not having enough operating liquidity because assets are tied up in things like inventory or unpaid invoices can have a huge effect on cash flow. On any given month, there are a 1,000 everyday decisions that can dramatically increase the cash needed to run a medium to large company.

These are the day-to-day business occurrences that are so common that they appear to be inconsequential. As an example, it could be the energy company plant manager who made the decision to order several months’ more worth of spare parts than he usually does— tying up cash to avoid worrying so often about not having a certain part. Or it could the employee at a consumer packaged goods corporation who happens to be 4 days late sending an invoice for a shipment of soap, missing a customer’s monthly invoice deadline and ultimately delaying payment terms deep in a new supplier contract and inadvertently agreed to pay the supplier’s invoices within 10 days – instead of the usual 45 to 60 days.

Stories like these are so commonplace, and they happen every day by the hundreds or thousands, in big companies; at all levels as well as across geographies and business divisions.

So given these complexities, sustainably running the business with less working capital requires a new way of working. The management consulting firm Mckinsey lays out a thorough post on why the analytical toolkit of the finance function is only part of the solution; the methods used for organizational transformation are just as crucial. This can include nurturing awareness and conviction, reinforcing mind-sets and behaviors with formal mechanisms, as well as deploying the right talent skills. The return on that effort can be quite surprisingly high, reducing the amount of cash needed to run a business by 20 to 30 percent- sometimes considerably more. One California based natural resources company, as an example recently reduced its working capital by more than 40 percent in less than a year’s time period. And that was worth almost $1.5 billion, three times its initial target.

Of course, the effort to improve working capital should be considerate to not tipping over into increasing risks to quality, fulfillment, or speed, such as trying to cut inventory so low that it impinges on operations or setting such strict payment terms that customers flee to other suppliers. Yet the reality is that in modern companies, there are buffers at every level; hyper-conservatism often reigns. Businesses that can find a way to achieve the right balance of attention to detail and operating discipline can demonstrate a broader and stronger stewardship over their enterprise.

There are a number of strategies particularly useful in advancing an initiative to optimizing working capital.

1) Motivate through conviction

Sometimes the day-to-day routines and behaviors are not easy to shift. Employees cannot just be told what to change; they need to understand why it’s important to change. Because in the absence of conviction and understanding, some of the coercive habits that a program seeks to rid itself of, can quickly come back. And since shareholder value captures only a small portion of what motivates employees – research shows that meaning at work is an amalgam of understanding one’s contribution to the organization, to society and to other coworkers – the usual emphasis on theoretical appeals to cash generation and shareholder returns often falls short.

Given the large number of workers who need to buy into a program to improve working capital, research has found that defining working-capital improvements with respect to being great at one’s job, or achieving functional excellence, is often more personal than persuasive. For example, the c-suite at a major manufacturing company would talk about “running a tight-knit shop” as the focus of their working capital program— with a happy by-product of more cash and stronger shareholder returns. So the cash conversion then became an indication of operating discipline; how well the business manages its customers and suppliers, cycle-time speed, and even things such as sending out invoices on time. But the thing is, that in practice any improvement goes both ways. The behaviors support better working capital management, such as analyzing often-ignored data sets, can also help improve performance overall.

As with any transformational improvement, changing a company’s culture around working capital requires strong CEO support and ultimate involvement. Because only the boss has the clout to set the vision, assign accountabilities, and get different functions running in the same direction. In one recent working-capital transformation, a CEO personally announced performance targets, made it clear to his executive team that their careers depended on delivery, consistently communicated about the importance of working capital in dialogues to his employees. Now that does mean that the CEO has to be responsible for running the whole program; smart ones wil delegate day-to-day oversight to another executive. At one industrial company, the CEO appointed a business unit interim CFO to oversee and run the program as the group wide “cash leader” – though the CEO continued to reinforce the program’s importance in all his internal communications.

2) Set reality-based targets

An employee’s individual conviction is difficult to manage in the absence of formal mechanisms, such as performance targets, that support the priorities of the company. In a corporation that hasn’t taken on working capital before, financial managers will anchor their expectations of what is possible to their current experience – which is similar to setting other performance targets and budgets. This inherent conservatism handicaps a business’s ability to make step-change improvements in working capital efficiency.

Consider the experience of a San Diego based company, where the executives pushed inventory managers to reduce working capital. In this case, a single target across several units became a nuisance to the company’s one service business. Now although the one service business held no inventory, its managers still had to do all the paperwork. Similar scenarios can play out or apply to corporations in different companies with different business practices, where managers may not be able to achieve company-wide targets for the timing of accounts receivable or collections.

As with any performance-improvement effort, targets need to be tailored to the circumstances of specific units. A clean-sheet approach can help. This allows managers to calculate working capital goals at the level of individual operational activities that drive working-capital balances, while also paying attention to other parameters of the business, like risk appetite. This approach can force a reexamination of basic assumptions around even well established structural norms, such as standard supplier-payment terms or common reordering points. And the result can often point to an opportunity that dramatically exceeds the instincts of the front line. Another example, an oil and gas company that uses different valves could optimize its inventory for each type of valve; the structural solution would instead be to standardize and possibly use one type of valve in order to enjoy a step-change reduction in the amount of safety stock it would carry.

So performance targets should also be designed to encourage achievable changes, not simply to game month-end balance-sheet numbers. It is often preferred to focus on both working-capital balances – normalized for uncontrollable factors like currency exchanges rates, major input prices, and inflation — as well as working working-capital days. If you look at it as a rolling average of working-capital days is best to alleviate seasonality. While not perfect, working capital days are the closest thing to a measure of working capital efficiency that can be easily understood across a large organization.

In order to change behaviors, targets should be promulgated company-wide and be reflected in team and individual performance metrics. As an example, targeting a structurally lower receivables balance (and days sales outstanding) could change its sales incentives to reward the actual amount of cash brought in instead of just signing contracts in hopes of future revenues. One California based manufacturer accomplished this by adjusting its main measure of performance from earnings to cash flow from operations. This motivated a business unit Chief financial offer to refrain pushing the sales staff to sign contracts before the end of a quarter to show growing backlog regardless of the payment terms. Instead, she started to push for advantageous receivable terms to ensure a faster time to cash.

3) Promote a steady drumbeat of success

So when you have the right targets and accountabilities setup, frontline employees, middle managers, and those with intimate knowledge of practices in, say collections or warehousing will be best placed to point out opportunities. That can produce a plethora of new ideas for experiments or initiatives that build momentum with a steady drumbeat of success stories.

The problem can lie in identifying these breakout success stories can happen only if all those initiatives care centrally tracked. We’ve found that a standard initiative-pipeline methodology works well, including simple, principles-based valuation, stage gates, a regular cadence of initiative review meetings, and a user-friendly internal digital platform. One business that went through a recent transformation, the managers tracked more than 300 initiatives. Each week, they would send an email to the entire staff celebrating the most successful stories and the people behind them — and inspiring others to tackle similar challenges.

Finally, working-capital performance hardly ever improves the same way across every business unit and region, or across inventory, receivables and payables. Financial management performance dashboards can allow managers to review a significant degree of detail, identify areas of success, and quickly pinpoint problem areas. So Performance metrics can also be shared widely to generate healthy competition among different business units or regions as well. The managers at San Diego software company, as an example, started measuring the frequency of invoicing in different states they have has offices in. Since invoicing is leading indicator of receivables, that enabled them to rectify problem areas before they ended up in the balance sheet.

Managers of an auto-parts business monitored exceptions to new standard supplier-payment terms, and the results delighted management. More suppliers were actually willing to change or accept new terms than initially expected, shifting the internal debate from why strategic suppliers should be exempted to why they shouldn’t be.

4) Keep the center lean

Now even though frontline managers and staff members are accountable for delivering a change in day-to-day behaviors, they can’t do it alone. To help speed up their work, they need support from a central team that can manage the program and provide specialized expertise. Yet in my experience, having too large of a central team feel can make the rest of the organization feel as though the transformation is being done to them, not something that they should own and deliver themselves.

Instead, a lean central team that focuses on tracking performance, reporting overall progress to management, and putting in place enablers, such as policies and training, can make the corporation take action to deliver. The central team can also manage a handful of projects that don’t otherwise have a natural owner in the organization.

This does not require excessive bureaucracy; at a company of 3,000 employees, the central team can be less than 5 people. Notwithstanding its size and focus, however, the central team should be commanded by a seasoned CFO. As an example, the CEO of a natural resources business selected the CFO of one its business divisions to lead its global-capital optimization program. The CEO’s thought was that the CFO’s financial management experience would carry weight with other aspects of the business and the central team can push against any inherent conservatism on the part of other business leaders.

Sometimes specialized skills will sit centrally as well, particularly when initiatives require capabilities tackle the hardest bits. For example, advanced analytics using machine learning algorithm are well-suited to modeling safety stock or optimizing collections. Such expert skill sets are not always common in most businesses.

In one another example, IT equipment manufacturer deployed a team of data scientists to the commercial departments of its business divisions to help discover patterns in customers’ payment behaviors. This analytics-driven recommendation engine flagged accounts likely to need escalations, such as collection calls and sales stops’ — which ended up resulting in a 7 percent reduction in the accounts – receivable balance by increasing the speed and targeting of collections.

Conclusion

Focusing on achieving better working capital management can deliver astonishingly strong returns. But more than just an analytical toolkit of your company’s finance function is needed to make it successful. The strategies of organizational transformation — nurturing awareness and conviction, establishing formal mechanisms, and deploying the talent and skills -can help. Sometimes bringing an outsourced CFO on interim or consulting basis help to give suggestions and guidance. Today, companies must either focus their attention on building and maintaining an optimal working capital level or risk being left behind.

{kind=link}