As 2025 draws to a close, taxpayers must strategically optimize their tax positions before year-end. The transformative One Big Beautiful Bill Act (OBBBA) (P.L. 119-21) and other recent legislation have fundamentally reshaped the tax landscape, creating significant planning opportunities alongside new complexities for individuals and businesses alike.

From expanded deductions and adjusted thresholds to evolving international tax regulations and state conformity considerations, proactive year-end planning has become essential to minimize tax liabilities and maximize available benefits.

Critical Planning Areas for 2025

This year demands strategic action across multiple fronts:

- Enhanced SALT Deductions: Leveraging the increased state and local tax deduction caps

- Expanded Section 1202 Benefits: Optimizing qualified small business stock exclusions

- Revamped GILTI Regime: Navigating the restructured Global Intangible Low-Taxed Income rules

- Accelerated Charitable Contributions: Maximizing deductions under new contribution limits

- SECURE 2.0 Retirement Planning: Preparing for upcoming changes to retirement plan regulations

The Imperative for Action

Whether you’re an individual taxpayer, business owner, or corporate entity, the window for strategic tax planning narrows with each passing day. Understanding how these legislative changes intersect with your specific circumstances is crucial for achieving optimal tax outcomes in 2025 and positioning yourself advantageously for 2026.

The One Big Beautiful Bill Act (OBBBA) (P.L. 119-21), signed into law July 4, 2025, represents the most significant tax legislation in years, delivering extensive changes to business, international, and individual tax rules.

Legislative Highlights

Key provisions include making many TCJA benefits previously scheduled to sunset permanent, introducing enhanced business tax breaks, implementing new deduction limitations for individuals and businesses, and fundamentally restructuring international tax provisions. These changes carry different effective dates and expiration timelines, requiring careful strategic planning.

Year-End Planning Focus

The following overview examines critical business-focused OBBBA provisions and outlines essential year-end tax planning considerations to help you navigate this transformed landscape effectively.

Full Expensing of Qualified Property

This provision permanently restores 100% bonus depreciation for qualified property costs acquired on or after January 20, 2025.

Planning Considerations:

Eligible Property

- Qualified property includes tangible personal property with recovery periods of 20 years or less

- Qualified improvement property (QIP) for real estate purposes qualifies

- This provision substantially enhances the value proposition of cost segregation studies for real estate investors

Acquisition Date Requirements

- Property acquisition date is determined by when a written binding contract is executed

- Once a binding contract exists, the property is considered acquired as of that contract date

- Critical Warning: Assets placed in service before January 20, 2025, qualify only for 40% bonus depreciation—timing matters significantly

Important Restrictions

Several limitations may disqualify property from 100% bonus treatment:

- Property primarily used outside the United States

- Property financed through tax-exempt bonds

- Property leased to or used by tax-exempt entities

Special Depreciation Allowance for Qualified Production Property

The OBBBA introduces a new provision allowing taxpayers to immediately deduct 100% of the cost of certain qualified production property. This includes newly constructed factories, specific improvements to existing factories, and certain other qualifying structures. Eligible taxpayers may deduct 100% of the adjusted basis in the year the property is placed in service.

Planning Considerations

Qualified production property generally refers to the portion of nonresidential real property that meets the following criteria (among others):

- Used by the taxpayer as an integral part of a qualified production activity

- Placed in service within the United States or a U.S. territory

- Original use begins with the taxpayer

- Construction begins after January 19, 2025, and before January 1, 2029

- Placed in service before January 1, 2031

- Taxpayer elects to claim the immediate deduction

A qualified production activity includes manufacturing, production, or refining of tangible personal property. The OBBBA expands the definition of “production” to include agricultural and chemical production. To qualify, the activity must generally result in a substantial transformation of the property into a new product.

Additional considerations:

- Portions of property used for offices, administrative functions, lodging, parking, sales, research, software engineering, or other non-production activities are not eligible.

- Treasury is directed to issue guidance defining “substantial transformation,” but no regulations have been released as of this publication.

- The deduction is permitted for AMT purposes.

- The January 19, 2025 construction start date should be carefully considered in year-end planning.

- Many states may decouple from this provision for state tax purposes.

Increase in Section 179 Expensing

The OBBBA increases the maximum Section 179 expensing limit to $2.5 million and raises the phase-out threshold to $4 million. The deduction is reduced dollar-for-dollar when the qualifying property placed in service exceeds the $4 million threshold.

- Applies to property placed in service in taxable years beginning after December 31, 2024

- State conformity may vary, as some states may opt out of this enhancement.

Changes to Percentage of Completion Method (PCM) for Residential Developers

Background

Generally, long-term construction contracts must use the percentage-of-completion method (PCM) under IRC §460. Exceptions apply to specific home construction contracts and to small business taxpayers. Before the OBBBA, condominium projects were excluded from the definition of home construction contracts.

New Law

The OBBBA expands the home construction exception to include all residential construction contracts, including condominiums. Additionally, the qualifying construction period is extended from two years to three years.

Effective Date:

Applies to contracts entered into in taxable years beginning after July 4, 2025 (the enactment date).

Planning Considerations

- The provision applies only to new contracts entered into after enactment

- Residential developers, particularly condo builders, may be able to defer income recognition to better align with cash collections and settlement timelines

Excess Business Loss Limitation Under Section 461(l)

The OBBBA makes the excess business loss limitation permanent for non-corporate taxpayers for tax years beginning after December 31, 2026. The law also resets the limitation thresholds, effective for tax years beginning after December 31, 2025.

Limitation Amounts

- Base limitation reset to $250,000 (single) and $500,000 (married filing jointly), indexed to 2024 (instead of 2017)

Inflation-adjusted thresholds:

- 2025:

- $313,000 (single)

- $626,000 (married filing jointly)

- $313,000 (single)

- 2026:

- $256,000 (single)

- $512,000 (married filing jointly)

- $256,000 (single)

Planning Considerations

- These limits should be incorporated into ongoing individual tax planning

- Excess business losses continue to be carried forward as net operating losses, rather than being re-tested in future years

Individual Taxpayer Limitations

Even when property qualifies for 100% bonus depreciation, individual taxpayers may face restrictions on their ability to utilize the full benefit:

- Excess business loss provisions (now permanent) may limit annual deduction amounts

- Passive activity loss rules can restrict deductions for rental real estate and other passive investments

Strategic planning is essential to maximize the benefit of this provision within these structural constraints.

2025 Year-End Estate & Gift Tax Planning

As 2025 draws to a close, recent tax law changes—most notably under the One Big Beautiful Bill Act (OBBBA)—create meaningful planning opportunities for high-net-worth individuals and families. Proactive action before year-end can help preserve wealth, reduce transfer taxes, and improve long-term income tax efficiency.

Higher Lifetime Exemptions

Beginning in 2026, the federal estate, gift, and GST tax exemptions permanently increase to $15 million per person, indexed for inflation. This expanded exemption allows taxpayers to make larger lifetime gifts and remove future appreciation from their taxable estates.

Planning opportunity: Consider lifetime transfers of appreciating or hard-to-value assets (such as closely held business interests) to maximize exemption usage and estate tax efficiency.

Trust Planning Takes Center Stage

With higher transfer tax exemptions, income tax planning becomes increasingly important. Non-grantor trusts may be used to:

- Multiply available SALT deductions

- Expand QSBS exclusion benefits by spreading ownership among multiple trusts

Care must be taken to avoid IRS aggregation rules when establishing multiple trusts.

- Charitable Giving Timing – While the Pease limitation has been repealed, a new limitation on the tax benefit of itemized deductions begins in 2026.

- Planning opportunity – Accelerate charitable contributions into 2025 to maximize deductibility under current rules.

Family Wealth Transfer Techniques

- Properly structured intra-family loans continue to be respected as bona fide debt when formalities are followed.

- Portability elections require careful estate tax reporting to preserve a deceased spouse’s unused exemption.

- New reporting requirements apply to gifts or inheritances received from covered expatriates, potentially triggering tax at the highest estate tax rate.

2025 Year-End State & Local Tax Considerations

State tax landscapes shifted significantly in 2025. As all 50 state legislatures convened to finalize budgets, the result was a wave of widespread reform. Legislation spanned from income tax rate and apportionment adjustments to broadening the sales tax base. Compounding this, the federal tax reform passed in July created a ripple effect, adding significant complexity to taxpayers’ evaluations of their state liabilities.

Impact of Federal Tax Reform on State Taxation

The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, significantly alters federal tax rules, affecting many states because most states start with federal taxable income when calculating state taxes.

State Conformity Approaches

- Rolling Conformity: Some states automatically adopt federal tax changes as they happen.

- Fixed-Date Conformity: States that are locked into a specific Internal Revenue Code (IRC) date won’t automatically adopt federal changes unless their legislatures act.

- Selective Conformity: Some states pick and choose which federal changes to adopt.

Because many states completed their legislative sessions before the OBBBA was enacted, conformity decisions will vary widely, and many states will revisit conformity in 2026 or later.

Looking Ahead — Other Considerations

The potential phase-out of the U.S. penny and the implications for sales tax rounding rules, an issue that will require state or administrative guidance if it advances.

2025 Employee Benefits Update: Key Changes for Year-End Planning

As we approach 2026, significant employee benefit changes from SECURE 2.0 and the One Big Beautiful Bill Act (OBBBA) require immediate attention for year-end tax planning and 2026 preparation.

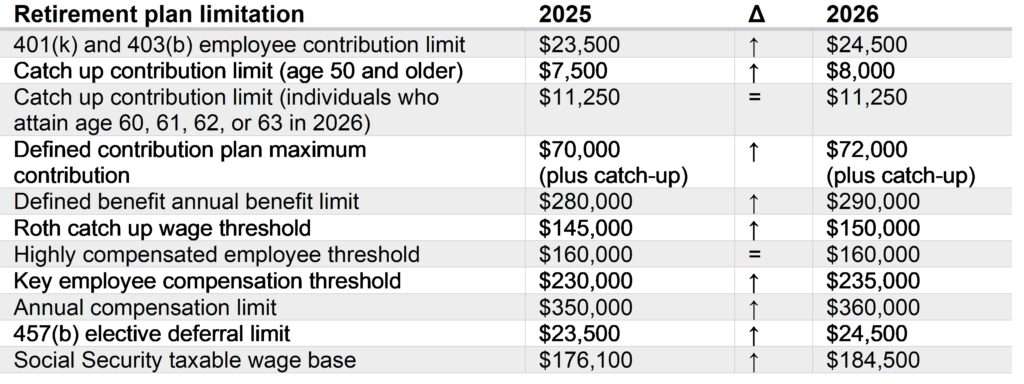

RETIREMENT PLAN CHANGES

Mandatory Roth Catch-Up Contributions (Effective Jan. 1, 2026)

- IRS final regulations confirm implementation date

- Applies only to employees earning over $150,000 in FICA wages during 2025

- Plans must offer Roth contributions to accept Roth catch-up contributions

- All participants 50+ must have the option, but only high earners are required to use Roth

- Action: Plans without Roth provisions must add them; existing plans may need amendments

Increased Catch-Up Contributions for Ages 60-63

- 2026 limit increases to $11,250 (up from standard catch-up)

- Plans offering regular catch-ups must be amended to allow higher amounts

- High earners in this age group must make increased catch-ups as Roth contributions

- Action: Review and amend plan documents; coordinate with payroll systems

2026 Cost-of-Living Adjustments Retirement plan contribution limits will increase for 2026 (specific amounts pending IRS announcement).

EMPLOYER-PROVIDED FRINGE BENEFITS

Student Loan Payment Assistance (Permanent – 2026)

- OBBBA makes tax-free employer contributions to employee student loans permanent

- $5,250 maximum exclusion indexed for inflation after 2026

- Action: Review and update educational assistance plans to include student loan payments

Moving Expense Reimbursements (Permanent Change – 2026)

- OBBBA permanently eliminates tax deduction for moving expenses

- Employer reimbursements remain taxable to employees (exceptions for Armed Forces/intelligence community)

- Action: Review relocation policies; continue treating reimbursements as taxable compensation

Qualified Transportation Benefits

- Bicycle commuting reimbursements permanently eliminated (effective Jan. 1, 2026)

- Monthly cap for transportation fringes and qualified parking increases to $340 (up $15)

- Action: Treat bicycle commuting as taxable; update policies for compliance

Employee Meals (Major Change – 2026)

- OBBBA eliminates employer deduction for meals provided to employees

- Includes office snacks, coffee, meeting meals, late-night dinners (previously 50% deductible)

- Employee events (picnics, holiday parties) remain 100% deductible

- Action: Evaluate whether employee meal benefits justify non-deductible costs

Dependent Care Assistance Programs (DCAP) – 2026

- Limit increases to $7,500 ($3,750 for married filing separately)

- NOT indexed for inflation going forward

- Action: Amend plan documents; update payroll systems; notify employees of increased limits

Health Care FSAs – 2026

- Pre-tax contribution limit increases to $3,400 (up $100 from 2025)

- Action: Update plan documents and employee communications

Paid Family and Medical Leave Credit (Permanent)

- Tax credit made permanent under OBBBA

- Credit based on wages paid during leave OR insurance premiums paid

- Expanded “qualifying employee” definition: employed 6+ months, 20+ hours/week

- Action: Review programs for OBBBA compliance; maximize credit eligibility

IMMEDIATE ACTION ITEMS

By Year-End 2025:

- Identify employees earning $150,000+ in FICA wages (subject to Roth catch-up mandate)

- Add Roth provisions to retirement plans if not currently offered

- Amend plans for increased catch-up contributions (ages 60-63)

- Update educational assistance plans for student loan payments

- Review and adjust employee meal benefit programs given the elimination of deduction

Early 2026:

- Coordinate payroll system updates for new contribution limits

- Communicate retirement plan changes to affected employees

- Update all benefit plan documents for OBBBA and SECURE 2.0 changes

- Ensure W-2 reporting reflects all benefit modifications

The convergence of SECURE 2.0 and OBBBA provisions creates both compliance obligations and planning opportunities. Key themes include mandatory Roth catch-ups for high earners, elimination of several employer tax benefits (moving expenses, employee meals, bicycle commuting), and expansion of others (DCAP limits, student loan assistance, family leave credits). Proactive plan amendments and employee communications are essential for smooth 2026 implementation.

Next Steps: Consult with your tax advisor to ensure all benefit plans are updated to comply with the new rules and optimized for tax efficiency.

2025 Year-End Planning Opportunity: Evaluating Section 1202 Benefits After the OBBBA

The One Big Beautiful Bill Act (OBBBA), enacted on July 4, 2025, significantly enhances the tax benefits available under Section 1202 for Qualified Small Business Stock (QSBS). These changes expand eligibility, reduce holding periods, and increase potential gain exclusions—creating meaningful year-end planning opportunities for founders, investors, and growing businesses.

Why This Matters Now

Year-end is an ideal time to:

- Confirm QSBS eligibility under expanded rules

- Review capitalization, asset levels, and equity issuances

- Structure late-year or early-2026 investments to maximize exclusions

- Start shortened QSBS holding-period clocks before year-end

Strategic action before December 31, 2025 can materially improve the timing and size of future tax-free exits.

Key Enhancements Under OBBBA

1. Shorter Holding Periods with Tiered Benefits

For QSBS acquired after July 4, 2025:

- 3 years: 50% gain exclusion

- 4 years: 75% gain exclusion

- 5+ years: 100% gain exclusion

Planning impact: Investors no longer need to wait more than five years to benefit, improving liquidity and exit flexibility.

2. Higher Gross Asset Threshold

- Aggregate gross asset limit increases from $50 million to $75 million

- Inflation-adjusted beginning in 2027

Planning impact: More companies qualify as “qualified small businesses,” expanding access to QSBS benefits and increasing potential exclusions under the 10x basis rule.

3. Larger Per-Issuer Gain Exclusions

For QSBS acquired after July 4, 2025:

- Per-issuer exclusion cap increases from $10 million to $15 million

- Indexed for inflation after 2026

The 10x basis limitation remains unchanged, but the higher $75 million asset cap increases the potential exclusion to $750 million, up from $500 million under prior law.

4. Broader Active Business Test

The active business requirement now includes:

- Domestic and foreign research & experimental expenditures

Combined with new R&E expensing rules, more companies are expected to satisfy QSBS requirements throughout the holding period.

Timing Matters

QSBS benefits are determined by the date the stock is acquired, not by the date it is sold.

- Stock acquired before July 4, 2025 remains subject to prior law (five-year holding period and lower exclusion limits).

- Stock acquired after July 4, 2025 qualifies for the enhanced benefits—even if sold years later.

Action Steps Before Year-End

- Review existing and planned equity issuances for QSBS eligibility

- Assess corporate asset levels relative to the new $75M threshold

- Consider accelerating investments to begin the three-year holding period

- Coordinate closely with tax advisors to avoid technical disqualification

The OBBBA materially strengthens Section 1202 as a tax-efficient exit strategy. With larger exclusions, shorter holding periods, and broader eligibility, QSBS planning is more valuable—and more complex—than ever. Proactive structuring and careful compliance are essential to capture these benefits fully.

Conclusion

If you have questions on how the above information may impact your tax situation, feel free to contact Huckbee CPA for a complimentary consultation.