As many small business owners are looking clarity towards applying for repayment forgiveness of their SBA Paycheck Protection Program (PPP) loans, on May 13, 2020 the Treasury Department finally released guidance providing a “safe harbor” from audits or penalties for businesses that received a loan that was under 2 million amount. The report also covered a number of frequently asked questions about the PPP loan program. I first read about this news from an article published in Allbusiness.com written by Neil Hare.

The guidance states the following:

“Any borrower that, together with its affiliates, received PPP loans with an original principal amount of less than $2 million will be deemed to have made the required certification concerning the necessity of the loan request in good faith. SBA has determined that this safe harbor is appropriate because borrowers with loans below this threshold are generally less likely to have had access to adequate sources of liquidity”

The author Mr Hare wrote that previous to this guidance, many companies were worried that under the “good faith” certification requirement on the PPP lending application, they would be subject to SBA or Treasury audits and potential penalties and damages. The PPP loan application requires the borrower to certify in “good faith” that they are requesting the loan due to “economic uncertainty,” and that they have no access to credit elsewhere. Traditional SBA loans require written documentation that the borrowed tried and failed to access credit from other sources.

The original intent for Congress and the Trump Administration when passing the PPP loans was twofold: First, give small business the funding necessary to survive the Coronavirus shutdown, which the federal government estimated would last two months. That is why the loan amount was based on your average 2019 monthly payroll multiplied by 2.5%, and forgiveness is largely based on two months of payroll. Second, to keep workers employed and on payrolls instead of sending them to the unemployment line.

While these two reasons behind the loans had purposeful intentions, they were misguided from the start and are now causing heartache for many small business owners. From day one, it was clear that forcing small business owners to keep workers on the payroll when they were effectively shut down with little or no revenue put them in the position of the unemployment office. The unemployment benefits program was also enhanced in the CARES Act to cover workers, and while no business ever wants to lay off good employees, there simply are times when that is necessary for survival.

The result of the PPP confusion is that billions of dollars remain untapped, so if you haven’t yet applied and still need the money, do so immediately. And the negative press of many large companies such as Shake Shack, Ruth Chris Steakhouse, Sweetgreen, the LA Lakers receiving loans that were meant for help small businesses, had a chilling effect in which the flow of loan applications and amounts requested slowed down, leaving many billions of dollars left in the program, for better or worse. This is partly because smaller firms are finally in the banks queue for PPP loans, which is good, but the entire point of the program was to introduce liquidity into the economy and to protect workers’ wages. Therefore, having this money sit on the sidelines is not helpful to businesses, workers, or the U.S. economy. I assisted a few of my clients to go through the paper work for getting this loan approved and it was sort of headache at times.

Here are a few of the most frequently asked questions about loan forgiveness starting with the most pressing one about borrower liability:

What is my liability exposure around the loans and forgiveness?

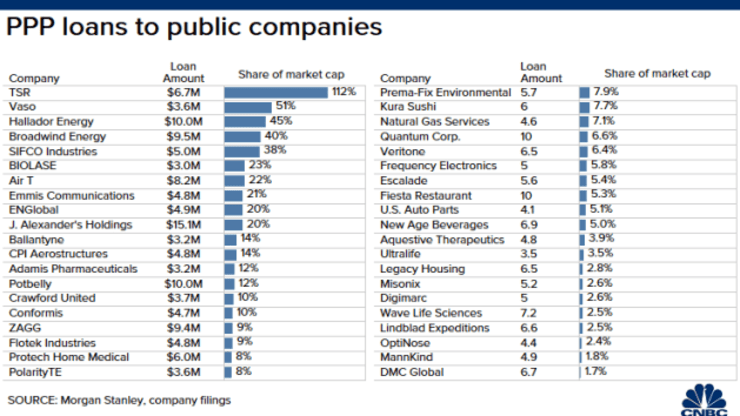

As you likely saw reported in the media, some major brands applied for and received PPP loans that was supposed to earmarked for small business. Large restaurant chains, hotel operators and energy companies to name a few. How did this happen? According to reporting from the CNBC, the Paycheck Protection Program offers forgivable loans to business with 500 or fewer employees. Companies can secure loans of equal to 2½ times their monthly payroll, up to $10 million. The law makes an exception for some companies — namely, those with a North American Industry Classification System code of 72, which covers businesses in the accommodation and food services industries. Such businesses that have more than one physical location, but which don’t employ more than 500 people per location, are eligible for loans through the Paycheck Protection Program, according to the Coronavirus relief law.

(image credit: CNBC)

While all the companies and organizations seemed to have met the criteria for the PPP loan, some the Trump Administration and the court of public opinion and bad press scrutiny determined they did not meet the “spirit of the law,” and many returned the funds. The CARES Act offered loopholes for borrowers who have more than 500 employees and waived the “Credit Elsewhere” test (with typical SBA 7(a) loans, borrowers must document they can’t access capital from other sources).

The PPP loans did not require this documentation, but put the onus on the borrower to show “good faith” that they needed the loans despite access to other sources of capital. Mr Hare pointed out that in the answer new May 13, Treasury guidelines to question 31 stated the following:

“Specifically, before submitting a PPP application, all borrowers should review carefully the required certification that “[c]urrent economic uncertainty makes this loan request necessary to support the ongoing operations of the Applicant.” Borrowers must make this certification in good faith, taking into account their current business activity and their ability to access other sources of liquidity sufficient to support their ongoing operations in a manner that is not significantly detrimental to the business.”

This somewhat vague standard has made many small businesses nervous that they will not meet this “good faith” test, and will have to repay the loan or worse, suffer penalties—perhaps even criminal penalties. So, what should you be worried about with the “good faith” standard? Steve Mnuchin explained that companies that have received over $2 million in loans will be automatically audited by the SBA and Treasury to determine if this standard was met.

So if your business was received under $500,000 or perhaps even under $1,000,000 in PPP loans, it is highly unlikely this audit will occur and you will face any liability. It is important to remember, it is your lender who will review documentation after 8 weeks to determine forgiveness based on use of funds; 75% for payroll and 25% for rent, utilities, and interest payments. Lenders are working towards an easy mechanism to approve forgiveness of most loans “at the push of button” and forsake lengthy reviews.

This being said, it is probably a good idea to document the state of your business and your need on or around the date you applied for the PPP loan. If you are a retailer or restaurant, the simple fact of being shut down as shelter in place should enough, and for any business, the reality of lost future sales, canceled orders, and uncertainty about the length of the shutdown should suffice to show “good faith.” Just remember, the government and the banks want these loans forgiven, so presuming you used the funds appropriately, that should be the case.

Do I have to use at least 75% of the PPP loan on payroll?

That is how congress wrote the legislation, the intent of the PPP loan program was to help companies temporarily keep their employees on their payroll and not file for unemployment. It would make sense for business owners to have some freedom to allocate these funds to use as they see fit on major expenses such as rent, but Congress chose to earmark ¾ of it for payroll instead. And while many associations and business groups have tried to lobby to reduce the percentage used on payroll to 50%, but that is not something to can bank on changing. So to make sure your lone gets forgiven make you comply with using 75% of the loan proceeds on your payroll.

If I laid off workers, do I need to rehire the same employees oe positions to meet the payroll requirement?

You have some leeway here. Your bank is not going to check to see if you hired the same employees back or which exact positions you filled. They are only going to look at the amount of your payroll to that it is the same or greater than the 2019 average upon which the loan amount was based. The author My Hare points out that even if you extent offer to an employee who rejects it “you may want to ensure the correspondence is in writing for future reference. But, even if that employee rejects your offer for reemployment, your obligation to use the PPP funds on payroll remains based on the 2019 numbers.” Another thing to point out you can hire other positions. For example, if you have been shutdown temporarily you could choose to hire a web developer to revamp your website instead of rehiring a sales person. You also have the flexibility to could shift roles and responsibilities of existing employees to meet the needs of your changing business model. Keep in mind; the position must be a full-time employee and not a contractor in order to count towards forgiveness.

What documentation should I use with my lender to show the money was spent according to the PPP program regulations?

The easiest solution would be to reach out to your outsourced payroll provider, such as Gusto or ADP, to prepare reports showing the funds were used for payroll. It should be as simple as that. In addition, provide bills and canceled checks for your rent, mortgage, utilities, or interest payments if you used the funds for those purposes. If you don’t use a payroll company, then follow the outline of a Schedule C form with backup documentation to show how the money was spent. This can include canceled checks, bank transfers, and the payment of acceptable expenses. It is recommended that should reach out to your payroll provider now and start documenting these expenses. If your CPA firm handles your payroll they can help you with this.

If possible, it is also advisable to keep PPP funds in a separate bank account and make all forgivable expenses out of this dedicated account.

When should I apply for forgiveness?

Most banks or lenders will begin processing forgiveness applications at seven weeks from fund disbursement date. It is recommended to reach out to your banker now to confirm this and to double-check on what documentation your particular lender will want to see. Again, the lender will make the decision on forgiveness. Update according to an article in Entrepreneur, on Friday evening, May 15, the SBA released the Paycheck Protection Program (PPP) Loan Forgiveness Application and clarified a few critical definitions and documentation requirements in their instructions, unfortunately no there was no additional guidance issued by the Treasury to go with it. Since the SBA released the PPP loan forgiveness application (an 11 page pdf), it is causing a lot of confusion according to reporting from Fortune Mag. Many CPA firms were expecting regulatory guidance, not just a form. Many businesses are banking on getting that crucial forgiveness for their loans. Otherwise, they’ll have a 1% loan to pay back over two years. I recommend you read the Fortune article since its covers the questions that were answered and the ones that still need more clarification.

The application has four components:

1. PPP Loan Forgiveness Calculation Form

2. PPP Schedule A

3. PPP Schedule A Worksheet

4. PPP Borrower Demographic Information Form (optional)

The accounting software company Bench put out a guide on how to fill out your forgiveness form correctly.

Like the Borrower Application to obtain the loan, the Forgiveness Application includes borrower certifications that should be reviewed with legal counsel or a certified CPA advisor.

Conclusion

Now there has been a lot of criticism of how the PPP program worked especially since many larger companies seemed to get preference if they had a better relationship with their lender or more lawyers to fill out the required paper work. While there still may a few clarifications needed from the PPP loan program, most of it is relatively straightforward and probably won’t change that much. Clearly the businesses that were forced to shutdown or customer demand dropped because of the pandemic, the need for the funds is clear and if the money is used on payroll as intended, it will be forgiven without any liability concerns. As the billionaire investor Mark Cuban recently recently said according to the Hill, that the Paycheck Protection Program (PPP) did not achieve its goals. “It’s time to face the fact that PPP didn’t work. Great plan, difficult execution. No one’s fault. The only thing that will save businesses is consumer demand. No amount of loans to businesses will save them or jobs if their customers aren’t buying,” Cuban tweeted Monday. For the companies that did receive the loan funding which I assisted a few of my clients to get them approved it was a decent source of short term capital till the end of June. Depending on how long this pandemic continues or how slow the reopening will happen forcing businesses to run on reduced capacity, companies should maybe start exploring additional sources of capital if possible. If any company has questions about the loan forgiveness application feel free to contact Huckabee CPA for a free consultation.