(image credit:vox)

Are the current GAAP financial statements reporting methods failing to capture the value created by digital companies who invest heavily and spend to gain market share and new growth? On May 10th, 2019 Uber Technologies Inc, went public on the New York Stock Exchange at a price per share of $45, lower than expected, valuing the company at about $82 billion, despite reporting losses at $1.8 billion for 2018. In 2013 Twitter reported losses of almost $79 million before its IPO, yet it still had a valuation of $24 billion and continued reporting losses over the next four years. In 2016 Microsoft made its largest acquisition of $26 billion to date for Linkedin that also reports losses. Back in 2014, Facebook paid a whopping $19 billion for the text messaging company WhatsApp that had no profits or revenue. On the opposite end of this spectrum, in 2018, the NYT’s reported that the Industrial behemoth General Electric’s stock price was down over 44%, as it reported its first loss in almost 50 years. Why does this matter?

In 2018 three professors from the Columbia and Dartmouth business schools Vijay Govindarajan, Shivaram Rajgopal, Anup Srivastava, co-wrote and published an article in the Harvard Business Review titled “Why Financial Statements Don’t Work for Digital Companies.” And they posed the question, “Why do investors react negatively to financial statement losses for an industrial firm but disregard such losses for a digital firm?” This makes it seem that current financial statements appear to fail to capture the value created by modern digital companies. They reference NYU Stern Professor Baruch Lev’s 2016 book called “The End of Accounting” that states that for the past 100 years or so, “financial reports have become less useful in capital market decisions.” And in the article, they go on to claim from their research that traditional accounting earnings are virtually inconsequential for digital and technology organizations. They suggest that the current financial accounting models or rules fail to capture the principal value driver for tech companies: which is increasing returns and scaling their intangible assets.

In line with this month’s article about financial statements, let’s dive a little deeper into the balance sheet and income statement. For a manufacturing or industrial company that mostly deals with physical goods and assets, using the balance sheet can present a pretty straightforward view of productive assets. The income statement shows an excellent estimate of the expenses required to create shareholder value. The difficulty comes with trying to use these types of financial statements to understand the value of tech or digital company.

The Balance Sheet

In order to report assets on the balance sheet, they have to physical, they have to be owned by the corporation, as well as being within the business’s confines. The problem is for many technology or digital corporations, is that most of their assets are considered intangible (data, software, trademarks, goodwill, technologies, brand name, patents, etc.) in nature and many have built out large ecosystems that extend out beyond the companies own parameters. The HBR author Vijay Govindarajan cites examples of some of the Fang companies products. He said, “consider Amazon’s Buttons, and Alexa powered Echo, Uber’s cars, and Airbnb’s residential properties, for example. Many digital companies have no physical products and have no inventory to report. Therefore, the balance sheets of real and digital companies present entirely different pictures.”

But if we were to compare the retail giant Walmart’s $116 billion of hard assets to its $312 billion market cap valuation against Facebook’s $13 billion of hard assets to its 535 billion valuation. The fundamental core business models for technology and digital companies are comprised of organizational strategy, technology research and development, products, brands, ecosystem and vendor networks, social and customer relationships, computerized databases and software, human capital (engineers, scientists’ and software workers’ and product development teams, salespeople, managers etc).

The economic reasons or purpose for all of these more intangible investments are no different from that of an industrial manufacturing company’s tangible investments in buildings and factories. When a tech company, investments in their furthering growth of business models or products (intellectual property, software investments, staff and managerial expertise, R&D, market research, advertising, business processes, organizational structures, database development, etc) they are not capitalized as assets (right away or many years), they get treated as expenses in the calculation of profits in that current earnings period. Basically, the more a digital startup (or now public) invests in building its future in innovative ideas or sometimes risky project bets that have lottery-like payoffs, the higher its initial reported losses will be. People that invest in technology or digital business model companies often have no choice but to disregard earnings in their investment decisions.

Bryce Coward of Knowledge Leaders Capital said: “digital companies tend to be less tangible capital intensive and more intangible capital intensive than older firms, which creates a big problem for financial analysts because accounting rules explicitly treat tangible and intangible capital investments differently.”

These professor researchers found that “intangible investments have surpassed property, plant, and equipment as the main avenue of capital creation for U.S. companies,” and yet all these intangible assets are absent from the balance sheet, which significantly hinders analysts from forming correct opinions about digital companies’ earning potential. It almost makes the balance sheet just an artifact of regulatory compliance with little value for potential investors. They noted that banks are starting to be less reliant on company balance sheets for making a lending determination because they heavily rely on asset coverage to calculate their security. What is interesting is that companies can report M&A brand acquisition purchases and intangibles as assets on the balance sheet. This then adds confusion to the earnings and assets of digital companies that rely on organic growth vs. acquiring competitors.

Things may change as more digital transformations happen

As more technology and digital business, companies take larger portions of GDP and as older legacy (more physical) companies go through digital transformations in parts of their operations; income statements might become less useful for investor analysis. They find that “earnings explains only 2.4% of the variation in stock returns for a 21st-century company — which means that their annual earnings do not explain almost 98% of the difference in companies’ annual stock returns “.

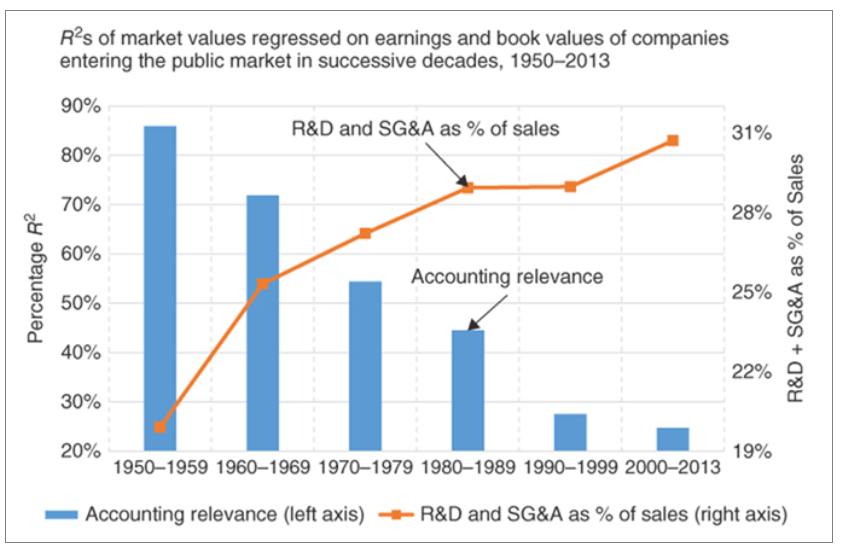

In Professor Baruch Lev’s “End of Accounting” book found that variations in financial metrics like earnings and book value can explain 90% of the variations in stock prices for companies that came public between 1950-1959, compared to around 20% for companies that have come public since 2000 (chart below).

(image credit: Knowledge Leaders Capital)

These professors think that current financial accounting models are flawed for technology businesses in another way. In an article titled “can anyone stop Amazon from winning the industrial internet,” they claimed that as physical assets depreciate with use, intangible assets may become more valuable with use. Think about social networks such as Facebook or Instagram: both of the companies value increases as more people use their products because the benefits increase to an existing as a new one joins the network. Their growth and company value has powered the system or network they have in place not increments of operating costs. That is why many digital businesses will aim for market leadership, creating network effects, and achieving Silicon Valley’s winner-takes-all profit business models. In another HBR article titled “A Blueprint for Digital Companies’ Financial Reporting,” these professors state “a company’s first positive revenues indicate the acceptance of its product or services by customers. When multiple players compete for the same space, revenues indicate the progress towards achieving market leadership that creates the dominant protocol for industry partners, suppliers, and customers.” With Facebook’s dominance in social media users and advertising, it achieved a whopping gross margin of 76% on its 2017 revenues of $46 billion, which then creates extra shareholder value for every additional dollar of revenue that comes in. If we compare them to Yelp’s 2017 revenues of $0.8 billion or Twitter’s 2017 revenues of $2.4, you can a stark contrast to companies that are not are the winner-take-all profit level.

Again there is not an accounting measure for concepts such as “network effects,” or even the increase in value of an intangible resource can get with use. Meaning these digital companies that leverage using networks ecosystems and software products to increase returns as it scales with users goes against the basic principle of financial accounting (that tangible assets depreciate with use over time). So all the big management consulting firms such as Accenture, Mckinsey, Deloitte, and others are mostly built on leveraging intangible assets such as human capital. But current accounting rules make it difficult to measure the disruptive digital companies that get increasing returns as their idea-based platforms scale with users. Let’s take Google, for example, can service millions of clients from different product lines from the same office building by just adding more server capacity because everything is cloud and digital software based (now they, of course, higher people more people as well). But take large accounting or audit firms such as PWC or KPMG, for them to dramatically increase client revenue they would need to hire more professional consultants and open more offices usually. And for professional service firms, most of their client billings are attached to employee wages, and that is reflected to match currently reported revenues. Meaning if you look at their income statements, they should reliably show the surplus or profit created in that accounting period, which is similar for many non-technology based companies.

But for digital and technology companies such as Uber, Slack, Airbnb, Facebook, Twitter, the majority of the costs of developing an idea-based software platform are reported as an expense in the beginning years, when they are in a growth mode and show little revenue. Once they achieve product-market-fit with their platform and start bringing in revenues, they have a lot fewer expenses to report. The HBR article authors conclude that in either phase, “the calculation of earnings does not reflect the true costs of revenues.”

How important are earnings reports in the digital era?

The HBR article authors ask another question “If earnings are so meaningless, then why do investors react positively to rumors concerning a digital company turning profitable?”

Back in October of 2017, Twitter announced that it was finally going to show a profit, and the financial news caused its share price to increase by 20%. And back in 2014 Yelp eventually turned a profit as well and the news made the stock rise by 8%. Did investors make the assumption that both of these companies finally matured past their growth and investing phase, and had achieved increased customer market share, or would they even now be headed towards the winner-take-all monopoly status?

Well, these hypothetical questions contradict the whole “earnings have valuable info” argument. And another reason could be that when investors believe in the growth story, market share potential, disruptive technology or idea behind a digital tech company (such as Netflix and Tesla) the initial losses or “burning thru capital” may be part of the risk of investing.

What are CEOs supposed to do?

If income statements do not fully convey the value created by the tech company, or the balance sheet is not showing the actual value of the company’s resources, CEO’s maybe starting to wonder what should we be reporting? The HBR article authors say there are some common questions they hear fairly often, such as:

- What does preparing and auditing accrual-based financial statements achieve?

- Wouldn’t digital companies be better off by only reporting a summary of their cash transactions?

- What can digital companies do to enhance the informativeness of their financial statements?

Are the accounting standards going to be changed to allow digital companies to capitalize their intangible investments? Not too likely. And even if tech companies were able to capitalize on their intangibles, when you recalculate the profits of assets would it truly justify some of the current crazy market valuations of digital businesses.

The same professors Vijay Govindarajan Shivaram Rajgopal and Anup Srivastava wrote another very insightful article called “Why We Need to Update Financial Reporting for the Digital Era.” All hope is not lost in corporations finding ways to show their real value or worth to potential investors. These professors’ research work found that investors can find useful signals by analyzing successful tech companies business models. They analyze things such as distribution partnerships, marketing, technologies, acquisition of major customers, the launching of new products and services, new subscriber counts, revenue per subscriber numbers, customer churn, and the geographic market areas of customers. In 2003, the Securities and Exchange Commission (SEC) established new guidance for technology companies such as Facebook to list this type of information in their “Management discussion and analysis (MDA)” item section of their SEC filed the annual report.

If your company creates a value relevant development, it’s better to put out a press release immediately then waiting for listing it on your 10k form report. Releasing information or disclosures on strategic ecosystem vendor partnerships, new products or services, increased web traffic, network advantages are considered “value-relevant” information to potential investors.

When an investor understands all your companies non-financial advantage indicators, then financial performance statements can become more value relevant. Tech companies can provide more detailed information on all the intangible investments made by the company – even if it can’t be verified by an audit – by reporting these investments into different categories. Such as:

- customer relationship and marketing

- information technology and databases

- talent acquisition and training

Large tech software companies such as Salesforce, Amazon, Microsoft, Oracle, Google, Facebook, Twitter will make M&A acquisitions of other technology startups each year for several reasons, for the patents, the technology, the talent team, the customers, or as a defensive play. And as the article titled “the real value of intangibles” stated “In conventional accounting, intellectual capital and other intangibles appear on a company’s balance sheet only in the course of an acquisition, as “goodwill” — the lump-sum difference between the amount a buyer paid to acquire another company and the book value of the acquired firm or its acquired shares. This amount generally represents the value that a company has accrued by way of its brand, reputation, customer service, and other nonphysical assets.” Google did not just pay $2.6 billion for the business intelligence company called Looker to acquire its physical assets.

Conclusion

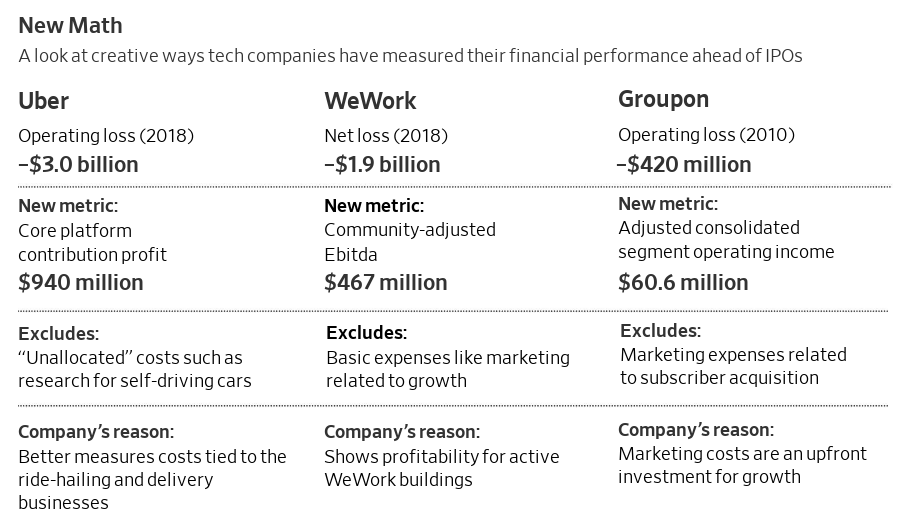

To summarize all this, as more legacy companies continue on their digital transformation journeys and spend more on intangible investments, and as digital technology businesses come to become the new face of corporate America, they will also have to drastically shift the manner and ways by which they convey their value to outside investors. Some companies such as Uber, Lyft and Wework are already trying to do just that. According to Seeking Alpha, Lyft is making an optimistic “contribution” tweak to the accounting lexicon. In a recent by Rolph Winkler in the WSJ titled “Uber and Lyft Get Creative With Numbers, but Investors Aren’t Blind to the Losses” noted that tech startups are starting to use unconventional financial terms like “contribution profit”, “annual recurring revenue,” “billings” and “bookings” that can give a more favorable impression than traditional accounting would. Many startups try to argue these nontraditional metrics are better measures for understanding the growth trajectory of their businesses. Rolf mentions ” Venture capitalists often place a premium on startups that can grow quickly, ignoring some upfront expenses. Marketing costs, for example, might push companies into the red at first, but if customers who sign up are highly profitable in the long run, the losses would be worth the investment today, venture capitalists and entrepreneurs say.” It’s sort of like they are saying “this is how profitable we would be if we stopped trying to grow and let our business cruise, not everyone agrees.” Seeking Alpha author said.

(image credit: WSJ)

All these companies spend heavily to increase market share and enter new areas. Only time will tell if these startups can try to convince investors by using non-GAAP financial terms on their road to growth and eventual profitability. Thomas Huckabee CPA provides accounting services for technology companies in San Diego, and if you have any questions, feel free to contact us for a free consultation.