Since the end of March of 2020, working professional taxpayers have moved to working remotely from their homes and often turning their living rooms, bedrooms, kitchens and various other rooms into temporary makeshift offices. And with this WFH trend still going on and could actually continue for the foreseeable future, a question that is now coming to people’s minds is “whether or not a home office deduction is now available?”

The CPA firm BakerTilly covered this topic back in October. According to Turbotax “many people whose small businesses qualify them for a home office deduction are afraid to take it because they’ve heard it will trigger an audit.” But if you deserve it, take advantage.

This blog article will go over the necessary requirements to be able to qualify for this tax deduction on a tax return and feel at ease doing so.

Business use of home

As a general rule, certain taxpayers can deduct business expenses related to their personal residence for space used exclusively and regularly in connection with a trade or business. Self-employed small business owner taxpayers or individual partners in partnerships can qualify. Employees working from a home office are no longer eligible to take a home office deduction. Why? This itemized deduction was suspended from 2018 through 2025 to help “pay for” the doubling of the standard deduction under the Tax Cuts and Jobs Act (TCJA).

So to meet the eligibility requirements for taking a home office deduction, a space needs to created that is exclusively used (and is principal location) to meet with clients, patients or customers in the normal course of business, or is where management or administrative functions (for example billings, maintaining books and records, ordering supplies, making calls, scheduling appointments etc.) are conducted. If business duties are occasionally done at over locations, which can include hotels or at a customer site, will not necessarily reject the taxpayer from qualifying for a home office deduction. Daycare centers have their own specific rules.

Generally speaking, to qualify for the home office deduction:

- Exclusive and regular use: You must use a portion of your home exclusively and regularly for your business.

- Principal place of business: Your home office must be either the principal location of that business, or a place where you regularly meet with customers or clients.

- Exceptions: Some exceptions to these rules, such as for daycare and storage facilities, are discussed below.

Exclusive use

The biggest roadblock to qualifying for these deductions is that you must use a portion of your home exclusively and regularly for your business.

-

- The office is generally in a separate room or group of rooms.

- The office can also be a section of a room if the division is clear—thanks to a partition, perhaps—and you can show that personal activities are excluded from the business section.

The law is clear and the IRS is serious about the exclusive-use requirement. Say you set aside a room in your home for a full-time business and you work in it ten hours a day, seven days a week. Let your children use the office to do their homework, though, and you violate the exclusive-use requirement and forfeit the chance for home-office deductions.

The exclusive-use rule doesn’t mean:

You’re forbidden to make a personal phone call from the office.

You have to rush outside whenever a family member needs a moment of your time.

Although individual IRS auditors may be more or less strict on this point, some advisors say you meet the spirit of the exclusive-use test as long as personal activities invade the home office no more than they would be permitted at an office building.

Regular use

There’s no specific definition of what constitutes regular use.

Clearly, if you use an otherwise empty room only occasionally and its use is incidental to your business, you’d fail this test.

If you work in the home office a few hours or so each day, you’d probably pass.

This test is applied to the facts and circumstances of each case the IRS challenges.

Home Office Deduction Expense Requirements (direct vs indirect)

Once you have determined that as a taxpayer you can qualify and take the home office deduction, next you have to divide certain expenses business and personal use. Now remember that personal expenses cannot be used in the calculation or computation. So expenses or costs that are directly associated with the trade or business, such as construction, repairs or painting of the business office space, would be considered deductible in full as a home office expense. Now indirect expenses, which includes rent (if the taxpayer does own it), homeowners insurance, utilities, are allocated to the home office using the percentage of the home being used for business (which is generally determined thru a square-footage allocation.)

The same percentage of mortgage interest and real estate taxes would be deducted as part of the home office deduction instead of an itemized deduction on Schedule A.

Another added bonus is that homeowners can also now depreciate (which would account for the normal wear and tear of the building structure not the land) the office used for the business part of the home. Also permanent improvements that were made to make the home office can also be depreciated also. Remember when you go to sell the home that depreciation of the home office has to be recaptured as ordinary income once it is sold. Meaning, the cumulative amount of depreciation deducted is not eligible for the primary residence sale exclusion.

Another thing to understand is, that the home office deduction is limited (using a formula) if total business expenses are less than the gross income. In other words, home office expenses can’t create a tax loss to shelter other income. Any carryover can be deducted the following year subject to the same limitation. In addition, special rules exist when taxpayers operate more than one business in the home or have more than one place of business.

How to calculated the home office business deduction

Your home office business deductions are based on the percentage of your home used for the business or a simplified square footage calculation.

Business percentage of house method:

The most exact way to figure this proportion is to measure the square footage devoted to your home office and find what percentage it is of the total area of your home.

If the office measures 150 square feet, for example, and the total area of the house is 1,200 square feet, your business percentage would be 12.5%

150 square feet ÷ 1,200 square feet = 0.125 (12.5%)

An easier way is acceptable if the rooms in your home are all about the same size. In that case, you can figure the business percentage by dividing the number of rooms used in your business by the total number of rooms in the house.

Simplified method

A few years ago the IRS introduced the simplified method to which was supposed to ease up the burden of recordkeeping for the taxpayer for determining the home office deduction amount. Instead of tracking separate expenditures of the home as described above, merely multiply $5 by the allowable square footage of the business portion of the home (using the smaller of 300 square feet or the actual space). The deduction cannot exceed the net income (receipts less non home-related expenses) from the business use of the home. Using this method means taxpayers do not need to adjust the amount of mortgage interest or real estate tax reported on Schedule A when itemizing deductions. The home office space is also not depreciated under the simplified method (meaning no recapture is necessary upon subsequent sale).

Taxpayers can switch between choosing to use the actual expenses one year and then use the simplified method in another year. But remember, that any carryover of actual expenses cannot be used in a tax year when the simplified method is used to compute the home office deduction. So just remember that with either method, the qualification for the home office deduction is determined each year.

IRS Guidance

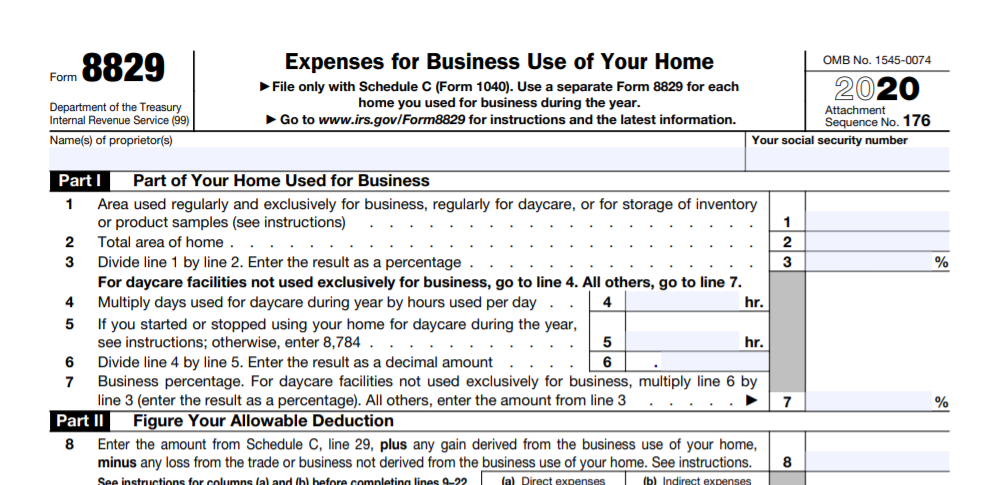

The IRS has several resources available to assist taxpayers in taking advantage of the home office deduction. Form 8829, Expenses for Business Use of Your Home, with its instructions, along with Publication 587, Business Use of Your Home, and FAQs – Simplified Method for Home Office Deduction can all be used to help determine eligibility and calculation.

Conclusion

The home office deduction is not a red flag for an IRS audit. Whether you qualify for this deduction is determined each year. Deducting a home office is treated differently depending on your business type. The simplified method can make it easier for you to claim the deduction but might not provide you with the biggest deduction. If you are a business owner that created a remote home office space this year, and if you are eligible for home office deductions, the tax savings can be well worth the additional work required to qualify. If you have a questions feel free to contact Huckabee CPA for a consultation about your specific situation.