A recent article published in CFO.com mentioned that NFIB Chief Economist Bill Dunkelberg had recently stated that “with small business owners’ views about future sales growth and business conditions dismal, some small business owners want to hire and make money now from solid consumer spending.” Since the economic data of U.S. retail sales rose 0.7% in July, beating expectations, suggesting continued consumer resilience.

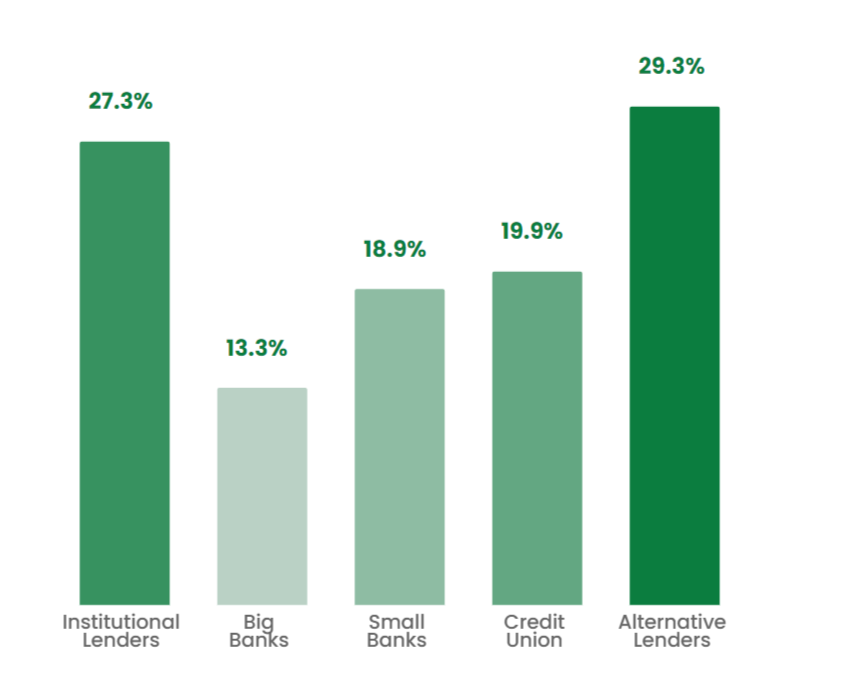

The problem is, with the regional and larger banks being under pressure, it is making it more difficult for small business owners who are looking for sources of short-term capital or credit to get approved for it. A Forbes contributor Rohit Rora, recently wrote about this issue explaining that according to the latest Biz2Credit Small Business Lending Index report , Small business loan approval percentages at big banks dipped from 13.5% in April to 13.4% in May. And the approval ratings at small banks remained at 18.7%. Meaning financing and lending to small businesses has tightened dramatically since last year.

(Image Credit: Biz2credit)

Banking credit crunch

The Forbes gives a pretty explanation into the banking problems. The cheap money is gone. So economics of the FED hiking rates for the past year or so, have raised the cost of capital. Banks are struggling to attract new deposits and having to offer higher interest rates to secure those deposits. This squeeze on both ends makes banks reluctant to lend. The banking industry started tightening lending standards last year.

Then the high-profile collapses of Silicon Valley Bank, Signature Bank, and First Republic Bank earlier this year sparked liquidity worries across the industry. In the wake of these bank failures, small and midsize institutions are losing deposits to large banks seen as safer havens. The combined impact leaves banks less willing to lend especially to small businesses which they see as a higher risk.

According to the Fed’s Senior Loan Officer Opinion Survey (SLOOS) on Bank Lending Practices, the study reported that lending policies tightened for commercial and industrial (C&I) loans to large, midsize and small firms in the first quarter of 2023. Meanwhile, banks reported weaker demand for all commercial real estate (CRE) loan categories.

Why have banks decided to approve less loans?

According to the Fed, they cited an uncertain economic outlook, reduced tolerance for risk, deterioration in collateral values, and concerns about banks’ funding costs and liquidity positions. The banks also reported concerns about funding costs, liquidity positions, and deposit outflows as reasons for tighter lending standards for the rest of 2023. Therefore banks have become worried about falling asset values and deteriorating credit quality. Thus, they have a reduced tolerance for risk, which has curtailed their aptitude to grant new loans.

A Federal Reserve survey released in May found small businesses need credit to expand, cover operating costs, make repairs, replace assets, and refinance or pay down debt. The Fed’s Small Business Employer Survey said these firms typically obtain financing through big banks, small banks, online lenders, and other sources. Credit is in demand among small business employers for a variety of common financial needs.

Some companies have used the ERC program for funding

The CFO.com article mentioned that some small businesses took advantage of the Employee Retention Credit (ERC), a tax incentive fueled by the pandemic that offers credits of up to $26,000 per retained employee for qualifying wages, has been used as a source of capital by small businesses affected by the pandemic. To file a claim for 2020, a company must do so by April 2024. Claims for 2021 are due a year later. The ERC program, unfortunately, has been plagued by fraudsters offering small businesses “easy money.”

SBA Loans might be the best option at the moment for small businesses but it’s not cheap

With residential mortgage interest rates above 8 percent, SBA loan programs might be only option from the banks. However, the rates on 7(a) loans are up to about 12% currently, and they take up to two months to process. Businesses that need money quickly are searching online and turning to alternative lenders, which offer capital at even higher interest rates than the banks do. Borrowers pay for the speed of the transaction and the increased risk the lenders are taking during turbulent times.

The CFO.com article mentions another option from a company called Newity, which offers access to working capital loans through the Small Business Administration’s 7(a) program. Newity’s niche is loans of $250,000 and under, too small for a bank, and rates run at prime plus 275 basis points, or currently about 11%. In the cureent fiscal year, SBA lenders — many of them banks — have approved more than 46,000 loans totaling about $22 billion.)

For the 7(a) loans, used for working capital, personal and business credit scores and number of years in business drive the underwriting.

Conclusion

Even in economic boom times, small businesses had a hard time qualifying for a bank loan, and now is not the best of times. Having a solid business credit profile is not a guarantee for getting qualified to securing financing for your business. But it opens up more options then compared a business that has a bad business credit profile.

In addition, robust hiring at small businesses may be starting to slow. According to Bank of America’s internal data, small business payroll payments per client were up 2% year-over-year in June, a slight moderation from 3% growth the prior month. Payments have been on a downward trend since early 2022.

With full employment, high labor costs, and rising oil prices, the Fed likely will not back away from rate hikes any time soon.

The takeaway being that going forward small businesses who are looking to working capital loans at this time might have fewer options, and it could take a while for this credit crunch to improve.