Understanding their tax implications is essential for business owners as cryptocurrencies become increasingly integrated into mainstream financial systems. Cryptocurrencies are treated as capital assets, and any transaction involving them—whether selling for fiat currency, trading one cryptocurrency for another, or using crypto to purchase goods and services—is considered a taxable event. The IRS requires these transactions to be reported based on their fair market value at the time of the transaction, which determines the applicable capital gains tax.

Key considerations for business owners include:

- Capital Gains Tax:

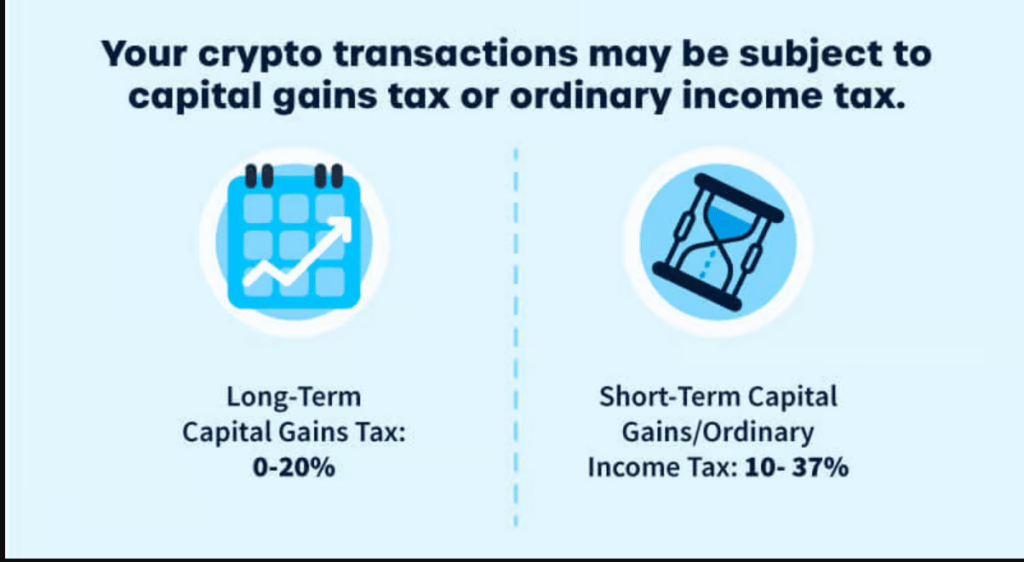

- Assets held for more than one year qualify for lower long-term capital gains tax rates.

- Assets held for a year or less are subject to short-term capital gains tax, with rates up to 37%.

- Crypto Income:

- Payments in cryptocurrency, staking rewards, and mining income are classified as ordinary income.

- This income is taxed at standard income tax rates and may also incur self-employment tax.

- Record-Keeping:

- Maintain detailed records of transaction dates, fair market values, and cost bases.

- Accurate documentation helps ensure compliance and identify potential deductions or credits.

- IRS Compliance:

- Stay updated on evolving IRS guidelines and cryptocurrency tax laws.

- Non-compliance can result in substantial penalties and interest.

Consulting a crypto tax expert or using reliable tax software can help business owners navigate these complexities, meet all tax obligations, and remain compliant. By proactively managing cryptocurrency tax responsibilities, business owners can optimize their financial strategy and leverage the benefits of digital assets while minimizing risks.

Background: What is Cryptocurrency

Cryptocurrency is a digital or virtual currency that utilizes cryptography to secure its transactions and is recorded on a decentralized ledger known as blockchain. This technology offers several key advantages:

- Encryption: Strong encryption safeguards transactions.

- Immutability: Records on the blockchain are virtually immutable, making it difficult to alter or tamper with transactions.

- Decentralization: Cryptocurrencies operate independently of central banks and governments, offering a degree of financial freedom.

Key Examples: Bitcoin (BTC) and Ethereum (ETH) are among the most prominent cryptocurrencies.

Market Growth and Regulatory Landscape:

The global cryptocurrency market is projected to experience significant growth in the coming years. While the potential benefits of crypto are widely discussed, including its borderless nature and enhanced security, concerns about its volatility and potential for misuse remain. The regulatory landscape surrounding crypto is still evolving, with governments worldwide grappling with how to best regulate and integrate this emerging technology.

Next: Understanding Cryptocurrency Taxes

This section will delve into the tax implications of cryptocurrency transactions as defined by the Internal Revenue Service (IRS).

Crypto Taxes: The IRS Perspective

From the IRS’s perspective, cryptocurrency is a form of virtual currency with an equivalent value in real currency. This classification means crypto functions as:

- A medium of exchange

- A unit of account

- A store of value

The IRS recognizes that cryptocurrency is used for various financial transactions, including paying for goods and services or being held as an investment. Because its value fluctuates, these activities can result in taxable gains or losses.

Jeffrey Zhou, CEO and Founder of Fig Loans, emphasizes the significance of cryptocurrency: “Crypto’s appeal as both a transaction tool and an investment asset is clear. The IRS recognizing it as a taxable entity highlights its value, much like traditional currency—it’s not just an investment but a powerful medium for everyday exchanges and a store of wealth.”

Understanding crypto tax obligations is crucial. Learn more about applicable tax rates in the next section.

Crypto Transactions Tax Rates Explained

In the U.S., the IRS does not classify cryptocurrency as a traditional currency like fiat money. Instead, it treats crypto as “property” for federal income tax purposes. As a result, certain cryptocurrency transactions are considered taxable events.

Crypto tax rates range from 0% to 37% and are determined by:

- Transaction type: The nature of the crypto activity (e.g., selling, trading, or using for purchases).

- Holding period: How long you’ve held the asset—short-term (1 year or less) or long-term (more than 1 year).

- Total income: Your overall earnings from cryptocurrency and other sources.

Two Key Tax Categories for Crypto

- Capital Gains Tax

This tax applies when you dispose of cryptocurrency and make a profit, such as:- Selling crypto for fiat currency

- Trading one cryptocurrency for another

- Using crypto to pay for goods or services

- Since crypto is considered a capital asset, you owe taxes on any profit (capital gains) from its disposal.

Rates for 2024 (due April 2025):- Short-term capital gains: For assets held 1 year or less, the rate aligns with ordinary income tax rates, which can reach up to 37%.

- Long-term capital gains: For assets held longer than 1 year, rates are more favorable, ranging from 0% to 20%, depending on your income level.

- Special Rate for Collectibles (NFTs)

Non-fungible tokens (NFTs), considered collectibles, are taxed at a higher rate of up to 28%.

Understanding these tax implications and keeping accurate records of your crypto transactions can help you stay compliant and minimize your tax liability.

Crypto Income Tax: Understanding Your Tax Liability

Earning cryptocurrency through work, mining, staking, or airdrops is considered ordinary income and is subject to income tax rates ranging from 10% to 37%, depending on your income level.

On the other hand, disposing of cryptocurrency—such as selling it, trading it for other digital assets, or using it to make purchases—triggers capital gains tax.

Cryptocurrency income tax applies to various ways you earn crypto, not just capital gains from selling it. These include:

- Crypto Payments: Receiving cryptocurrency as payment for goods or services.

- Crypto Staking: Earning rewards for validating blockchain transactions.

- Crypto Mining: Receive cryptocurrency to contribute computing power to the network.

- Crypto Airdrops: Receiving free tokens as part of promotions or network updates.

- DeFi Interest: Earning returns by lending or staking crypto on decentralized finance platforms.

- Referral Bonuses: Receiving cryptocurrency rewards for referring new users to platforms.

Calculating Crypto Income Tax:

Determining your crypto income tax liability involves:

- Determining the Fair Market Value: Calculate the dollar value of the cryptocurrency received on the date it was earned.

- Applying Your Tax Rate: Determine your federal and state income tax rates based on your total income, including the value of your cryptocurrency income.

Non-Taxable Crypto Transactions

Not all cryptocurrency activities trigger a tax liability. Here are examples of non-taxable crypto transactions:

- Purchasing cryptocurrency: Buying digital assets with fiat currency.

- Transferring assets: Moving crypto between your own wallets.

- Gifting crypto: Sending small amounts as a gift.

- Creating NFTs: Developing or minting a non-fungible token.

- Donating cryptocurrency: Contributions to qualified charities, which may be tax-deductible.

Stephen Boatman, Principal at Flat Fee Financial, emphasizes the importance of consulting with crypto tax professionals. “Crypto tax rules can be tricky to navigate, especially with so many different taxable events,” he says. “Partnering with a crypto tax expert ensures you meet IRS requirements and avoid unnecessary risks.”

For more on crypto tax compliance and regulatory requirements, continue to the next section.

IRS Reporting Requirements for Crypto Taxes

Understanding IRS reporting requirements for cryptocurrency is essential for small business owners and crypto investors to ensure legal and regulatory compliance. Here’s what you need to know:

General Tax Filing Schedule

- Tax Year: The U.S. tax year runs from January 1 to December 31.

- Filing Deadlines: Taxes are due on April 15. U.S. expats have until June 15, and extensions to file (not pay) are available until October 15 by submitting Form 4868.

- Penalties and Interest: Failing to pay taxes owed by the April deadline can result in penalties and interest. To avoid additional fees, estimate and pay your expected tax liability on time.

Crypto Tax Reporting Requirements

To report cryptocurrency taxes, include them in your annual tax return. Prepare the following documentation:

- Copies of previously filed tax returns.

- Employer Identification Number (EIN) or Social Security Number (SSN).

- Financial statements.

Additionally, complete the appropriate forms:

- Schedule D and Form 8949: Report crypto disposals (gains or losses).

- Schedule 1 (Form 1040) or Schedule C (Form 1040): Report cryptocurrency income.

You can file these forms on paper or electronically using tax software like TurboTax or TaxAct. Keeping your records organized will simplify the process and ensure compliance with IRS regulations.

Steps for Crypto Tax Filing

Filing cryptocurrency taxes doesn’t have to be overwhelming. By preparing early and following the right steps, you can confidently navigate the process.

Steps to Report and Pay Crypto Taxes

To accurately report and pay your cryptocurrency taxes, follow these steps:

- Calculate Gains and Losses: Determine the gains or losses from your cryptocurrency transactions.

- Complete Form 8949: Use this form to detail your crypto disposals, including dates, fair market value, and cost basis.

- Attach to Schedule D (Form 1040): Link Form 8949 to Schedule D to summarize your capital gains and losses.

- Report Crypto Income: Use Schedule 1 (Form 1040) under “Additional Income and Adjustments to Income” to report any cryptocurrency-related income.

- Finalize Your Return: Ensure all forms are correctly completed and included in your tax filing.

- Pay Your Taxes: Submit your crypto taxes through the Electronic Federal Tax Payment System (EFTPS), IRS Direct Pay, or by mailing a check.

By adhering to these steps, you can ensure accurate reporting and compliance with IRS regulations. Properly managing this process helps you avoid penalties and keeps your financial records in good standing.

New crypto tax reporting rules

The U.S. Department of the Treasury and IRS recently issued the Crypto Tax Regime for 2025. Here are some of the highlights you should know:

- Mandatory 1099 Forms (2025): Crypto brokers will be required to file 1099 forms for customer sales and gains.

- Exemptions for Non-Custodial Platforms: DeFi platforms and non-hosted wallets are exempt for now, with separate rules expected in the future.

- Cost Basis Tracking (2026): Brokers must report the original purchase price of cryptocurrencies sold.

- Stablecoin & NFT Reporting Limits: Transactions involving stablecoins under $10,000 and NFTs under $600 will not require reporting.

- Crypto Real Estate Reporting: By 2026, real estate transactions using crypto must include fair market value reporting.

- Focus on Tax Compliance: These regulations aim to improve compliance among high-income taxpayers and reduce tax evasion.

- Industry Concerns: Miners and developers may face challenges due to a lack of tools for meeting reporting requirements.

- Safe Harbor for Asset Basis (2025): Taxpayers can allocate unused cost basis for assets held in wallets.

- No Token Classification: The rules do not define tokens as securities or commodities.

Conclusion

Staying compliant with crypto tax requirements is essential to avoid severe legal and financial consequences, including hefty penalties or the risk of business closure. As cryptocurrency becomes a more common form of transaction in the digital age, understanding tax rates and IRS regulations is critical for maintaining compliance.

Applying the key insights shared above is essential if you’re a small business owner or crypto investor. Whether accepting crypto payments or engaging in mining and staking, being informed about and fulfilling your tax obligations is crucial for avoiding potential legal and financial risks.

Handling your business tax returns, including those involving crypto transactions, doesn’t have to be overwhelming. Consider partnering with professional tax filing services to ensure accurate reporting, efficient filing, and regulation compliance. Contact Huckabee CPA today to learn how we can assist you!