We received much information about inflation in the first week of January 2024. Some seemed to support the idea that inflation was sticky, meaning it wasn’t moving lower, while other data suggested inflation was in retreat. Here’s what we learned:

- Headline inflation, as measured by the Consumer Price Index, suggested inflation was headed in the wrong direction last month – higher. It showed prices rising more than expected (0.3%, month-to-month) in December 2023. In November, prices rose less (0.1%, month-to-month).

- Core inflation, excluding volatile food and energy prices, showed steady inflation. Prices rose by the same amount (0.3%, month-to-month) in November and December.

- Producer prices are the prices producers receive for goods and services. Last week, the Producer Price Index showed inflation was headed in the right direction – lower. Producer prices fell (-0.1%, month-to-month) in November and December.

- Conflict in the Middle East could stoke inflation by increasing oil prices and shipping.

The Federal Reserve (Fed) has been working to bring inflation down since March 2022. Over that time, it has lifted the federal funds rate from zero to 0.25% to 5.25% to 5.50%, and inflation has dropped from a peak of 8.9% in June 2022 to 3.4% in December 2023. The Fed’s goal is to lower inflation to two percent.

Markets are closely monitoring the Fed’s success because they want to see rates move lower. Lower rates put more money in the pockets of businesses and consumers, which supports economic growth and higher stock prices.

When the data came in, few investors expected the Fed to begin lowering the federal funds rate this month; however, about three-fourths of the anticipated rates would drop in March, according to data from the CME FedWatch Tool.

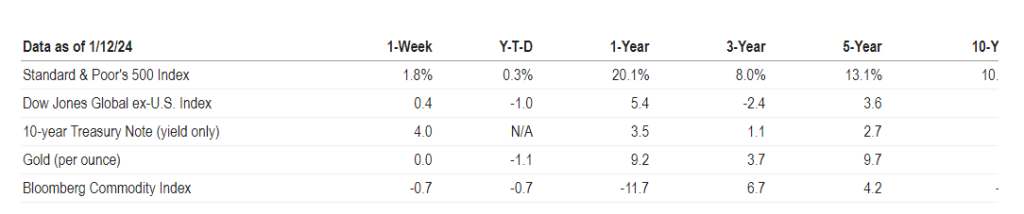

Major U.S. stock indices finished the week higher. Yields on most maturities of Treasuries moved lower.

The rise in consumer prices slowed for a sixth straight month, but the cost of living remains high

The rise in consumer prices slowed for a sixth straight month, but the cost of living remains high

The Bostonglobe reported that the latest Consumer Price Index (CPI) report from the Labor Department shows some welcome signs of easing inflation pressures. Prices in December rose at the slowest yearly rate in over a year – up 6.5 percent compared to a year earlier, down from 7.1 percent growth in November. On a monthly basis, prices even declined slightly in December, the first such drop since May 2020.

Several factors have combined to cool the hottest inflation seen since the early 1980s. Improving supply chains, higher interest rates set by the Federal Reserve, and government interventions in energy markets are helping.

Consumers saw lower prices last month for goods including milk, gasoline, air travel, and both new and used vehicles. While inflation remains high historically, the data provides some tentative evidence that price increases may continue moderating.

The latest inflation data provides some breathing room for the Federal Reserve as it walks the tightrope of taming price increases without sparking recession. While costs remain painfully high for many essentials, December’s cooling Consumer Price Index allows policymakers more latitude to further downshift the pace of interest rate hikes at their upcoming January 31st-February 1st meeting.

Housing, goods, and services still see overall inflation, outpacing income growth for many Americans. Much of the improvement stems from falling energy prices, partly due to tapped government petroleum reserves – declines that may prove temporary.

Nonetheless, this marks another step towards the right direction according to economists. In months ahead, consumers may begin feeling the economic shift underlying the data.

Key details from the CPI report:

- Prices increased 6.5% year-over-year in December, down from 7.1% in November and a 40-year high of 9.1% last June.

Beyond the volatile food and energy sectors, core inflation still remains elevated albeit moderating. The core Consumer Price Index, which strips out food and energy, increased 5.7 percent year-over-year in December – down from 6 percent in November and a post-COVID peak of 6.5 percent last March.

On a monthly basis, the overall CPI actually declined 0.1 percent in December – the first drop since inflation took off after COVID in 2020. Falling gas prices offset rising shelter costs to spur the dip.

The report matched economist forecasts and prompted a modest stock rally, signalling potential peak inflation. After a brutal 2022, the S&P 500 has gained 3.7 percent year-to-date while the tech-heavy Nasdaq rose 5.1 percent.

Meanwhile, the 10-year Treasury yield edged lower to 3.46 percent, retreating from an October high of 4.24 percent. Investors increasingly bet the worst of the Fed’s inflation fight nears its end.

Still, some urge caution before halting rate hikes, arguing tighter policy works with a lag

The Fed’s preferred inflation gauge – the core Personal Consumption Expenditures index – remains well above target at 4.7 percent as of November. Additionally, unemployment sits at 50-year lows and wage growth may fuel further price increases in services, where labor is the biggest cost.

The Fed has thus far raised rates from near-zero to 4.25-4.5 percent to tamp down demand. Further hikes could stall the strong job market. For now, policymakers must balance these risks against persistent inflation in key categories like core services, up 7 percent over the past year.

Conclusion

While cautious optimism emerges, the path remains long for the Fed’s sought-after “soft landing” – taming inflation sans sparking recession.

The outlook shines brighter than in recent memory as price surges show signs of cresting. As Pence Capital’s chief investment officer Dryden Pence noted, “We think inflation has peaked and we expect to see a rapid decline in year-over-year [readings] for the next couple months.”

However, risks still abound on the trek back from 40-year highs. “We also, however, note that getting from 9 percent to 5 percent is a much easier task than getting from 5 percent to 2 percent,” Pence added.

The early progress marks just initial steps quelling the inflation fire, far from extinguishing lingering embers that may reignite price pressures.

For the Fed and economy, the tough slog persists in getting inflation decisively down to acceptable levels. While hopes strengthen, caution remains vital not to declare victory prematurely.