Is the Delta Variant Driving Stagflation for the Economy?

It was a summer of unpleasant surprises for the world economy. The United States, Europe and China are growing at a slower pace than investors expected. The prices consumers pay are increasing at a very rapid rate in the United States.

Stagflation isn’t trending, but it was mentioned in quite a few headlines last week.

Stagflation is a portmanteau of ‘stagnation’ and ‘inflation.’ It occurs when a country experiences slow economic growth along with high inflation and high unemployment. In the United States:

-

- Economic growth was strong during the second quarter; 6.5 percent year-over-year, according to the Bureau of Economic Analysis. However, some forecasts for the third quarter’s economic growth have been revised downward. Economists at one large investment bank lowered their estimate from 9 percent to 5.5 percent, reported Lindsay Dunsmuir of Reuters.

-

- Inflation is the rise in prices over time. The Federal Reserve prefers to measure the rise by looking at median Personal Consumption Expenditures (PCE) inflation. Median PCE was up 0.29 percent from June to July 2021, and up 2.2 percent over the past 12 months. The Federal Reserve’s target for inflation is 2 percent.

-

- Employment showed a solid increase in August, although the gains were less robust than many expected. Unemployment ticked lower (5.2 percent), the labor force participation rate remained unchanged (61.7 percent), and average hourly earnings ticked higher ($30.73).

The culprit behind slowing growth, rising prices, and recent unemployment levels are COVID-19. The spread of the Delta variant created a new wave of parts and labor shortages. Demand for goods is rising as many people appear to be less concerned about the virus. Shortages of goods coupled with high demand for those goods have pushed prices higher. The version is weighing in on consumer spending in the wealthy parts of the world but isn’t causing a recession. In many vaccinated countries, cases are no longer deterring consumers from progressing as much.

The Economist reported that the Delta variant, “…looks like a stagflationary force that is sapping growth less dramatically [than the original COVID-19 strain] but firing up inflation. Delta is weighing on consumer spending in the rich world but not causing a collapse. In countries with lots of vaccines, cases are no longer doing as much to stop consumers from moving around.”

Consumers are less afraid of the disease, despite not having enough vaccinations to fill hospitals. A year ago, US restaurants had nearly half the number of customers compared to 2019. Now, despite hospitals being overcrowded three times, the service is down about 10% from that period.

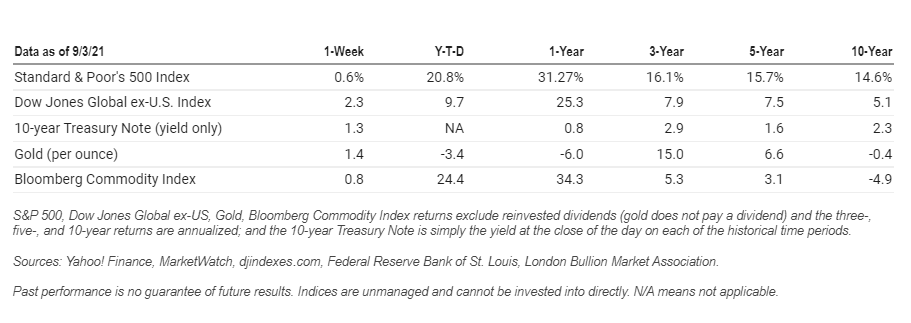

Last week, the Dow Jones Industrial Average finished lower, while the Standard & Poor’s 500 Index and the Nasdaq Composite moved higher. The yield on 10-year Treasuries ticked higher during the week.

Supply Chains

Meanwhile, the proliferation of the delta variant is disrupting global merchandise supply, as consumers, especially Americans, are looking to buy more cars, gadgets and sports equipment than ever before.

Outbreaks of low vaccination rates in Southeast Asian countries are causing temporary shutdowns in factory production and logistics networks, which in turn exacerbate supply chain disruptions.

In the United States, retailers including Gap and Nike have prompted the White House to donate more vaccines to Vietnam, which is vital to getting their factories back online. The shortage is driving up the prices.

Factory hiring is being constrained by input shortages, especially semiconductors, which have depressed motor vehicle production and sales.

Raw material shortages have also made it harder for businesses to replenish inventories.

Motor vehicle sales tumbled 10.7% in August, prompting economists at Goldman Sachs and JPMorgan to slash third-quarter GDP growth estimates to as low as a 3.5% annualized rate from as high as 8.25%.

“At some point production should pick up, allowing for the restocking of inventories and supporting sales, but it is unclear exactly when this will occur,” said Daniel Silver, an economist at JPMorgan in New York. “The recent spread of the Delta variant and persistence of broader supply chain issues has generated some downside risk to the near-term outlook.”

Changes in the relationship between the virus and the economy have implications for policymakers. They will not be able to replicate the pandemic’s trick of the beginning of the pandemic of restricting the movement of people as a way of stopping the spread of the virus while issuing financial aid to create a compensatory surge in demand for goods.

If the spread of the delta variant hurts service industries such as leisure and hospitality, more financial aid would only create more inflation. It is also hard to argue that fear of the virus scares consumers away from shopping and that government restriction to slow the spread of the disease are therefore of little additional economic cost.

A weak correlation between the need for cases and the movement of people and the growth of the service sector drives up the cost of the lockdown.

U.S. job growth seen slowing in August

According to reporting from Reuters, U.S. employment growth likely pulled back in August after gaining nearly 2 million jobs in the past two months as soaring COVID-19 cases reduced demand for travel and entertainment, but the pace was probably enough to sustain the economic expansion. Recent spikes in COVID-19 cases could also have kept some unemployed people home, frustrating efforts by employers to boost hiring.

“The Delta variant is like a sandstorm in an otherwise sunny economy,” said Sung Won Sohn, a finance and economics professor at Loyola Marymount University in Los Angeles. “If it weren’t for that, employment in August would have been even higher.”

According to a Reuters survey of economists nonfarm payrolls likely increased by 750,000 jobs last month. The economy created 1.881 million jobs in June and July. Should job growth in August meet expectations, that would leave the level of employment about 5 million jobs below its peak in February 2020.

But the forecast is highly uncertain, with estimates ranging from 375,000 to 1.027 million.

High-frequency indicators have suggested a softening in demand for air travel, hotel accommodation, and in-person dining, which some economists expect led to a moderation in leisure and hospitality job growth.

Reports this week showed a measure of factory employment contracting and private payrolls undershooting expectations. But hiring by small businesses accelerated and consumers’ views of the labor market remained fairly upbeat.

Over the last several years, including in 2020, the initial August payrolls print has undershot expectations and been slower than the three-month average job growth through July.

Conclusion

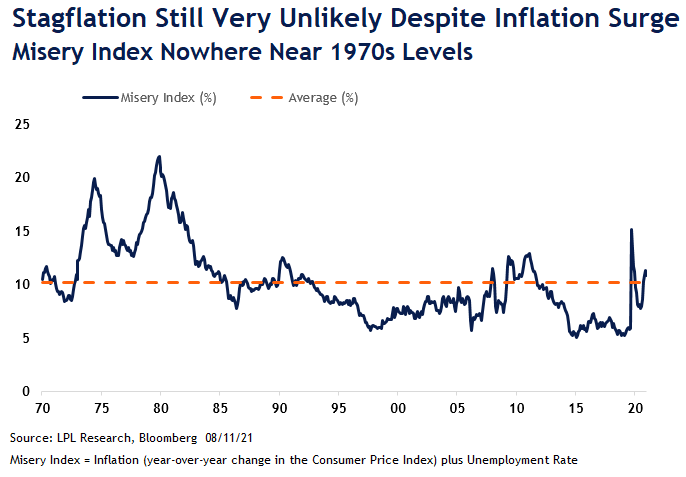

Not all economists feel we are headed for a “stagflation” of the 1970s which saw runaway inflation—largely driven by sky-high energy prices—and lackluster economic growth. for instance LPL Financial, published an article recently stated “We don’t believe the current environment is anything like the stagflation experiences of the 1970s,” explained LPL Financial Director of Research Marc Zabicki. “We think much of the elevated inflation readings we’re seeing now are transitory and related to pandemic bottlenecks and materials shortages. Meanwhile, the economic reopening and massive stimulus should provide a strong one-two punch to keep economic growth well above average through 2022.”

That said, after the boosts from the reopening and stimulus pass, the U.S. economy may resume its pre-pandemic growth trend in the neighborhood of 2% real gross domestic product (GDP) growth.

{kind=link}