Coronavirus stimulus package CARES Act: What you should know as a business owner

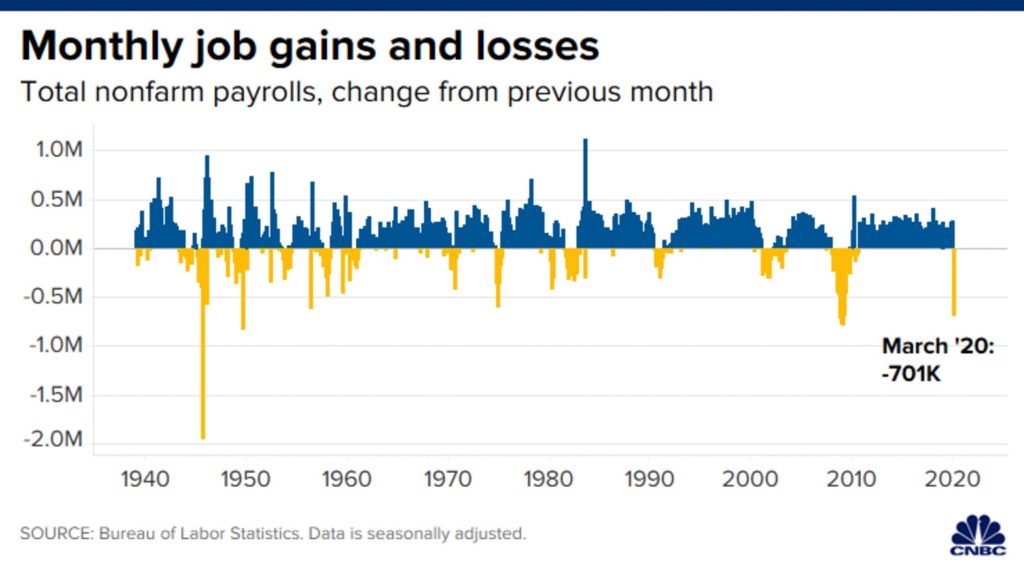

On March 27, 2020, Congress officially passed a $2 trillion stimulus package, called the Coronavirus Aid, Relief, and Economic Security (CARES) Act, aimed at helping employees, businesses, and states deal with the economic fallout from efforts to curb the coronavirus outbreak. The HR.748 CARES Act is the third round of federal government aid related to COVID-19. Large accounting firms Grant Thornton, BDO and Baker Tilly wrote informative articles on the highlights of the CARES Act stimulus program. The latest US payroll numbers (according to Labor Department report) plunged 701,000 in March just begin to capture the the start of a job market collapse according to reporting from CNBC. It was the first decline in payrolls since September 2010 and came close to the May 2009 financial crisis peak of 800,000. Some two-thirds of the drop came in the hospitality industry, particularly bars and restaurants forced to close during the economic shutdown. Over 10 million people filed for unemployment benefits in the month of March.

On March 27, 2020, Congress officially passed a $2 trillion stimulus package, called the Coronavirus Aid, Relief, and Economic Security (CARES) Act, aimed at helping employees, businesses, and states deal with the economic fallout from efforts to curb the coronavirus outbreak. The HR.748 CARES Act is the third round of federal government aid related to COVID-19. Large accounting firms Grant Thornton, BDO and Baker Tilly wrote informative articles on the highlights of the CARES Act stimulus program. The latest US payroll numbers (according to Labor Department report) plunged 701,000 in March just begin to capture the the start of a job market collapse according to reporting from CNBC. It was the first decline in payrolls since September 2010 and came close to the May 2009 financial crisis peak of 800,000. Some two-thirds of the drop came in the hospitality industry, particularly bars and restaurants forced to close during the economic shutdown. Over 10 million people filed for unemployment benefits in the month of March.

So as the social distancing is shutting down businesses the government passed legislation to try and soften the blow to the people who may become unemployed as well as to businesses to incentivise them to keep employees on the payroll.

So as the social distancing is shutting down businesses the government passed legislation to try and soften the blow to the people who may become unemployed as well as to businesses to incentivise them to keep employees on the payroll.

The CARES Act marks the largest economic relief package in our nation’s history.

A lot of the CARES Act pertains to tax and related economic relief assistance for businesses and individuals. The Act offers rebates for many individual taxpayers, expands unemployment insurance coverage and provides opportunities to access retirement plan funds without penalties. On the corporate side of it, net operating loss rules are relaxed, new loan programs are available and certain payroll tax liabilities can be deferred. In addition, several revenue-raising provisions from the Tax Cuts and Jobs Act (TCJA), limiting business deductions are being temporarily rolled back or modified.

Important ProvisionTakeaways

Small business loans

Small business interruption loans of up to $10 million would be available to companies and certain nonprofit organizations with 500 or fewer employees to meet payrolls and other employee-related costs as well as debt, rent and utility payments. According to a fact sheet posted on the Treasury’s website, the loan amounts will be forgiven as long as the money is “used to cover payroll costs, and most mortgage interest, rent, and utility costs over the 8 week period after the loan is made” and “employee and compensation levels are maintained.”

Eligible companies must qualify as a “small business” as defined under the Small Business Act. Small businesses need to be aware of the “Paycheck Protection Program,” which is part of the emergency stimulus package to help small businesses pay employees during the crisis.

Figuring the most advantageous use of the many taxpayer-friendly provisions of the CARES Act may require careful planning. For instance, a taxpayer who participates in the small business loan program (aka payroll interruption loans) are not allowed to use the employee retention credit. Taxpayers who have part or all of their payroll interruption loans forgiven are not eligible for the payroll tax deferral. Evaluating the most beneficial way to utilize the CARES Act requires a facts-and-circumstance analysis from a professional advisor. According to an interview with Yahoo News, billionaire entrepreneur Mark Cuban, the owner of the Dallas Mavericks and investor on the hit TV show “Shark Tank,” is encouraging small businesses to apply for the $349 billion in forgivable loans as part of the CARES Act, calling it “literally the best stimulus bill ever for small businesses.”

Individual Recovery Refund Checks

The $1,200 recovery refund checks for each taxpayer ($2,400 for joint filers) plus an additional $500 per qualifying dependent child age 16 and under will send out to certain taxpayers depending on their earned income, Social Security benefits and retirement income of the taxpayer as based on 2019 returns (or 2018, if a 2019 return has not yet been filed).

The rebate amount phases out beginning at $150,000 of adjusted gross income for a joint return ($75,000 for single taxpayers, $112,500 for head of household) and completely phases out at $198,000 ($99,000 for single taxpayers, $136,500 for head of household). The tax rebates do not extend to nonresidents, trusts, estates or anyone who can be claimed as a dependent on someone else’s return. The CARES Act provides that the IRS will make automatic payments to individuals who have previously filed their income tax returns electronically, using direct deposit banking information provided on a return any time after January 1, 2018.

Unemployment benefits

The federal government will supplement unemployment benefits for furloughed workers for up to four months under the “Keeping American Workers Employed and Paid” program.

TCJA revisions

Several provisions from the TCJA are altered, including:

- Net operating losses: Net operating losses can now offset 100% of taxable income for 2018, 2019 and 2020, rather than the 80% under the TCJA. Net operating losses incurred in these years can now be carried back to the previous five years for a refund.

- Loss limitations for noncorporate taxpayers: Internal Revenue Code section 461(l) regarding the limitations of “excess business losses” incurred by noncorporate taxpayers is deferred until 2021.

- Section 163(j) interest limitation: A taxpayer’s adjusted taxable income limit increased to 50% from 30% for the 2019 and 2020 tax years.

- Qualified improvement property: Fixing the “retail glitch,” qualified improvement property is now 15-year property, eligible for bonus depreciation, and is retroactive to 2018.

- Refundable tax credits: Unused minimum tax credits (MTC) are allowed to be refunded in 2018 and 2019.

Employee retention credit

Quarterly credits are available to employers that have experienced a full or partial suspension in their operations due to COVID-19 against certain employer payroll taxes, subject to certain restrictions.

Payroll tax deferral

Payment of the employer (not employee) portion of the FICA 6.2% payroll tax liability is deferred with half coming due in 2021 and remaining half due in 2022. The deferral applies to 50% of self-employment tax liability as well.

Early withdrawals from retirement plans and participant loans

Taxpayers affected by COVID-19 can withdraw up to $100,000 from a qualified retirement plan before the end of the year, without being subject to the 10% early withdrawal penalty. In addition, a taxpayer can take a participant loan from certain retirement plans for coronavirus-related relief up to the lesser of $100,000 or $100% of the account balance.

Temporary waiver of required minimum distributions

For 2020, the required minimum distributions retirees must take from retirement plans and IRAs are suspended.

Required minimum distributions

For 2020, the required minimum distributions retirees must take from 401(k) plans and IRAs are suspended.

Alternative Minimum Tax Credit Refunds

The CARES Act allows the refundable alternative minimum tax credit to be completely refunded for taxable years beginning after December 31, 2018, or by election, taxable years beginning after December 31, 2017. Under the Tax Cuts and Jobs Act, the credit was refundable over a series of years with the remainder recoverable in 2021.

Business provisions

Small business loans

Small business loan programs play a key role in the Act, making small business interruption loans available to companies and certain nonprofit organizations with 500 or fewer employees. To qualify, the company or organization must fall under the parameters of “small business” determined by the Small Business Act, during the period between Feb. 15, 2020, and June 30, 2020.

- The maximum loan amount is the lesser of $10 million or an amount determined using a formula that incorporates the applicant’s payroll, mortgage, other debt and rent payments.

- Proceeds could be used to meet payrolls and other employee-related costs as well as debt service, rent and utility payments. In addition, certain expenditures can qualify for loan forgiveness.

– Amounts eligible for this forgiveness are based on monies used to cover certain payroll, mortgage interest, rent and utility costs paid within eight weeks of the loan’s origination date. Limits would apply to the amount eligible for forgiveness.

– For example, if a business borrows $5 million under this program and incurs $2.5 million of eligible expenses within eight weeks of obtaining the loan, that $2.5 million is eligible for forgiveness.

– The debt forgiveness is not subject to federal taxation. However, state taxation of such debt forgiveness is far from certain at this time - Taxpayers that participate in the small business loan program are not allowed to use the employee retention credit, and taxpayers that have part or all of this small business loan forgiven are not eligible for the payroll tax deferral.

Net operating losses

The TCJA limited the amount of taxable income a net operating loss (NOL) could offset to 80%. The CARES Act restores NOL usage to pre-TCJA levels, meaning NOLs can offset 100% of taxable income for 2018, 2019 and 2020 returns. The 80% limit would apply to taxable years beginning after Dec. 31, 2020. Taxpayers with NOLs that were limited to 80% of taxable income on 2018 returns should consider amending their returns to take advantage of this provision.

The TCJA also eliminated a taxpayer’s ability to carry back NOLs. The CARES Act allows NOLs from 2018 to 2020 to be carried back five years. Taxpayers with losses in those years should review prior years to determine whether to carry back their NOLs to get tax refunds. Keep in mind that the alternative minimum tax (AMT) NOL rules may still be in effect depending on the carryback year. Consequently, you may not be able to offset 100% of prior-year income for AMT purposes.

There are also special rules for real estate investment trusts (REITS), life insurance companies and those taxpayers with section 965 income inclusion amounts (U.S. shareholders paying a repatriation tax on untaxed foreign earnings).

Loss limitations for noncorporate taxpayers for 3 years

Section 461(l), created by the TCJA, limits excess business losses of noncorporate taxpayers. Individuals with business losses from partnerships, S corporations or sole proprietorships can only offset nonbusiness income with a portion of the active loss plus a threshold amount ($255,000 for single filers, $510,000 for joint filers for 2019). This provision was originally effective for taxable years beginning after Dec. 31, 2017, and before Jan 1, 2026. The Cares Act delays the effective date until 2021. This could possibly result in amended returns if you have a section 461(l) limitation in prior years.

Once section 461(l) becomes effective in 2021, wages will no longer be considered business income for purposes of this limitation. While more taxpayers will likely be subject to this limitation in the future, it will not impact their ability to obtain a refund if subject to this limitation in the past.

The CARES Act defers the effective date of Section 461(l) for three years, but also makes important technical corrections that will become effective when the limitation on excess business losses once again becomes applicable. The CARES Act temporarily modifies the loss limitation for noncorporate taxpayers so they can deduct excess business losses arising in 2018, 2019, and 2020. (Code Sec. 461(l)(1), as amended by Act Sec. 2304(a)) Accordingly, net business losses from 2018, 2019, or 2020 may offset other sources of income, provided they are not otherwise limited by other provisions that remain in the Code. Beginning in 2021, the application of this limitation is clarified with respect to the treatment of wages and related deductions from employment, coordination with deductions under Section 172 (for net operating losses) or Section 199A (relating to qualified business income), and the treatment of business capital gains and losses.

![]() So now by waiving the previous $500,000 limit on business losses against other income for non-corporate taxpayers, The New York Times and CNN both pointed out that “So now real estate moguls with lucrative day jobs or bountiful capital gains from other investments can go back to living tax-free, the Kushner way, before limits were put in place as part of the 2017 tax reform bill.” and on top of that The change applies to this year — and retroactively to 2019 and 2018. This means wealthy individuals can file amended returns now, and get refunds of perhaps millions of dollars. So if you are San Diego real estate investor this could really beneficial.

So now by waiving the previous $500,000 limit on business losses against other income for non-corporate taxpayers, The New York Times and CNN both pointed out that “So now real estate moguls with lucrative day jobs or bountiful capital gains from other investments can go back to living tax-free, the Kushner way, before limits were put in place as part of the 2017 tax reform bill.” and on top of that The change applies to this year — and retroactively to 2019 and 2018. This means wealthy individuals can file amended returns now, and get refunds of perhaps millions of dollars. So if you are San Diego real estate investor this could really beneficial.

Business interest expense limitation (section 163(j)) mended for Taxable Years Beginning in 2019 and 2020

The TCJA limits the interest expense deduction to 30% of a taxpayer’s adjusted taxable income (ATI) plus interest income plus floor plan interest expense. The CARES Act increases the ATI limit to 50% for the 2019 and 2020 tax years. In addition, taxpayers can elect to use 2019 ATI for the calculation for their taxable year beginning in 2020. However, special rules apply to partnerships. A partnership does not get to use the increased limitation in 2019, deferring any potential benefits from the 50% threshold to 2020.

Qualified improvement property

In a much longed-for technical correction to the TCJA, the CARES Act fixes the so-called “retail glitch.” Qualified improvement property (QIP) becomes 15-year property, eligible for bonus depreciation. This change is retroactive to 2018. Taxpayers that placed QIP in service in 2018 may be able to file an accounting method change (Form 3115) to “catch up” the bonus depreciation on their 2019 return. Taxpayers may also be able to amend their 2018 return to claim bonus (under the “one-year depreciable property” rule). Certain partnerships are restricted from amending returns under the centralized partnership audit regime (CPAR) rules.

The QIP change does not help real property trades or businesses that previously elected out of section 163(j). Taxpayers that made the irrevocable real property trade or business election to opt out of the business interest expense limitation must depreciate nonresidential real property, residential real property and QIP under the alternative depreciation system (ADS). ADS property is not eligible for bonus depreciation. Unless Congress changes this rule to provide retroactive relief, electing real property trades or businesses cannot take bonus on QIP. Congress may address this issue in the next round of coronavirus legislation.

- The tax treatment of Qualified Improvement Property which includes Qualified Leasehold, restaurant and leasehold Improvement property was changed to qualify as 15-year property as a technical correction to the Tax Cut and Jobs Act of 2017(TCJA).

- The classification as 15-year property (as opposed to 39-year property) makes these asset subject to 100% Bonus Depreciation deductions for many taxpayers.

Payroll tax deferral

The Act defers payment of the employer’s portion of the FICA 6.2% payroll tax liability. This deferral applies to wages incurred after the date of enactment through Dec. 31, 2020. Half of deferred payroll tax liability would be due by Dec. 31, 2021, with the remaining 50% due by Dec. 31, 2022. These late payments would not be subject to underpayment penalties. Again, this payroll deferral applies only to the employer, not the employee, portion of the FICA 6.2% payroll tax. Self-employed taxpayers are also allowed to take advantage of this deferral.

Employee retention credit

The CARES Act provides a quarterly credit against certain employer payroll taxes available to employers that experienced a full or partial suspension in their operations (and, in some cases, a significant decline in gross receipts) due to COVID-19. The amount of the credit is 50% of qualified wages paid or incurred from March 13, 2020, through Dec. 31, 2020, not to exceed $10,000 per quarter. For this purpose, wages are payments to employees while they are unable to work due to the operational or financial difficulties described above, subject to certain limitations.

For employers with 100 or fewer employees, qualified wages are amounts paid to employees while the employer is experiencing operational or financial difficulties described above, without considering whether all or a portion of the employees are unable to work (e.g., the business is shut down or they’re furloughed) due to these coronavirus-related difficulties. For employers with greater than 100 employees, qualified wages are limited to amounts paid to employees while they are unable to work due to coronavirus-related issues.

This credit is unavailable to employers that have received a small business interruption loan and may be limited if the employer took the credit for paid family and medical leave under the TCJA. For purposes of this credit, controlled groups are treated as one employer.

Amendments to payroll tax credits under the Families First Coronavirus Response Act (FFCRA)

The CARES Act amends the FFCRA to make the payroll tax credits refundable for both the emergency sick leave pay and emergency Family and Medical Leave Act (FMLA) pay. Additionally, the CARES Act provides the two payroll tax credits may be provided in advance; the Treasury Department is instructed to provide guidance on this.

The CARES Act also amends the FFCRA to provide that an eligible employee, solely for purposes of emergency FMLA pay, includes employees who are rehired by the employer, if such employee had (1) been laid off on March 1 or a later date, and (2) worked for the employer for at least 30 days of the last 60 day prior to being laid off.

Refundable tax credits

The TCJA repealed the corporate AMT but permitted unused minimum tax credits to be carried forward and refunded between 2018 and 2021. The Act allows for the unused credits to be refunded in 2018 and 2019. An election may be made to take the entire refundable credit amount in 2018. It appears that guidance will be required from Treasury if an election is made to take the entire credit in 2018.

Corporate charitable contributions

The CARES Act expanded the threshold for corporations making charitable contributions to 25% from 10% of corporate taxable income for taxable years beginning after Dec. 31, 2019. Also, the deductible threshold for contributions of food to charitable organizations that use it for the ill or needy also increased to 25% for 2020 donations.

Coronavirus Economic Stabilization Act

In addition to the small business loan program described above, there is a separate $500 billion fund established under the Coronavirus Economic Stabilization Act (CESA) where the Treasury is authorized to make COVID-19 loans, loan guarantees and other investments in support of eligible businesses. Loan recipients under this program are subject to both employee and executive compensation and stock buyback restrictions, plus maintain a specified level of employment for a certain period.

Employee compensation limits

Businesses taking advantage of these loan agreement provisions would be legally bound to mitigate executive compensation for one year after the loan is paid off. Generally, officers and employees making more than $3 million in 2019 will find their compensation limited to a base of $3 million, plus 50% of their 2019 compensation that was in excess of $3 million. There are also restrictions on compensation for officers and employees making more than $425,000. In other words, the CARES Act does not allow taxpayers to take out these relief loans to pay its officers and highly paid employees.

Stock buyback limitations

Companies receiving a government loan under CESA would be subject to a ban on stock buybacks through the term of the loan plus one additional year. Furthermore, executive bonuses are limited and employee protections must be put into place. The Treasury Department must disclose the terms of loans or other aid to companies and a new Treasury inspector general would oversee the lending program.

Employee retention requirements

Businesses acquiring loans through CESA must also maintain their employment levels as of March 24, 2020, “to the extent practicable” and, in any case, cannot reduce their workforce by more than 10% of the March 24 baseline.

Conclusion

Many of the provisions will provide tremendous cash flow relief. The suspension of the employer portion of Social Security taxes is particularly powerful, and most of the other provisions are also designed to provide quick access to cash. here may also be opportunities to enhance benefits by pairing the new incentives with other tax planning, especially regarding NOL carrybacks. During this uncertain time, Huckabee CPA is ready to help you with sound advice on informing and supporting your employees as well as keeping your business running thru this crisis. Get a free consultation today.

{kind=link}