You could earn $150,000 per year and pay $0 in taxes.

How? The tax code is designed to favor investors, not W-2 employees.

Here’s how it works—and how you could potentially live tax-free.

As a W-2 employee, your tax burden includes:

- 6.2% Social Security tax

- 1.45% Medicare tax

- Federal income tax, ranging from 10% to 37% depending on your income level.

For example, say you’re married and earning a combined W-2 income of $125,000 annually.

With the standard deduction for Married Filing Jointly (MFJ) at $30,000, your taxable income drops to $95,000.In 2025, you would owe $20,486 in federal taxes.

For investors, the picture looks quite different

The tax code is structured to incentivize certain behaviors while discouraging others.

Take the example of electric vehicles: the government offers EV tax credits to promote their adoption.

Likewise, the government promotes investment activities by offering preferential tax rates on capital gains.

When you sell a capital asset, the difference between what you originally paid (adjusted basis) and the amount you sold it for is called a capital gain or capital loss (IRS Topic 409). In simpler terms, it’s the difference between the purchase and selling prices.

What is a capital asset?

A capital asset is anything you own that can be sold, such as homes, boats, cars, stocks, cryptocurrency, and more.

What is basis?

Basis typically refers to the purchase price of an asset, but it can be more complex, especially for things like houses.

When the IRS mentions “realized,” it simply means the moment you sell the asset. Before selling, you might have unrealized gains or losses, which only become “realized” once the sale occurs.

Capital gains tax applies to the profits you earn from selling investments like stocks, mutual funds, property, or ETFs within a given year.

Three key factors determine the exact rate you pay:

- The amount you originally paid for the investment, including any adjustments (e.g., broker fees)

- The length of time you’ve held the investment

- Your current income level

When you sell an investment like stock, a mutual fund, or real estate, and you’ve made a profit, the IRS taxes that gain. This is called capital gains tax, and it’s different from the taxes you pay on your regular income (like wages or business income).

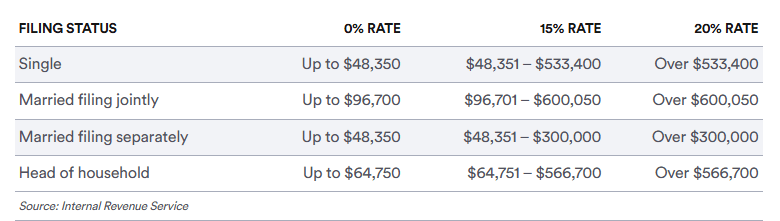

Unlike ordinary income, which is taxed using a progressive tax bracket system (from 10% to 37% in 2024), long-term capital gains have their own tax rates. While most people are aware of the 15% long-term capital gains tax rate, many don’t realize that it’s possible to pay no capital gains tax depending on your income level. This guide will explain how.

If you hold an investment for more than a year, it qualifies as a long-term capital gain.

Long-term capital gains are taxed at a separate, preferential rate rather than your federal marginal income tax rate.

For single filers in 2025, the federal income tax rate is 0% for taxable income (after the standard deduction) up to $48,350.

The 0% cap gains tax bracket applies to taxable income up to $96,700 for married couples filing jointly.

How Are Capital Gains Taxed?

Short-Term Capital Gains (STCG):

If you own an asset for one year or less, any gain is considered a short-term capital gain and is typically taxed as ordinary income. This means it’s subject to the same marginal tax rates you pay on your W-2 income. Current federal tax brackets are 10%, 12%, 22%, 24%, 32%, 35%, and 37%.

Long-Term Capital Gains (LTCG):

If you hold an asset for over a year, the gain is classified as a long-term capital gain, which generally benefits from lower tax rates. The current LTCG tax brackets are 0%, 15%, and 20%.

However, there are circumstances where the tax rate may exceed 20%. For example, you may face higher taxes due to depreciation recapture or profits from collectibles like art, jewelry, and precious metals.

Let’s say you made a wise investment years ago, putting $25,000 into some ETFs. Today, that initial investment has grown to a remarkable $150,000, resulting in a significant long-term capital gain of $125,000.

If this is your sole income source and you are married (similar to the W-2 example), your calculation would look like this:

$125,000 LTCG

- $30,000 Standard Deduction

= $95,000 Taxable Income

However, since this income is taxed at preferential rates, you pay 0% in federal taxes and are exempt from Social Security and Medicare taxes.

Financial Comparison: Investment vs. Employment Income

Your investment strategy yielded $150,000 with no immediate tax burden, while traditional W-2 employment generated $125,000 but incurred $20,486 in federal taxes, significantly reducing your net earnings.

Tax Impact by Location:

While state tax treatment is often similar for both income types, residents of Alaska, Florida, Nevada, South Dakota, Texas, Tennessee, and Wyoming enjoy additional savings with no state income tax – maximizing the tax advantages of investment income.

Strategic Account Withdrawal Strategy

Optimize your tax liability by combining distributions across accounts:

- 401(k): $30,000

- Long-term capital gains: $50,000

- Roth IRA: $20,000

Total cash accessed: $100,000 with zero federal tax impact through carefully coordinating withdrawal sources.

Conclusion

Now, this strategy works best for people in lower income levels for states without state tax; if you live in California and are in a higher income bracket, other methods must be examined.