Choosing the right fundraising structure as an early-stage founder can be a challenging task. Among the available options, the SAFE agreement is often highlighted for its straightforward and flexible design.

Traditional VC funding paths often burden early-stage companies with high costs, complex terms, and immediate dilution. SAFEs (Simple Agreements for Future Equity) emerged as a game-changing alternative, offering startups a streamlined, founder-friendly approach to raising capital with built-in flexibility.

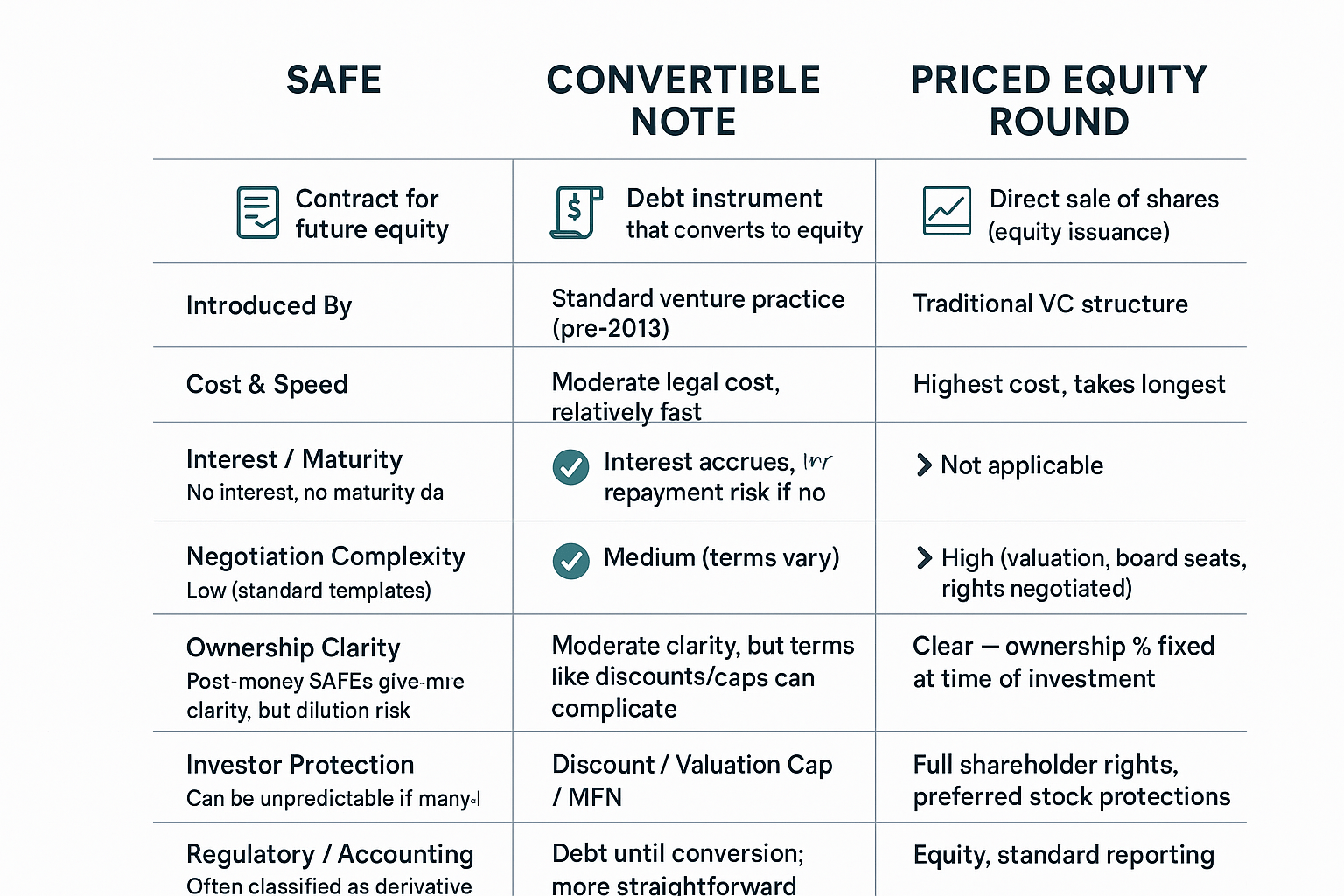

For early-stage startups without a clear valuation—or for founders who want to keep control while still testing and refining their business—SAFEs often provide a simpler, faster alternative to priced equity rounds. Compared to convertible notes, SAFEs eliminate debt features while still offering the flexibility young companies need.

Despite their legal simplicity, SAFEs present significant accounting challenges. Poor classification decisions, valuation errors, or missed compliance obligations can create financial reporting disasters and expose companies to regulatory penalties. Master the intricacies of SAFE management to confidently navigate your funding journey, from initial rounds through audit preparation.

The SAFE Framework: A Modern Funding Innovation

SAFEs represent contractual legal agreements for startups that grant investors future equity rights, typically activated during subsequent funding events or public offerings. The startup accelerator Y Combinator developed this financing model, which has gained widespread adoption due to investor-friendly features, including pricing discounts and valuation caps, combined with the absence of interest accrual or maturity requirements. While legal frameworks remain straightforward and cost-effective, the underlying accounting requirements demand sophisticated treatment.

The Origins of SAFEs Simple Agreement for Future Equity

Before SAFEs, the most common way for early-stage startups to raise money was through convertible notes—essentially short-term debt that converts into equity during a future financing round. While effective, convertible notes carried challenges: they accrued interest, had maturity dates that could create pressure to repay, and often required more negotiation between founders and investors.

To simplify things, Y Combinator introduced the SAFE (Simple Agreement for Future Equity) in 2013, help founders of pre-revenue companies raise their initial round of funding. The SAFE was designed to remove the loan-like aspects of convertible notes, making early fundraising faster, cheaper, and less risky for founders. Instead of being debt, a SAFE is a contractual right to receive equity upon completion of a priced round.

Why SAFEs Took Off

- Speed & Simplicity: SAFEs can often be closed in days instead of weeks since there are fewer terms to negotiate.

- Lower Legal Costs: Standardized templates reduce the need for heavy legal review.

- Founder-Friendly: No interest, no maturity date, and less risk of default compared to convertible notes.

- Flexibility: Investors can participate early without forcing startups to set a valuation too soon.

Key Features of SAFEs

- Valuation Cap: Sets the maximum valuation at which the SAFE will convert into equity, protecting investors from excessive dilution.

- Discount: Offers a percentage discount (e.g., 20%) when the SAFE converts, providing early investors with a reward for taking on higher risk.

- Most-Favored Nation (MFN) Clause: Ensures investors receive upgraded terms if later SAFEs are issued with more favorable conditions.

- Post-Money vs. Pre-Money SAFEs: In 2018, YC updated the SAFE to a “post-money” structure, providing investors with greater clarity on ownership percentages after conversion.

Pros and Cons of SAFEs

✅ Pros (for founders):

- Faster and cheaper fundraising process, they don’t require lengthy negotiations, extensive documentation, or the need to agree on a company valuation

- Can give early-stage startups access to seed capital if they aren’t ready to negotiate a formal valuation with venture capitalists

- Avoids pressure from repayment or maturity deadlines

- Flexible terms that attract early investors

- Allows companies the ability to delay issuing preferred stock until a later stage

⚠️ Cons (for founders):

- Can create unexpected dilution if multiple SAFEs are issued before a priced round

- Accounting treatment is complex—often classified as a liability, requiring revaluation at fair value

- Some investors outside of Silicon Valley may still prefer convertible notes or priced rounds

The Accounting Challenge: Why SAFEs Demand Expert Attention

The apparent simplicity of SAFE contracts masks their accounting complexity. Variable equity conversion scenarios and evolving contractual terms create classification dilemmas and valuation puzzles that require continuous professional assessment and strategic planning.

Companies are generally required to classify SAFEs as derivative liabilities rather than equity. This is because the agreements commit the company to issue a variable number of shares, depending on future events such as funding rounds or an IPO. As derivative liabilities, SAFEs must be revalued at fair market value on a recurring basis—adding complexity to financial reporting.

In limited cases, when the terms are fixed and no cash settlement is required, SAFEs may qualify for equity classification. However, fixed-term SAFEs are relatively rare. Ultimately, the accounting treatment depends on the specific contract terms, and each agreement must be evaluated carefully.

Companies typically must classify SAFEs as derivative liabilities rather than equity, since they require issuing a variable number of shares based on future events such as a financing round or IPO. This treatment requires companies to revalue the SAFEs at fair market value on a recurring basis, adding significant complexity to financial reporting.

In contrast, when terms are fixed and there is no cash settlement obligation, SAFEs may qualify as equity instruments. But these structures are uncommon in practice. The correct classification ultimately depends on the specific terms of each SAFE, so companies should review agreements carefully with accounting advisors before finalizing treatment.

Practical Challenges in Valuation and Reporting

For private companies, SAFEs introduce unique operational hurdles:

- Valuation Costs: Independent fair value assessments can be expensive, particularly for early-stage startups without in-house finance teams.

- Legal & Advisory Fees: The conversion of SAFEs to equity often triggers additional costs for legal review and compliance.

- Reporting Complexity: Ongoing revaluations require clear documentation and alignment with evolving accounting standards, which may strain limited finance resources.

5 Tips to Avoid Missteps

SAFE agreements come with accounting complexity and evolving regulatory considerations that can easily trip up even experienced teams. Leveraging the right expertise—whether in-house or external—helps ensure accurate classification, valuation, and reporting, while minimizing compliance risks.

Key areas where professional support adds value:

- Initial Measurement & Classification: Determining whether a SAFE should be recorded as liability or equity, based on contract terms and accounting standards.

- Fair Value Valuation: Conducting recurring fair value assessments using sound financial models and market benchmarks.

- Regulatory Compliance & Reporting: Aligning treatment with GAAP, IFRS, and SEC requirements, and preparing accurate disclosures.

- Ongoing Monitoring & Adjustment: Reassessing terms and classifications as market conditions or circumstances evolve.

- Strategic Advisory: Understanding how SAFEs impact capitalization tables, future fundraising, and long-term financial health.

Conclusion

Securing expert guidance early helps companies avoid costly errors, maintain transparency, and build audit-ready financial reporting processes. The key lesson for founders is to pay close attention to how much future equity you are giving up when raising money with SAFEs. Feel free to reach out to Huckabee CPA if you have any questions or for a free consultation.