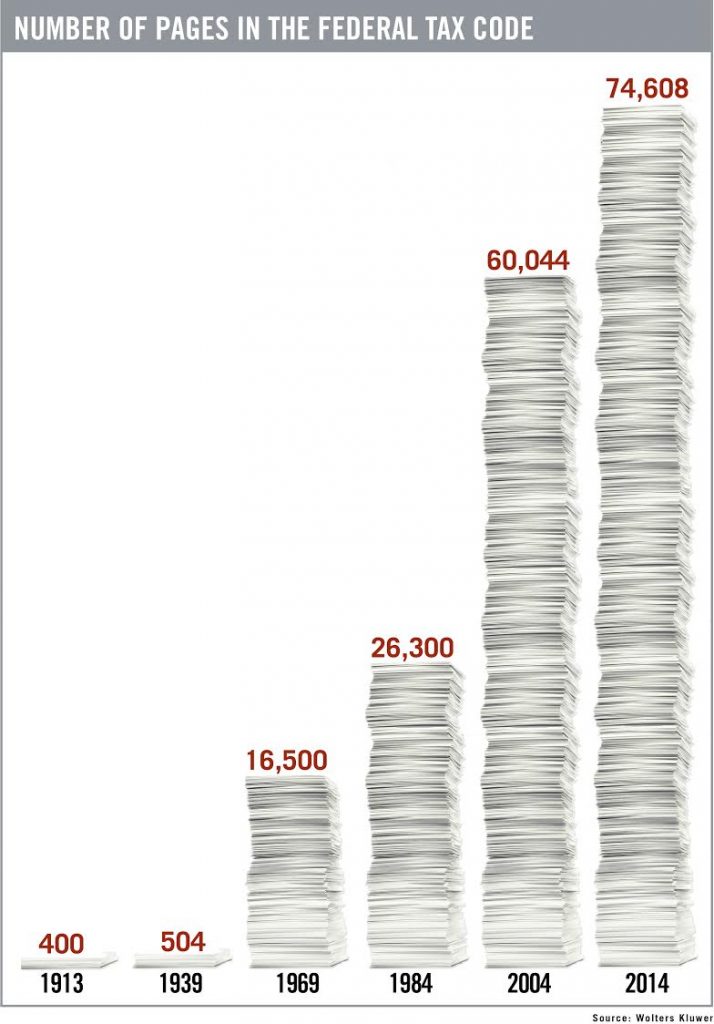

Albert Einstein famously coined the phrase that “the hardest thing to understand in the world is the income tax.” As a business or individual, you should not being paying more in taxes than what is explicitly stated in IRS guidelines. Discovering legitimate and pitfall-free ways to lower taxes on your company is invaluable. As it stands now, 90% of business owners overpay their taxes. With the federal United States tax code coming in at around 70,000 pages long, it is clear why small business owners and accountants experience difficulty in understanding it. Because of this, we have compiled 10 ways that your small business can save money on taxes…let’s take a look:

1. Make Smart Tax Elections

1. Make Smart Tax Elections

Even if a year or accounting period has come and gone, there still remain methods to positively affect what your business is responsible for in taxation areas, during that previous period. That is done by making certain tax-related elections such as such as the manner in which your business deducts depreciation. In this depreciation example, you have the option to deduct all costs of obtaining equipment and machinery in full, up to a set dollar amount; in 2017, that dollar amount is $500,000.

In the event that your startup is not generating a lot of revenue, consider consulting an accountant or CPA about depreciating items over time, rather than assuming the full cost in one hit during one year. This will produce and allow for future year deductions at a point in time that those assets may be far more valuable to you. For instance, let’s say that your business is currently subject to the 15% tax bracket but anticipates being in the 35% tax bracket due to increased profitability in future years. A $10,000 deduction in the current period would produce savings of only $1,500. If this $100,000 cost could have a depreciation schedule over a five or seven year period, your business could potentially have a $3,500 deduction rather than a $1,500 deduction, assuming your business falls into the higher 35% tax bracket. Here are a few more notable ways to help your company save on taxes:

- Making a choice on how to calculate disaster losses…do you want to claim losses related to a disaster on returns for the year in which the disaster occurred, or would it be better to claim that loss on a previous year’s returns?

- Making a choice as to how you want to deduct home office expenses…do you want to use actual costs or an IRS simplified rate ($5 per square foot up to 300 square feet of space?)

- Making a choice as to if you want to deduct vehicle costs for gas based on actual costs or according to the IRS mileage allowance (53.5 cents per mile in 2017.)

Another potential claim could be deducting annual business insurance expenses. You can determine your eligibility for this deduction using IRS form 1040. Here is a list of additional business insurance coverages that you may be able to deduct:

- Workers Compensation Insurance

- Liability Insurance

- Commercial Auto Insurance

- Business Interruption Service insurance

It is unfortunate that small businesses are notorious for having formations that essentially allow for ways to cheat on taxes. For that reason, meticulous scrutinization of small business filings is conducted. This is especially true if your business entity is arranged as a single person LLC, sole proprietorship or a separate entity.

2. Extract Income from your Company Using Tax-free Ways

Although it is pretty difficult to not be taxed on salaries, bonuses and distributions from your respective share of business profits, the success of your business can possibly benefit from using one or both of the following methods:

- Offering tax-free fringe benefits for medical coverage, retirement plans and other items.

- Creating loans in which the business lends on a no- or low-interest basis. If this interest rate is smaller than IRS-set rates, the company will, more than likely, be subject to taxation on the interest received from the arrangement; the key point here though is that, if interest rates are low, such an arrangement isn’t too expensive.

3. Use Accountable Plans

An accountable plan is a plan that is in compliance with IRS standards revolving around employee reimbursements for entertainment, travel, tools and many more items. If an accountable plan is used, a company does not report reimbursements given to employees as income but it does deduct expenses related to those reimbursements; this method is generally thought of as a way to save money in the company employment tax area.

4. Monitor Adjusted Gross Income (AGI)

You will normally see additional taxes, tax limitations and tax breaks teeing off of AGI or modified adjusted gross income, which is usually identical to AGI. An example of this concept in action would be the guideline that does not require payment of the extra 0.9% Medicare tax if your AGI does not exceed $200,000 as an individual taxpayer and $250,000 if you file a joint return.

5. Pay Attention to Carryovers

There are limitations surrounding particular credits and deductions which may not be able to be fully used during a current year- the carryover of these credits and deductions to future years is usually an option. Keep an eye on carryovers and tracking them, should you want to use them in years to come. Some examples are:

- Net Operating Losses

- Capital Losses

- General Business Credits

- Home Office Deductions

- Charitable Contribution Deductions

6. Offer Fringe Benefits to Employees

When your business has additional wages to pay, your company’s employment costs will rise. However, should your business offer fringe benefits to your employees, this tax increase can be avoided. Here are some the tax-exempt benefits that your business should think of offering:

- Health Care Packages

- Group Term Life Insurance

- Long-term Care Insurance

- Dependent Care Assistance

- Disability Insurance

- Educational assistance

- Providing Meals

- Transportation Benefits

7. Profit Sheltering Via Retirement Plans

It’s actually easier than you think to offer and set up simple retirement plans for your employees. Your business is not taxed on earnings that are subsequently used as contributions to employee retirement plans. On a tax-deferred basis, funds will increase and distributions are only taxable when they are used down the line; at that point in time, it is ideal if you are in a lower tax bracket.

It’s actually easier than you think to offer and set up simple retirement plans for your employees. Your business is not taxed on earnings that are subsequently used as contributions to employee retirement plans. On a tax-deferred basis, funds will increase and distributions are only taxable when they are used down the line; at that point in time, it is ideal if you are in a lower tax bracket.

Many options are available when you are investigating retirement plans and your choice will be contingent on your financial standing. In the back of your mind, always recall that employees in your business must be treated in a nondiscriminatory fashion, and it is forbidden to favor company owners or management team members. Also recall that almost all of the costs of saving in a 401(k) will be shifted to business employees.

8.Planning for the Next Year

Even though tax planning is conducted every day throughout the year, there are still ways to save on taxes; in fact, such savings can be very substantial. One good example of this approach is the business that uses cash-based accounting. As a way to save money on taxes, delaying earnings from services is quite popular. By delaying earnings, we mean billing customers later than ordinary for services that have been provided; this would effectively mean that the corresponding payment is received later. This method is usually used during the end of an accounting period, particularly the year-end accounting period.

Several additional strategies can also help to reduce business profitability before year-end. One option is to buy fixed assets and report a portion of their depreciation right away. Or, you can revalue and weed out assets that are listed on your books; doing so will assist in lowering your tax responsibility because more items will be depreciating on your books. In turn, depreciation costs will offset net income and make your taxable income lower because depreciation is subtracted from that net income.

If you come across an asset that is worthless (has no value or use) in your opinion, there is a possibility that this asset can be deleted- your CPA or accountant will know the answer to that question. For example, let’s say you are unable to collect on an account receivable for a customer who will most likely not remit payment. These types of account receivables can sometimes actually be written off, resulting in a loss in your taxable income; hence smaller profits and lower taxes.

Finally, where year-end planning is concerned, it is absolutely essential to submit and file your taxes before their submission deadline. According to IRS.gov: “The penalty for filing late is normally 5% of the unpaid taxes for each month or part of the month that a tax return is late. The penalty starts accruing the day after the tax filing due date and will not exceed 25% of your unpaid taxes.”

9. Altering Business Structure

Sometimes, a business may benefit from a different and new business structure; be it an LLC, sole proprietorship or other types of business formation. One common example of this is when an LLC elects to be taxed as if it were an S corporation. If this method is implemented, FICA taxes for the owner will only be based on that owner’s earnings from the LLC. In this case, the owner’s self-employment tax is determined by business’ net income and his proportionate share of that net income. Should the option to exercise a change in business structure not be taken, the LLC owner will be responsible for taxes on all business earnings, including his own salary.

Let’s use an example to clarify this methodology and assume that an LLC has a profit of $350,000. Let’s also assume that, from an S corporation perspective, $150,000 is considered to be a reasonable salary for the LLC owner. Without taking the election to switch business structures, the LLC’s owner must pay a self-employment tax on that $350,000. Conversely, when the election is taken, FICA taxes for the owner and business will only be based on that $150,000.

10. Abandoning Business Property Instead Of Selling It

Rather than selling business property for a nominal amount, consider talking to your accountant regarding the benefits of abandoning that property. Abandoning property, instead of selling it, will allow your business to claim an ordinary loss on the property. Selling the property at a loss would be considered a capital loss, which is subject to more regulations and limitations than an ordinary loss.

A Section 1231 classification is usually given to the property when a loss due to a property may be considered ordinary or capital, depending on certain characteristics of the property, especially an analysis of the current year’s Section 1231 transactions and prior previous Section 1231 losses.

Conclusion

The dollar amount that your business pays on taxes can be pretty high. Luckily, there are several legal ways that you can decrease this amount if you are aware of certain tax opportunities and tax breaks. Thomas Huckabee, CPA operates a full-service tax firm in San Diego, California and can help you discover methods to lower your taxes by using breaks and deductions. Please contact us for a consultation.