2021 California Business Income Tax Returns Now Include Unclaimed Property Questions from CA Assembly Bill 466 Legislation

CALIFORNIA ASSEMBLY BILL (AB) 46

The California State Controller’s Office’s (SCO’s) increased compliance efforts regarding any unclaimed property will likely result in increased audit activity. CA Assembly Bill 466, which passed and became effective on Jan. 1, 2022, authorizes the Franchise Tax Board (FTB) to share certain information with the SCO related to unclaimed property. Through this change, the state of California expects to increase awareness of and compliance with its Unclaimed Property Law. And a recent article by Singer Lewak mentions that “beginning tax year 2021, the FTB will include additional questions for taxpayers to answer on their business entity tax return.”

What’s Changing?

Effective Jan. 1, 2022, the FTB will add the following questions to certain business entity tax returns:

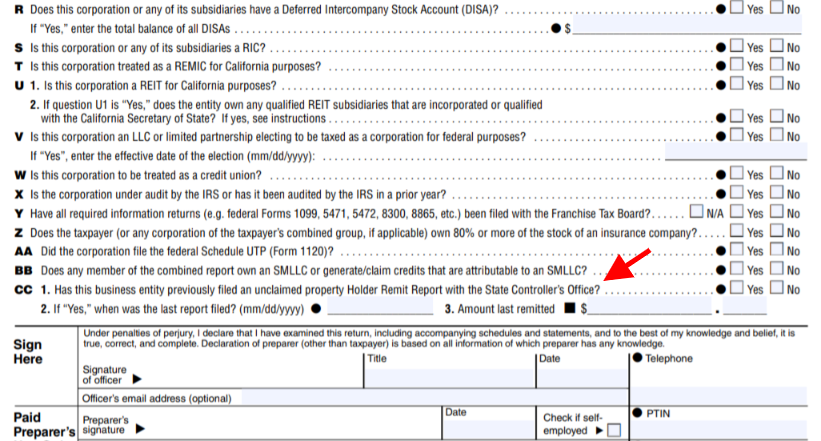

- Has this business entity previously filed an unclaimed property Holder Remit Report with the State Controller’s Office? [Yes/No]

- If “Yes,” when was the last report filed?

- Amount last remitted?

The FTB will add these questions to Forms 100, 100S, 100W, 565 and 568. The FTB will be able to share the answers to these questions, along with the taxpayer’s entity status and revenue range with the SCO. Answers to these questions will have no impact on FTB’s return processing. The form instructions will include information regarding these new questions. For more information and to review form instructions, visit Forms and publications.

Once the SCO obtains this information, it may use it to identify companies it feels may not be in unclaimed property compliance for audit.

Why Is California Doing This?

The FTB Bill Analysis states that the change is intended to help SCO increase awareness of and compliance with California’s reporting requirements. According to a California Legislative Analyst’s Office (LAO) report issued in March 2019, most California businesses are not reporting unclaimed property. The SCO estimates that the compliance rate may be as low as 2%. According to the LAO report, the reasons for such low compliance are willful noncompliance to avoid interest and penalties or ignorance of the reporting requirements.

What Is Unclaimed Property?- the Background

(image credit: unclaimedpropertyfinder)

Unclaimed, or abandoned property consists of tangible and intangible items that a business owes to its employees, customers, vendors, creditors, shareholders—everything from uncashed checks, voided checks, life insurance settlements, unused/unredeemed gift certificates to accounts receivable credits, deposits and refunds, and rebates These funds may also be in the form of cash, stocks, bonds, securities, insurance benefits, and other types of property. Each year millions of dollars are turned over to the State Controller’s Office when businesses are unable to contact property owners. Unclaimed property also refers to abandoned property or accounts with financial institutions or companies where there has been no activity generated with the property for a designated amount of time. After a designated period of time (also referred to as a dormancy period) with no activity or contact, the property is considered to be abandoned therefore classified as unclaimed. While some taxpayers mistakenly believe such property reverts back to their company, by law, the unclaimed property must be turned over to the state. California unclaimed property Holder’s Reports are due before November 1st annually.

All 50 states, the District of Columbia, Puerto Rico, Guam, and the U.S. Virgin Islands have laws that require companies to report and remit various property types that have been unclaimed or dormant for a period of time. Frequent legislative changes and the administrative burden make it difficult for many companies to successfully implement a compliance process and maintain ongoing compliance. States are enforcing unclaimed property laws more strictly, with audits that can go back 15 years or more now prevalent for all industries and businesses of all sizes.

California Unclaimed Property Specifics

The SCO can audit a holder if there is reason to believe the holder failed to report applicable property. California does not currently have a voluntary disclosure/amnesty program. Below is a summary of important aspects of California’s Unclaimed Property Law.

Interest and penalties

California assesses interest at a rate of 12% of the value of the property per year, from the date the property should have been reported.[ii] In addition, the state may assess penalties and/or fines up to $50,000.[iii]

Contingency fee auditors

The SCO conducts its own audits and also utilizes third-party contingent-fee auditors for audits.

Property types

California reviews companies for all types of unclaimed property; however, the property types most frequently reported are:

- Vendor/accounts payable payments

- Accounts receivable credits

- Payroll

Lookback period

A California review will generally cover a 13-year period: 10 years plus dormancy. (Note: The dormancy period is three years for most property types, but for payroll, it is one year).[iv]

CA compliance filings requirements

California has a two-report process with the following requirements and due dates:[v]

- Holder Notice Report – No property is remitted with this report. The due dates for these reports are:

- November 1 – Businesses and organizations

- May 1 – Life insurance companies

- Holder Remit Report and Payment. The due dates for these reports are:

- June 1–15 – Businesses and organizations

- December 1-15 – Life insurance companies

Due diligence

California requires holders to send notices to owners of property with a value of $50 or more prior to reporting the accounts to the state.[vi]

Aggregate filings

California allows aggregate filing for property valued at less than $25.[vii]

Negative reporting

California does not require holders to file a negative report confirming that they have reviewed their accounting for unclaimed property but did not identify any for a given report year.

Please visit the SCO’s Website for further information relating to unclaimed property in California.

Conclusion

The unclaimed property review and reporting process is one that is frequently overlooked by many businesses. It is a common misconception that the only companies that have an unclaimed property issue are those companies that issue items like credit cards or gift cards (that go unused). In practice, any company that has common items like payroll checks and vendor checks that go uncashed has an unclaimed property issue and has an obligation to remit such funds to the state of California, once a specific dormancy period is met.

AB 466 is a further step by California’s Controller’s office to identify an existing unclaimed property, putting additional taxpayers at risk for penalties for failure to remit funds to the state.Have questions feel free to reach out to Huckabee CPA for a free consultation and additional guidance on how these changes may impact your business.

{kind=link}