Tax brackets, 401(k) contribution limits, and estate and gift tax thresholds are expected to get the biggest inflation adjustments in decades. Recently Ashlea Ebeling a WSJ contributor recently published an article where she stated “one ripple effect of the high inflation eating into Americans’ spending power may be lower tax bills.”

The article mentions that come this January a number of workers will get bigger paychecks and be able to put away more money in their retirement accounts when the IRS makes its annual inflation adjustments to dozens of tax provisions. Normally these are minimal modifications, but given August’s persistently high inflation data, tax experts estimate a significant impact on 2023 taxes. Why?

Next year the thresholds for income tax-brackets and the standard deductions are going to be raised, thanks to automatic inflation adjustments built into the tax code, resulting in more Americans’ income being taxed at lower rates in 2023.

Inflation means the IRS could soon change your tax bracket

Jim Young, an accounting professor at Northern Illinois University told the WSJ, “a single taxpayer with $100,000 of adjusted gross income in 2023, could see a tax savings of about $500 compared to someone with the same income this year.”

And the estate- and gift-tax thresholds are expected to go up, too, enabling a higher income wage earning married couple the ability to shelter nearly $2 million more from these taxes. And the contribution limits will likely be raised for retirement plans, meaning more tax-advantaged savings.

“Over the last decade, inflation has been moderate, so we only saw minor increases in tax parameters each year,” said Kyle Pomerleau, a federal tax policy expert at the American Enterprise Institute. “This year, we will see a much larger adjustment as prices have risen much faster.”

The cost of almost everything that people buy housing to food and energy from has skyrocketing in price, so these inflation adjustments can hardly be seen as positive or sign of hope.

Every year, the IRS adjusts many provisions to account for the impact of inflation, ranging from individual tax brackets to how much you can save in your individual retirement account, or IRA. With inflation running near a 40-year high, experts say some major changes are likely to be in store for taxpayers.

The IRS makes the adjustments based on formulas set out in federal law that are somewhat different from headline inflation numbers. Recently the Labor Department reported its consumer-price index was 8.3% higher in August than the same month a year ago.

The tax-provision adjustments are tied to an alternate inflation measure called the chained consumer-price index, which takes into account the substitutions shoppers make as costs rise. The average of the chained CPI from September 2021 to August 2022 is used to calculate the 2023 adjustments, which the IRS will announce in October or November. These ultimately affect tax returns for the 2023 tax year filed in early 2024.

“Adjusting tax-return data for inflation was a purposeful decision by Congress intended to shield taxpayers from annual inflation,” said Mr. Young. “This will hopefully help taxpayers cope with rising prices.” The benefits of these changes could be offset by inflation in other ways. If your wages have gone up, your total tax bill may not go down, Mr. Young said.

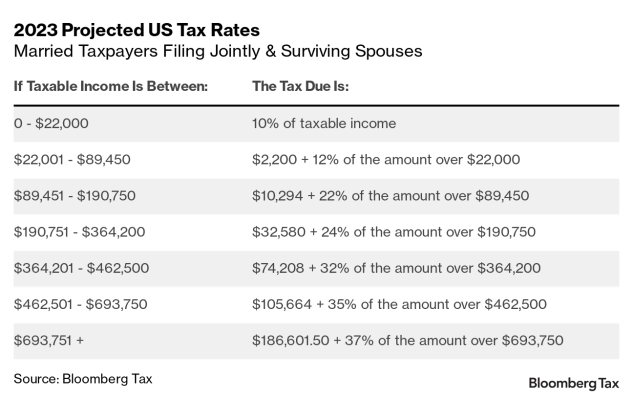

Projected inflation-adjusted amounts for the 2023 tax year

CBS News reported that IRS makes these changes to avoid “bracket creep” from the rising cost of living, noted American Enterprise Institute’s Kyle Pomerleau, an expert on taxes. Without such adjustments, workers who received pay increases to keep up with inflation would be bumped into higher tax brackets, even though their standard of living remained the same.

Here are the estimates, for the IRS adjustments, according to the American Enterprise Institute (AEI):

The threshold for the top federal income-tax bracket in 2023 is expected to climb by nearly $50,000 next year for married couples, and that 37% rate will apply to income above $693,750. For individuals, that top tax bracket will start at $578,125.

(image credit: Bloomberg)

(image credit: Bloomberg)

Those levels and the other tax-bracket breakpoints will all rise about 7% from the tax year 2022, compared with about 3% last year, which was the largest increase in four years. This year’s increase is the largest in the past 35 years, said Mr. Young.

The expected increases in many of the tax-related provisions will be smaller than the estimated 8.7% increase in Social Security monthly benefits anticipated by the Senior Citizens League because the adjustments follow different rules.

The Social Security wage base tax level is estimated to increase 5.5% from $147,000 to $155,100 in 2023, according to the 2022 Social Security Trustees Report.

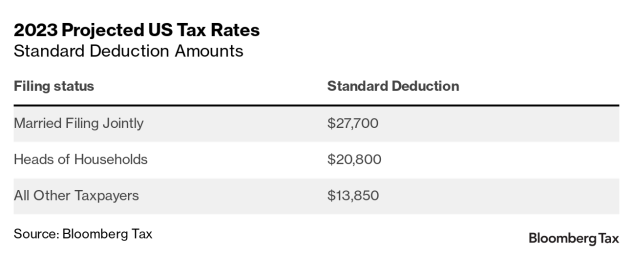

Higher standard deduction

The standard deduction for married couples is expected to be $27,700 for 2023, up from $25,900 this year, and $13,850 for individuals, up from $12,950. This is the amount those who don’t itemize deductions on their returns can subtract from their total earnings subject to income taxes.

The federal estate-tax exclusion amount, which an individual can shelter from estate taxes, is $12.06 million this year. It is expected to increase to $12.92 million by 2023, meaning a married couple could shelter nearly $26 million from estate tax with little planning.

The annual limit on tax-free gifts is expected to climb from $16,000 this year to $17,000 in 2023. Wealthy and high-income earning families will benefit the most from this, as they can give away more without estate- or gift-tax consequences.

Higher limits for FSAs, IRAs

The maximum contribution amount for an individual retirement account is expected to jump to $6,500 for 2023, up from $6,000, where it has been stuck since 2019. The maximum contribution allowed for a healthcare flexible spending account is expected to increase to $3,050 in 2023, up from $2,850 this year.

The maximum contribution amount for a 401(k) or similar workplace retirement plan is governed by yet another formula, using inflation data through September. Actuaries at Milliman, a benefits firm, estimate that the contribution limit will rise from $20,500 this year to $22,500 in 2023, and the catch-up amount for workers aged 50-plus will rise from $6,500 to at least $7,500.

The child tax credit is even more complicated. Under current law, the total tax credit of $2,000 per child isn’t adjusted for inflation, Mr. Pomerleau said. But the additional child tax credit that is refundable and available even to taxpayers who have no tax liability, is adjusted for inflation. It is expected to rise from $1,500 to $1,600 in 2023. The income limits related to the CTC aren’t adjusted for inflation.

Conclusion

This year, taxpayers could see some of the biggest changes in decades due to the hottest inflation since the early 1980s, and while the IRS will likely officially announce these changes in October or November, according to AEI forecasts that many tax provisions will be adjusted upwards by about 7%. This is something taxpayers can use to plan their taxes over the next year. In 2023 taxpayers are going to set their withholding, and businesses will make investment decisions, and that will depend on how much tax they have to pay. For instance, people who use flexible spending accounts to put aside money for medical expenses will need to make those decisions for 2023 in October or November of this year during open enrollment. Have questions feel free to reach out to Huckabee CPA, and get a free consultation about our tax planning services and your specific situation.