Planning and saving for retirement should be a priority for every person. According to a survey from YouGov, 49% of Americans said saving money was one of their New Year’s resolutions for 2022. But just wishing without taking proactive steps won’t deliver results. You have to do something different if you want your habits—and your future—to change! According to a recent article from Dave Ramsey, there are a few simple steps you can take to turbocharge your retirement savings:

- Set a goal for your retirement savings

- Invest 15% of your income into Tax-Advantaged Accounts like a 401(k) and Roth IRA

- Going Beyond 15%—Max Out your 401(k) and Other Investing Options

So let’s talk about investing for retirement using 401(k)s and Roth IRA accounts. A recent article in Fox Business News discusses the benefits of using Traditional IRA’s and Roth IRAs which both offer tax advantages to build a retirement income that can be used as a supplement or an additional income source to those eventually claiming their Social Security income benefits.

Saving for retirement can qualify you for several different types of tax breaks. Recently US News published an article that points out that some retirement accounts allow you to defer paying income tax on your retirement savings, while others help you avoid paying tax on any of the investment gains you accrue.

The problem is that many higher-income earners cannot use a regular Roth individual retirement account (IRA) thanks to strict income caps on contributions to these accounts. To contribute directly to a Roth IRA, your income must be under a certain amount, determined by your modified adjusted gross income (MAGI). Individuals who earn above a specified income limit (based on taxpayer status) are prohibited from opening or funding Roth IRA accounts under IRS regulations.

Here is a quick look at the 2022 limits, per the IRS:

| If your filing status is… | And your modified AGI is… | Then you can contribute… |

|---|---|---|

| married filing jointly or qualifying widow(er) | < $218,000 | up to the limit |

| married filing jointly or qualifying widow(er) | > $218,000 but < $228,000 | a reduced amount |

| married filing jointly or qualifying widow(er) | > $228,000 | zero |

| married filing separately and you lived with your spouse at any time during the year | < $10,000 | a reduced amount |

| married filing separately and you lived with your spouse at any time during the year | > $10,000 | zero |

| single, head of household, or married filing separately and you did not live with your spouse at any time during the year | < $138,000 | up to the limit |

| single, head of household, or married filing separately and you did not live with your spouse at any time during the year | > $138,000 but < $153,000 | a reduced amount |

| single, head of household, or married filing separately and you did not live with your spouse at any time during the year | > $153,000 | zero |

So if you are someone who is a professional that makes over $100,000 a year and you may want to consult a financial advisor about a retirement vehicle called a Backdoor Roth IRA. Despite the semi-illicit name, a backdoor Roth is a legit (and legal) way to make Roth IRA contributions with a high income. Funding this retirement account is one of the best money moves you can make this year.

Backdoor Roth IRA Conversion

According to Investopedia’s definition “a backdoor Roth IRA is not an official type of retirement account. Instead, it is an informal name for a complicated but IRS-sanctioned method for high-income taxpayers to fund a Roth, even if their incomes exceed the limits that the IRS allows for regular Roth contributions.” The major investment brokerages such as Fidelity, Charles Schwab or Morgan Stanley that offer both traditional IRAs and Roth IRAs provide assistance in pulling off this strategy, which basically involves converting a traditional IRA into the Roth variety.

Keep in mind, this isn’t a tax dodge. You still need to pay taxes on any money you use to fund the (NON-DEDUCTIBLE) traditional IRA.

A two-step Roth conversion process

According to a Charles Schwab article In 2010, Congress passed rules to provide more flexibility and allow retirement savers to convert savings held in a traditional IRA into a Roth IRA, paying taxes on the distributions when they make the conversion. Some higher-income earners use this approach, in a two-step process:

- Open a non-deductible traditional IRA and make after-tax contributions. For 2020, you’re allowed to contribute up to $6,000 ($7,000 if you’re age 50 or older). Make sure you file IRS Form 8606 every year you do this.

- Transfer the assets from the traditional IRA to a Roth IRA. You can make this transfer and conversion at any point in the future.

For example, if you contribute $6,000 to a (non-deductible) traditional IRA, this has to be a non-deductible IRA, different than a traditional tax Deductible IRA and then, immediately say within a week or so convert that money to a Roth IRA, you’ll owe taxes on the $6,000. You’ll also owe taxes on whatever money it earns between the time you contributed to the traditional IRA and when you converted it to a Roth IRA.

It is recommended to maintain the $6,000 in a non-interest-bearing account, do not invest it, this way no earnings will have accrued and thus you will avoid any possible tax on accumulated earnings. The key is the IRA must be a NON-Deductible IRA, do not invest the money and convert very quickly as soon as the check clears the brokerage company.

The appeal and limitations of a Roth IRA

With a Roth IRA, you get no up-front tax deduction, as you do with a traditional IRA, 401(k) retirement plan or other tax-deferred account. However:

You pay no tax on either principal or earnings when you withdraw your money (although you must be at least age 59½ and have had the Roth for five years).

There’s no time requirement on when you have to withdraw money, if ever—an appealing option for those wanting to leave the money to heirs.

Pay the tax due

The conversion triggers income tax on the appreciation of the after-tax contributions—but once in the Roth IRA, earnings compound tax-free. Distributions from the Roth IRA in the future are tax-free as well, as long as you are 59½ and have held the Roth for at least five years (note that each conversion amount is subject to its own five-year holding period as it relates to tax-free withdrawals).

If you have no other IRAs, figuring out your tax due will be simple. However, it can be more complicated if you have other IRAs. The IRS’ pro-rata rule requires you to include all of your traditional IRA assets—that means your IRAs funded with pretax (deductible) contributions as well as those funded with after-tax (nondeductible) contributions—when figuring the conversion’s taxes. Then, you pay a proportional amount of taxes on the original account’s pre tax contributions and earnings. If you have questions feel free to give us a call.

Take advantage of the backdoor Roth as it may not last forever

Roth conversions generally can make sense, generally, for many higher-income investors with large amounts saved in traditional IRA or 401(k) accounts. Having investments in traditional brokerage accounts, IRAs, and Roth IRAs as well as 401(ks) can increase flexibility in your retirement stage. If you are a State employee (that already has a pension plan, a typical defined benefit plan), Teacher, civil service employee, a police chief, a sheriff in the state of New York and you make at least 100k then this is a strategy that can be very useful. According to a Forbes article you’re a perfect candidate for a backdoor Roth IRA when you’re a single filer and make at least $139,000 annually. If you file a joint tax return, a minimum $206,000 annual income disqualifies you from a standard Roth IRA.

Claiming Decision & Retirement Security

An article in Think Advisor about how to maximize your social security benefits and what age should someone claim their benefits income retirement stream. According to a recent report from Bipartisan Policy Center, found that more than 1/3 of Americans still claim at age 62 and two-thirds claim before their full retirement age (FRA). Many people can be tempted to claim their benefits early for a variety of reasons that article cites such as: “It’s my money and I want it now,” “Social Security is going bankrupt,” or “my mom/dad/grandparent died at 72 so I want to get some of my money back.” An important aspect of Social Security planning is evaluating whether the individual is likely to be alive in their 80s and 90s. While benefits are available as early as age 62, claiming later permanently raises monthly benefits with the maximum benefits available to those who claim at age 70. There’s a 6% reduction in monthly benefits for each year one begins receiving benefits before full retirement age.

If you are able to wait, delaying claiming past the full retirement age means they will gain about 8% more in monthly benefits each year, up to age 70. For someone with a full retirement age of 67, delaying Social Security retirement benefits until age 70 would result in a 24% increase in the monthly benefit amount.

Here are a few ways that contributing to your retirement personal savings with IRAs can help you diversify your retirement income streams and be in a financial position to not be forced to claim your social security at a suboptimal time.

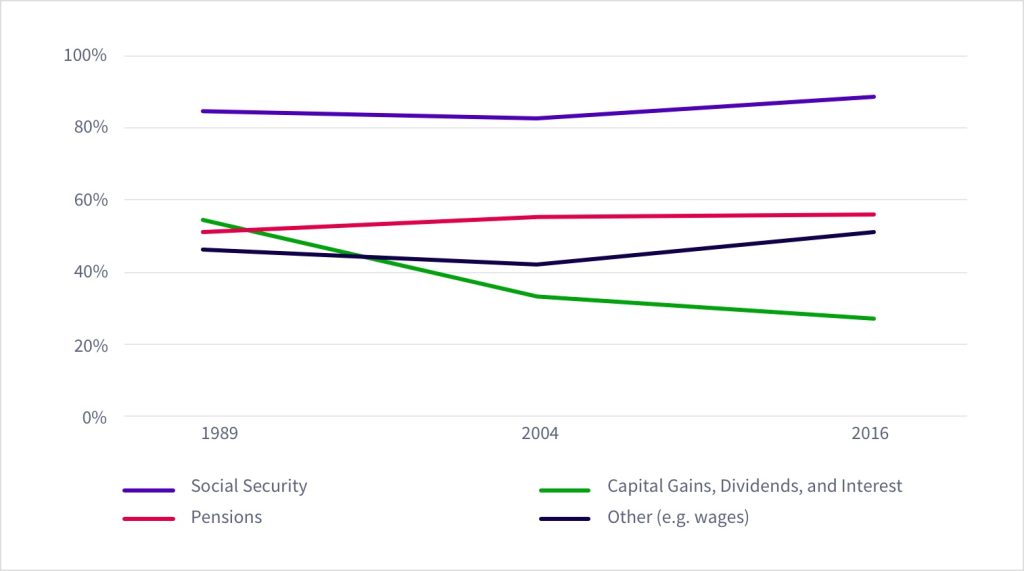

1 You need multiple retirement income streams

Most people cannot live comfortably off of social security benefits alone. The Fox Business article mentions that the average monthly retirement benefit was recently only $1,547 — roughly $18,500 per year. If you earned above-average wages, you’ll collect more, but a huge windfall. Keep in mind that retirement accounts contribution limits will increase over time, and you’ll pass the age-50 threshold at some point, too, so it’s very possible you can amass much more.

2 It can help to build a nest egg that could enable you to retire earlier

For many elderly people, Social Security is a much-needed source of retirement income. But if you want enough income to retire early at 60, you would need to have other income savings besides Social Security. The Fox Business article also points out that

you can start collecting from IRAs as early as age 59 1/2. Now technically you can access it earlier, but you will be hit with an early withdrawal penalty. So obviously the earlier you start contributing to retirement savings and building an investment portfolio, the more you will have over time to draw income from which could help you retire earlier.

3 It can help to maximize your social security benefits by not needing to claim it too early

So as I already mentioned earlier in this article that if a person can wait to begin collecting benefits until age 70, the monthly benefit would be about 24% higher. So income from an IRA can help you pay your bills until your Social Security checks start coming. Another reason you may want to wait to claim your Social Security benefits is if you are a higher earner and married, is to be able to make your checks as large as possible for when you or your spouse are widowed — and able to claim the larger of your two benefit checks.

Conclusion

As a Wall Street Journal article points out that many American households aren’t prepared for retirement, and the recent Covid-19 pandemic economic turmoil is likely widening the disparity.

It is important to educate yourself on retirement strategies and learn more about how to save and invest effectively for your future. If you have any questions feel free to reach out to us.