That’s correct…you read the title of this post correctly. There are many benefits for small business owners in the Tax Cuts and Jobs Act (TCJA), but the elimination of the entertainment expense deduction is simply not one of them. In all seriousness, this is a very serious hit that small and big business must absorb. Tucked into the massive $1.5 trillion tax overhaul that Congress approved last month was the elimination of the 50 percent tax deduction that firms had long been able to take on business-related expenses for “entertainment, amusement, or recreation.”

That’s correct…you read the title of this post correctly. There are many benefits for small business owners in the Tax Cuts and Jobs Act (TCJA), but the elimination of the entertainment expense deduction is simply not one of them. In all seriousness, this is a very serious hit that small and big business must absorb. Tucked into the massive $1.5 trillion tax overhaul that Congress approved last month was the elimination of the 50 percent tax deduction that firms had long been able to take on business-related expenses for “entertainment, amusement, or recreation.”

Let’s make one thing very clear: no one is exempt for this new provision in the Tax Cuts and Jobs Act (TCJA). All entrepreneurs and small business owners are affected by this change in legislation, including C corporations, S corporations, LLCs and sole proprietorships. Effectively, the cost of running a business just went up, astronomically in some instances. Let’s take a look at pretty clear-cut scenario:

Example

It’s, 2018 and, as a small business consultant and insurance agent, James has a meeting with one of his clients. The purpose of the meeting is for James to provide guidance related to a business transaction and sell an insurance policy. James will be taking his client golfing and out to lunch.

Deduction Possibilities

No way. The deduction or write-off for entertainment expenses is no longer available as of the beginning of 2018. Tom will get no deduction for the golfing portion of the visit with his client and, although there is is a very minute chance that the related meal could be written-off, the time and stress involved in filing for a meal deduction makes the process not worth it.

Previous Legislation

Prior law dictated that assuming a cost could be found to be directly or, in some instances, even remotely associated with, the conduct of active business or active trade, a tax deduction was permitted for those activities considered recreation, amusement or entertainment. Now, the expense deduction was capped at 50% of the expense but it was still some reimbursement for a business expense that was notoriously known as outrageously costly for a company. Entertaining is not cheap.

Current Legislation

Current Legislation

There is no deduction (at all) allowed for any of the following:

- Dues for membership dues to any facility or club designed for social or recreation activities

- Activities normally considered to be recreational, entertainment or amusement, in nature

- A club or facility, or any portion of such a venue, used in connection with the above items

Basically, this means that the set of theater tickets, round of golf, fishing trip and skybox no longer come with an associated tax deduction. The loss of this deduction is going to have a tremendous impact on the bottom line of many businesses.

Unforeseen Consequences & Collateral Damage

Many people seem to be unaware of how much actual real business deals are negotiated in that expensive skybox or on that fancy golf course. Many tax professionals will agree that a substantial amount of business is conducted via the use of “entertainment”- that entertaining is a very large portion of courting a potential client, getting to know the client (and vice versa) prior to closing a mutually beneficial deal.

The new legislation dismantling the entertainment tax deduction is also beginning to have an impact on the entertainment industry. Sporting events, theater events and golfing events- particularly where season passes are held- are already feeling the impact. Business dealings and transactions provide an enormous source of income for the entertainment industry, and that enormous source of income is not as enormous as it was in previous years.

Effects on the Restaurant Industry and Meals?

As other entertainments expenses, business meals are also very much affected by the TCJA. Basically, experts are contending that business meals used to be deductible because they were directly connected to IRC Section 274(a) and were deducted because they were classified as being “directly related” to, or “associated” with the entertainment expense. However, experts are contending that the loss of the entertainment expense means that client meals out are not deductible either.

The Surviving Entertainment Deductions

Although positive news to report remains few and far between, there remain a few ways to write-off entertainment expenses under IRC Section 274(e). It is necessary to be realistic here and note that these surviving deductible items are very unique types of expenses and most businesses will not find them useful at all. Nonetheless, they are:

- Recreation, amusement and entertainment expenses considered as compensation to employees contained in their wages- this means including the cost of such expenses in W-2s…something that will not be very popular with those W-2 recipients.

- Recreation and social, including facilities primarily for employees, expenses. These expenses cannot be associated with already highly compensated employees (hence the skybox issue.)

- Expenses for entertainment goods, services, and facilities that you sell to clients. This is otherwise known as the cost of goods sold (COGS.)

- One of those exceptions is for “expenses for recreation, social, or similar activities primarily for the benefit of the taxpayer’s employees, other than highly compensated employees”. (i.e. office holiday parties are still deductible).

- Business meals provided for the convenience of the employer are now only 50% deductible whereas before the Act they were fully deductible. Barring further action by Congress those meals will be nondeductible after 2025.

Keep closely tuned to certain specific IRS regulations and implementation of the new laws associated with them. Of course, a colossal influx of audits and court cases are on the horizon to give us guidance regarding the many new provisions of the TCJA.

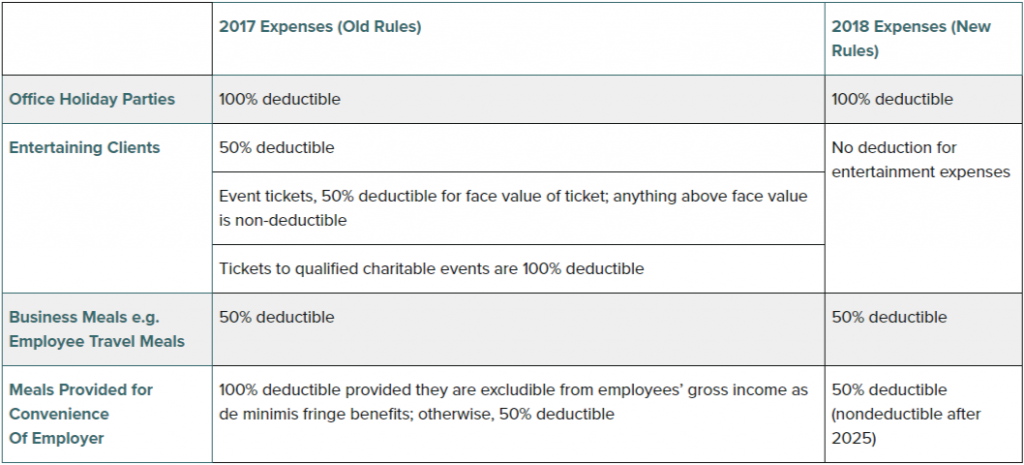

Businesses should keep the new rules in mind as they plan their 2018 meals and entertainment budgets. See below for a chart comparing the rules before and after the Act.

Conclusion

Conclusion

Write-offs for business-related meals with clients haven’t changed; they’re still 50% deductible. That may mean more dinners, and fewer experiences, for clients. But businesses still need to be careful: Going to an extremely expensive restaurant with live music could, for instance, fall under entertainment.

Companies will find ways around this, of course. Promotional events are still deductible as a marketing expense, so companies may start branding outings with more advertising to qualify for the deduction. The caveat: That business pitch needs to last the entire duration of the event, not just a few minutes.

In order for your business to be successful, you should consider leaving its accounting for entertainment expenses, if there even is any, to professionals. Employing the services of a CPA firm will allow you peace of mind because you will know that your company’s accounting processes are in good hands, while adhering to strict accounting laws. Thomas Huckabee, CPA of San Diego California is an small business accounting expert who can help you succeed. Please contact our office for further information.