For many people, (besides owning their own home), founding and running a small business or startup is considered part of the capitalist American dream. Being your own boss (the proverbial “shot caller”), whether that means picking their own schedule or determining the best route to boost income.

For many people, (besides owning their own home), founding and running a small business or startup is considered part of the capitalist American dream. Being your own boss (the proverbial “shot caller”), whether that means picking their own schedule or determining the best route to boost income.

With all the media attention about successful “Unicorn startups” (valued at billion or more) that have gone on to build profitable companies (or not such as in Uber’s and Lyft’s case) and even IPO, makes entrepreneurship seem to be an in vogue thing nowadays. Everyone enjoys hearing about an inspirational entrepreneurial success story, where the entrepreneur as a protagonist overcomes obstacles and builds a thriving, well-known company brand (and become wealthy while doing so). It may make you want to learn from them and even to try to replicate it. But this type of thinking can have its flaws or biases if you are not analyzing the other side of the coin of what things make some startup businesses not make it. Jason Cohen, the founder of WP Engine & Smart Bear Software explains it this way. “The fact that you are learning only from success is a deeper problem than you imagine… drawing conclusions only from data available or convenient and thus systematically biasing your results.”

As I am writing this it is National Small Business Week 2019 that celebrates America’s entrepreneurs and small business owners. And according to the SBA “More than half of Americans either own or work for a small business, and they create about two out of every three new jobs in the U.S. each year.”

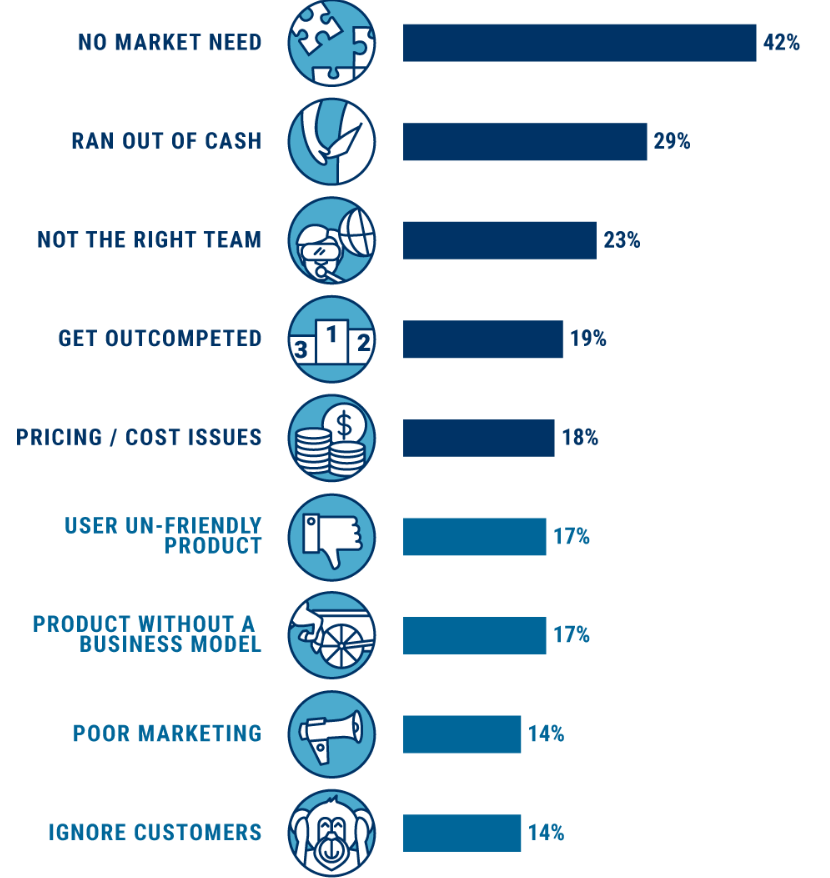

The machine intelligence software platform CBInsights analyzed 101 post mortem business failures to compile the top 20 reasons why startups fail. Forbes contributor Stephanie Burns wrote about this as well. I am going to cover 11 of those business failure reasons. Now many of the startups failed for more than one reason but there was some reoccurring patterns or causes in the data findings. Also, insights written by founders, investors, and journalists offer some clues as well. You’ll see the chart from CB insights highlighting the top 20 reasons doesn’t add up to 100% (it far exceeds it).

From no market need to running out cash to being too early, to ignoring customers, a lot of these issues can be avoided with careful planning and research. Don’t fail. Learn from the mistakes of other startups that did not make it.

From no market need to running out cash to being too early, to ignoring customers, a lot of these issues can be avoided with careful planning and research. Don’t fail. Learn from the mistakes of other startups that did not make it.

“Within 3 years 92% of startups fail.

Learn from their mistakes.”

Let’s get into it.

1) No market need: 42 percent

“Tackling problems that are interesting to solve rather than those that serve a market need was cited as the No. 1 reason for failure, noted in 42% of cases.” -CB Insights

As Stephanie Burns said “This is what is called a solution looking for a problem.” When a product, app, service, gadget, is made because the person thought it was useful or interesting, it can encounter the issue or risk of not having an actual market or need that it will solve. Mike Brown points out “without a clearly defined market for a product or service, turning a profit becomes impossible, and as logic would suggest, a lack of revenue makes it impossible to meet operational expenses and keep doors open.” As CB Insights pointed out from a startup called Patient Communicator had written, “I realized, essentially, that we had no customers because no one was really interested in the model we were pitching. Doctors want more patients, not an efficient office.”

2) Ran out of cash: 29 percent

Cash flow and time can be limited for early-stage companies and they need to use it carefully. Many startups and small businesses struggle with how to effectively allocate and budget their money. This issue was cited as a common problem and big reason for failing and going out of business. It’s usually more than one thing that brings a company down such as failure to find a product-market fit or pivoting problems. And if your startup has raised an initial round of funding and you run out before making progress and raising another funding round. CB Insights mentions a failed startup called Flud that said this “In fact what eventually killed Flud was that the company wasn’t able to raise this additional funding. Despite multiple approaches and incarnations in pursuit of the ever elusive product-market fit (and monetization), Flud eventually ran out of money — and a runway.” When starting a business you need research and think about all the startup costs such as building the website or app, hiring employees, payroll costs, renting office or coworking space, computer or business equipment, etc.

3) Not the right team: 23 percent

Some startups and small businesses are founded by one person but others are started with having a few people or cofounders. And there are plenty of success stories of college friends think of an idea together and each person brings a different set of expertise or skills that compliment each other. But for all the Uber’s, Paypal’s, Facebook’s, Shazaam’s, Croissants there are plenty of other horror stories, where founding a business with your friends does not work out. Many successful startup stories will attribute having a diverse team with different skill sets as one of the reasons it worked out. But some failed companies will say stuff such as “I wish we had a CTO from the start,” or wished that the startup had “a founder that loved the business aspect of things.” You can’t scale a business without a smart team but the chemistry needs to right. CB Insights mentions a quote from a failed startup called Standout Jobs and they said “…The founding team couldn’t build an MVP on its own. That was a mistake. If the founding team can’t put out product on its own (or with a small amount of external help from freelancers) they shouldn’t be founding a startup. We could have brought on additional co-founders, who would have been compensated primarily with equity versus cash, but we didn’t.”

4) Got outcompeted: 19 percent

It’s not recommended to lose sleep over obsessing about new competitors but do not make the mistake of ignoring them either. Once a new business model or idea gets popular or market validation that people will use it and pay for it, then many more competitors will jump into the space. Having competition is good in the sense that others think its viable business sector, but when similar or copy cat competitors pop up you should understand what they are doing and learn how to articulate or convey to potential customers why your’s is better. Mark Hedland of failed startup Wesabe said “Between the worse data aggregation method and the much higher amount of work Wesabe made you do, it was far easier to have a good experience on Mint, and that good experience came far more quickly. Everything I’ve mentioned — not being dependent on a single source provider, preserving users’ privacy, helping users actually make a positive change in their financial lives — all of those things are great, rational reasons to pursue what we pursued. But none of them matter if the product is harder to use.”

5) Pricing /Cost issues: 18 percent

Pricing is a very important thing for a startup that has a product or service, but getting it right is hard. Many times a company will struggle between with pricing the product high enough to cover costs but also low enough to bring new customers. You need to convey the value of what it costs to what it will bring the customer. The failed mobile analytics startup Delight.io said

“Our most expensive monthly plan was $300. Customers who churned never complained about the price. We just didn’t deliver up to their expectation. We originally priced by the number of recording credits. Since our customers had no control on the length of the recordings, most of them were very cautious on using up the credits. Plans based on the accumulated duration of recordings make much more sense for us and the number of subscription showed.”

6) User un-friendly product: 17 percent

It’s never a good idea to ignore user feedback, and even the best business ideas can be ruined by an unpleasant user experience. Bad things happen when you ignore what a user wants and need, whether consciously or accidentally. If the interface or software is confusing, not intuitive or hard to learn how to use, it won’t get user adoption. Failed startup GameLayers Inc wrote this about their product UI,

“Ultimately I believe PMOG lacked too much core game compulsion to drive enthusiastic mass adoption. The concept of “leave a trail of playful web annotations” was too abstruse for the bulk of folks to take up. Looking back I believe we needed to clear the decks, swallow our pride, and make something that was easier to have fun with, within the first few moments of interaction.”

7) Product without a business model: 17 percent

If you want to get money from an investor, one of the questions you may get asked are things related to “what is your business model” Failed founders seem to agree that a business model is important – staying wedded to a single channel or failing to find ways to make money at scale left investors hesitant and founders unable to capitalize on any traction gained. Basically, it is hard to scale or expand without a solid business model. Investors want to see a clear path to growth to feel comfortable or excited to put money in.

Failed startup Tutorspree wrote, “Although we achieved a lot with Tutorspree, we failed to create a scalable business … Tutorspree didn’t scale because we were single channel dependent and that channel shifted on us radically and suddenly. SEO was baked into our model from the start, and it became increasingly important to the business as we grew and evolved. In our early days, and during Y Combinator, we didn’t have money to spend on acquisition. SEO was free so we focused on it and got good at it.”

8) Poor marketing: 14 percent

It’s crucial to research and understand your target market or customers and how to get their attention and convert them to leads. Ultimately customer acquisition is one of the most important skills of a successful business. But an inability to market was a common failure especially among founders who liked to code or allocated most of the capital into product development and did not spend enough time on promoting or marketing the product. More times than not, it’s the businesses that position their brands as different, authentic, and alluring that stand the test of time. It comes as little surprise then that those businesses that fail to stand out in the crowd are the ones that are forced to close their doors.

didn’t relish the idea of promoting the product. Getting customers, building your brand is not easy and can get ignored because of it. Failed startup Overto said,

“Thin line between life and death of an internet service is a number of users. For the initial period of time, the numbers were growing systematically. Then we hit the ceiling of what we could achieve effortlessly. It was time to do some marketing. Unfortunately, not one of us was skilled in that area. Even worse, no one had enough time to fill the gap. That would be another stopper if we dealt with the problems mentioned above.”

9) Ignore customers: 14 percent

Ignoring users or customers is a tried and true way to fail. Tunnel vision and not gathering user feedback about your product or service are deadly mistakes for most startups. You need to pay attention to your customer’s concerns or questions if you are not listening to their feedback or are providing features or services that they don’t want or use, they may go to your competition. Failed startup VoterTide told CB insights,

“We didn’t spend enough time talking with customers and were rolling out features that I thought were great, but we didn’t gather enough input from clients. We didn’t realize it until it was too late. It’s easy to get tricked into thinking your thing is cool. You have to pay attention to your customers and adapt to their needs.”

10) Product mistimed: 13 percent

Sometimes a product is just too early or too late to market. If you release your product too early, users may write it off as not good enough and getting them back may be difficult if their first impression of you is negative. And if you release your product too late, you may have missed your window of opportunity in the market. The whole first mover vs fast follower paradigm. Try not to get caught up in developing your business idea because without getting it in the hands of users as soon as possible you may not know if people find value in it.

Think about what happened to social media platform Myspace compared the success of Facebook that came later. This is where customer feedback is very important.

Failed startup Calxeda said,

“In [Calxeda’s] case, we moved faster than our customers could move. We moved with tech that wasn’t really ready for them – ie, with 32-bit when they wanted 64-bit. We moved when the operating-system environment was still being fleshed out – [Ubuntu Linux maker] Canonical is all right, but where is Red Hat? We were too early.”

11) Pivot gone bad: 10 percent

Pivots like Burbn to Instagram or ThePoint to Groupon or Glitch to Slack can go extraordinarily well or they can take you down the wrong path and lead to the demise of the business. Few entrepreneurs pivot for the fun of it. Oftentimes, entrepreneurs face a tough decision in a situation with mounting challenges; they may be losing money or facing insurmountable competition or the product or service may not working as they had hoped. Accordingly, they know their startup can’t survive the way it is. A pivot is sometimes the only logical option if they want the business to survive.

Failed startup Flowtab’s explains,

“Pivoting for pivoting’s sake is worthless. It should be a calculated affair, where changes to the business model are made, hypotheses are tested, and results are measured. Otherwise, you can’t learn anything.”

Conclusion

According to recent data from SBE Council, small businesses make up 99.7 percent of U.S. employer firms, and therefore they are the backbone of our nation’s economy. Although failure statistics can serve as a source of angst for some business owners, they can also help entrepreneurs recognize potential risks / pain-points and adapt their business strategy to account and navigate for these issues. Contact Thomas Huckabee CPA for a free consultation, we have helped many San Diego startups and small businesses grow.