With tax season coming soon, many accredited investors may be submitting their tax documents.

Ever receive a K-1 and feel like you’ve been handed a cryptic code instead of a tax document? Or get one without even realizing your investment would generate it? You’re not alone. This guide breaks down exactly what a K-1 is, how the income is taxed, and what to watch out for when you file.

What is a K-1 tax form?

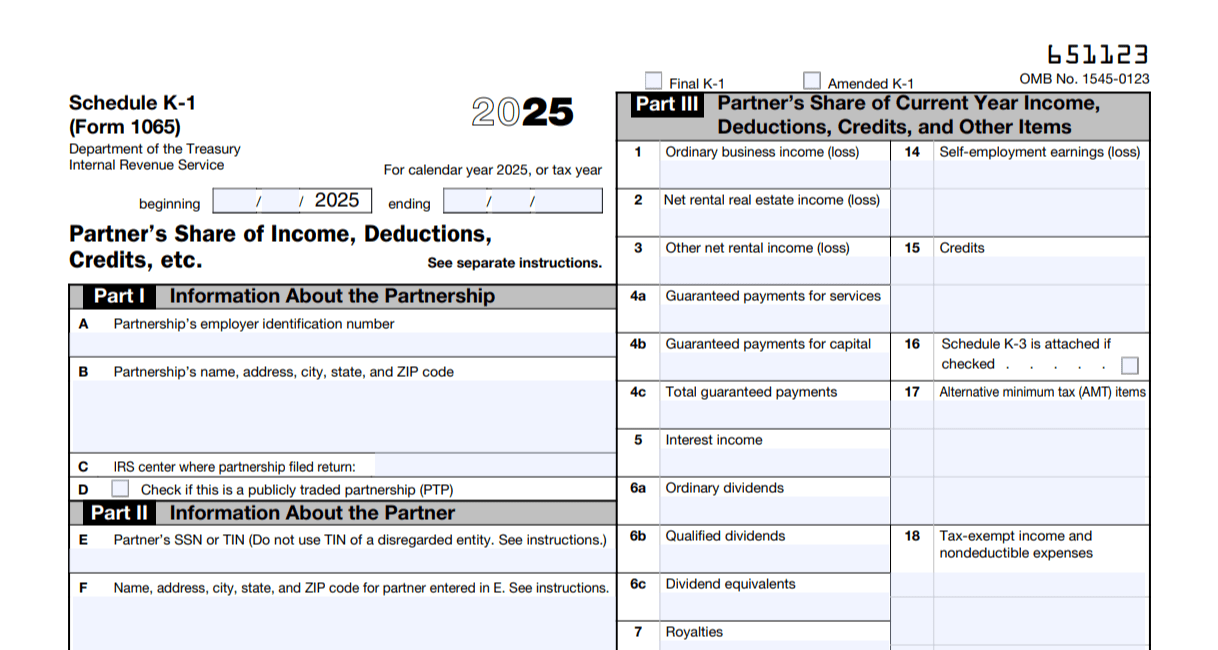

A K-1 is a tax form issued by partnerships, S corporations, trusts, and estates to report each owner’s or beneficiary’s share of income, deductions, and credits. You use the information on your K-1 to complete your personal tax return — similar to how you use a W-2 to report wages from a job, except that no taxes are withheld from K-1 income.

K-1s exist because of “pass-through taxation.” Rather than the entity paying taxes on its income directly, that income flows through to the individual owners, who report and pay taxes on it themselves. This structure prevents double taxation, where the same income would otherwise be taxed once at the business level and again when distributed to owners.

K-1 vs. W-2: What’s the difference?

A W-2 reports wages from which your employer has already withheld income tax, Social Security, and Medicare. A K-1 reports your share of an entity’s income with no withholding — meaning you are responsible for paying estimated taxes on that income throughout the year. It is also possible to receive both a W-2 and a K-1 from the same entity, for example if you are both an employee and a shareholder of an S corporation.

The four types of K-1 forms

While K-1s share a common purpose, there are meaningful differences depending on which entity issues them.

Form 1065 (Partnerships) is the most common. It covers domestic partnerships including LPs, LLPs, and multi-member LLCs. It includes guaranteed payments — amounts paid to partners regardless of the partnership’s profitability — which are treated similarly to a salary and are subject to self-employment tax.

Form 1120-S (S Corporations) is broadly similar to the partnership K-1, but with two notable differences. S corporations do not make guaranteed payments; instead, they can pay shareholder-employees a W-2 salary, which offers more flexibility in compensation planning. Additionally, income passed through an S corporation K-1 is generally not subject to self-employment tax — a meaningful advantage when choosing an entity structure.

Form 1041 (Estates and Trusts) is more distinct. It presents income in a different order, separately reports a beneficiary’s share of depreciation and amortization, and includes a unique section for final-year distributions when a trust is terminated.

Form 8865 (Foreign Partnerships) applies to U.S. taxpayers who are partners in a foreign partnership. It reports the U.S. partner’s share of the foreign partnership’s income, deductions, and credits, and can trigger additional foreign reporting obligations.

Read the K-1 footnotes carefully

The first page of a K-1 — often called “the face” — is just the starting point. Many K-1s include additional pages of footnotes that detail the sources, treatment, and reallocation of income and deductions. These footnotes can trigger foreign reporting requirements, additional state tax filings, and nuanced details around gain characterization (such as QSBS and carried interest), stock cost basis, and crypto distributions, among other things.

Even a straightforward K-1 can raise questions. More complex ones can pose significant challenges, often requiring expert knowledge to navigate the reporting requirements correctly.

How is K-1 income taxed?

How K-1 income is taxed depends on its category. There is no single rate — each type of income carries its own tax treatment.

Ordinary business income and interest income are taxed at the recipient’s ordinary income tax rate.

Dividend income is split: qualified dividends are taxed at the lower long-term capital gains rate, while non-qualified dividends are taxed as ordinary income.

Capital gains follow a similar split. Long-term gains are taxed at preferential rates of 0%, 15%, or 20% depending on the taxpayer’s income level, while short-term gains are taxed as ordinary income.

Rental income is taxed as ordinary income and may also be subject to passive activity loss rules.

Guaranteed payments are taxed as ordinary income and, for partners in a partnership, are also subject to self-employment tax.

You may owe taxes even if you received no cash (phantom income)

This is one of the most important — and often surprising — aspects of K-1 income. The taxes you owe are based on your share of the entity’s taxable income, not on what was actually distributed to you. This is sometimes called phantom income: taxable income you are required to report and pay taxes on even though you never received the cash.

An entity can generate taxable income and choose to reinvest it rather than distribute it to owners. Even so, you are still responsible for reporting and paying taxes on your share.

Distributions shown on line 19 of a K-1 generally have little impact on your taxable income for the current year — they typically represent cash that was already taxed in a prior year.

Example: If you are a partner in a partnership that earned $200,000 in taxable income but reinvested all of it without distributing a dollar to partners, you would still owe taxes on your proportionate share of that $200,000 at your personal tax rate.

What to do when you receive a K-1

- Don’t file your personal return until you have it. K-1s are often issued after the April 15th individual filing deadline. If you are expecting a K-1, you may need to file an extension.

- Review the footnotes. Don’t stop at the first page. The additional pages can contain information that affects your state tax obligations, foreign filing requirements, and more.

- Make sure the numbers match your records. Check your capital account balance and any distributions against your own statements.

- Report everything on your personal return. K-1 income flows primarily to Schedule E of Form 1040. Guaranteed payments and self-employment income flow to Schedule SE.

- Adjust your estimated tax payments. Since no taxes are withheld from K-1 income, you are generally required to make quarterly estimated tax payments to avoid underpayment penalties.

Why K-1s can be frustrating

K-1s are essential documents, but they come with real challenges.

Complexity is the most common complaint. K-1s require a solid understanding of the tax rules that apply to partnerships, S corporations, trusts, and estates — and errors in reporting can have consequences.

Timing is another issue. K-1s are often issued after the April 15th individual filing deadline, forcing many taxpayers to file extensions.

Multiple K-1s compound the complexity for taxpayers involved in several entities, each with its own reporting requirements.

Passive activity loss rules can limit a taxpayer’s ability to deduct losses against other income.

Estimated taxes must typically be paid quarterly, since entities do not withhold taxes on behalf of their owners.

Phantom income, as described above, can create cash flow challenges when taxes are owed on income never received in cash.

Audit risk increases when there are errors or discrepancies on K-1s, potentially leading to additional taxes, penalties, or interest.

Inheriting K-1 tax obligations

K-1s play a particularly important role when an estate or trust reaches the end of its existence. When a trust is terminated, the final Form 1041 and its accompanying K-1s allocate all remaining income, deductions, and credits to the beneficiaries, who then report those items on their personal returns. Handling this correctly is essential for IRS compliance and for ensuring beneficiaries receive any available tax benefits. Capital losses and other deductible expenses from the trust can carry over to a beneficiary’s personal return, potentially reducing their taxable income going forward.

Frequently asked questions

When will I receive my K-1? K-1s are typically issued after the regular April 15th tax filing deadline, which is why extensions are common for taxpayers who receive them. There is no single IRS deadline for issuing K-1s — it depends on when the entity files its return.

Do I have to file an extension if I haven’t received my K-1? In most cases, yes. If you know you are expecting a K-1 and haven’t received it before your filing deadline, it is generally advisable to file for an extension to avoid filing an inaccurate return.

Can I owe taxes on a K-1 if the partnership lost money overall? It depends on your specific share of income and loss, as well as passive activity loss rules. Even if the entity as a whole had a net loss, certain income items on your K-1 may still be taxable.

Does K-1 income affect my self-employment tax? It depends on the entity type and the nature of the income. Guaranteed payments from partnerships are subject to self-employment tax. Income from an S corporation K-1, by contrast, is generally not — which is one reason entity selection matters.

What if I receive K-1s from multiple entities? Each K-1 must be reported separately on your return. Coordinating multiple K-1s, particularly those with different income types and state-level implications, is one of the more complex aspects of tax filing for investors in pass-through entities.