With a significantly reduced workforce, the IRS’s ability to conduct audits, its primary tool for identifying tax return issues, is in question. While a decrease in audit activity might seem inevitable, tax experts argue that the agency’s remaining enforcement capabilities shouldn’t be underestimated. The news publication Marketwatch reported that the Trump administration’s efforts to trim government ranks led to around 7,000 fewer IRS compliance personnel, although court orders temporarily reversed some of these cuts. Moreover, approximately 5,000 IRS employees accepted buyout packages.

The initial stages of more substantial IRS staff cuts are underway, with further departures anticipated after next week’s tax season. This includes Acting Commissioner Melanie Krause, who reportedly resigns following an information-sharing agreement with ICE. Rochelle Hodes of Crowe notes that the consequences of these cuts include abruptly stopped audits, suddenly transferred cases, and audits that never begin, alongside ongoing investigations. She added, “I’m attempting to understand a pattern but haven’t been able to.”

Tax attorney Travis Thompson at Boutin Jones said the disruption is directly affecting taxpayers. He cited two instances in the past month where IRS staff responsible for audit appeals were absent for scheduled calls about his clients’ audit cases. Other tax attorneys have not experienced any sudden changes or pauses in the audits they defend their client cases against.

How often does the IRS audit taxpayers?

Under the Biden administration, the Internal Revenue Service announced intentions to increase audit scrutiny of wealthy individuals and businesses. However, this shift came against a backdrop of historically low audit rates across the tax system. In 2019, according to the agency’s most recent finalized audit data, the IRS examined fewer than 0.5% of all individual income tax returns.

Outlook for Average Taxpayers

Tax experts anticipate minimal changes in audit likelihood for typical income earners under the Trump administration’s IRS leadership. The existing automated compliance systems that flag potential issues among standard returns are expected to continue functioning similarly.

Audit Stability for Wage Earners

“For W-2 employees and 1099 employees, I don’t think there’s much change,” explains Travis Thompson, a tax professional familiar with IRS enforcement patterns. This stability applies to:

- Traditional employees receive W-2 forms reporting wages and withholding

- Independent contractors and gig economy workers receiving 1099 forms

Thompson notes that much of the review process for these standard income reporting methods is already automated, making these systems less susceptible to policy shifts between administrations.

According to tax professionals, the IRS’s ability to identify tax errors will likely depend on the complexity of the return. Automated reviews may still catch simple discrepancies, but the nuanced issues often found in high-income and corporate filings could be missed due to fewer enforcement personnel. Rochelle Hodes from Crowe LLP predicts a shift towards computer-based audits due to staff reductions, potentially making the audit process more challenging for taxpayers. A Treasury spokesperson told MarketWatch that these staffing changes aim to enhance the IRS’s revenue collection and taxpayer services.

If history is any indication, assuming that recent reports of paused or scaled-back audits mean wealthy taxpayers will avoid scrutiny under Trump’s IRS could be misleading.

Back in 2020, during Trump’s first term, Treasury Secretary Steven Mnuchin directed the IRS to audit at least 8% of tax returns reporting over $10 million. However, the IRS later told a Treasury watchdog that it abandoned that target because many audits failed to uncover additional taxes owed. The agency said it has since shifted its focus under the Biden administration to prioritize audits of businesses, partnerships, and households earning more than $400,000 annually.

Krause will remain acting commissioner until at least May 15, and according to a Treasury spokesperson, she will continue leading efforts to modernize and restructure the IRS in the meantime.

Republicans have steadily reduced IRS funding for tax enforcement over the years

In 2022, President Biden signed the Inflation Reduction Act, allocating $80 billion to the IRS over a decade. Republicans opposed the measure, citing concerns about overly aggressive audits and inefficient spending. Their efforts to claw back IRS funding have drawn criticism for appearing soft on wealthy tax evaders.

Of the $80 billion, around $5 billion was earmarked for modernizing outdated IRS technology—some of which still includes fax machines. For instance, after not hearing back from IRS staff, taxpayer Thompson had to fax a letter just to document his outreach.

Roughly $45 billion was designated for enhanced enforcement efforts targeting high-income earners and businesses making over $400,000, with the remainder going to operations and customer support.

In late 2023, the IRS began hiring and launching new programs to collect unpaid taxes from wealthy individuals and audit complex entities like hedge funds and complex law firm partnerships. But Republican-led efforts have significantly reduced that enforcement funding—about $20 billion was stripped following 2023 debt ceiling talks, and another $20 billion was rescinded through a recent spending deal, according to a House Appropriations Committee aide.

Despite political divisions, many experts agree that investing in better IRS customer service is worthwhile—not just for taxpayer satisfaction but also because it improves compliance and tax revenue by helping filers navigate the system correctly.

IRS audit rates differ depending on income level

“Broadly speaking, the IRS will likely maintain its focus on wealthier taxpayers,” stated Eric Hylton, national director at Alliantgroup. This includes increased scrutiny of issues such as questionable Puerto Rican residency claims, shell corporations used by contractors, and underreported cryptocurrency earnings.

Hylton acknowledged that reduced staffing might limit the agency’s ability to execute these priorities fully. “If the stated priorities remain, but there are fewer personnel, then logically, fewer actions may be taken. Hopefully, technological advancements can help bridge that gap.” However, he cautioned that the widespread effectiveness of AI in tax enforcement is still some time away.

Tax attorney Travis Thompson emphasized that ensuring compliance among high-income individuals requires specialized expertise within the IRS, particularly in understanding the complex tax laws related to partnerships, high-net-worth individuals, pass-through businesses, and other sophisticated entities.

Turning to working-class taxpayers, a significant audit area revolves around the Earned Income Tax Credit (EITC), a complex provision where eligibility and payout amounts depend on the number of qualifying children in the household.

For the 2019 tax year, IRS data indicates that less than 1% of tax returns claiming the EITC were audited. These audits were typically conducted through mail correspondence, and the IRS ultimately recommended that taxpayers pay an additional $1 billion collectively as a result.

According to reports, audit rates for EITC claims decreased under the Biden administration following concerns about racial disparities in these audits. Megan Nassau has observed this decline and is “curious to see if the IRS decides it’s one area it can ramp up enforcement in.”

Conclusion

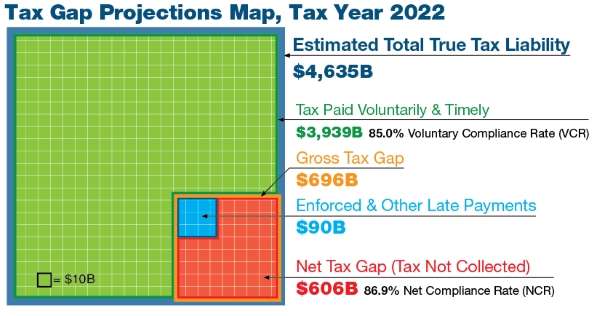

In fiscal year 2023, the IRS collected nearly $40 billion through audits and other enforcement efforts—a small fraction compared to the estimated $600+ billion tax gap for 2022, which represents the difference between taxes owed and taxes actually paid, even after enforcement actions, according to the IRS’s most recent estimates.

Some accountants have had to dissuade clients from skipping their tax filings, reminding them that the IRS still has tools to pursue noncompliance. As the IRS evaluates how aggressively to audit high-income individuals and corporations, the Trump administration must weigh how a more lenient approach could affect federal revenue and Treasury funding.