10 Common Payroll Errors a Small Business Must Avoid

In order for a company to grow, prosper and operate, it is imperative that a business engages its employees. The issue with this reality is that engaging employees comes at a cost to a business because it will give an employer several more, and often complicated, responsibilities. Failing to comply with such responsibilities can have dire consequences. Running afoul of these duties can trigger severe penalties, and can also impact the bottom line of a business, as certain tax saving advantages may be overlooked. The IRS extended $6.1 billion dollars in payroll tax penalties in 2016 fiscal year. In addition to IRS taxing requirements like unemployment, each state, county, locality and district has its own filing and paying requirements. In just one year, a small business with three employees could end up with more than 10 to 30 tax returns that need to be filed with federal and state revenue agencies. Payroll is not as easy to understand as some may believe; there are many facets to it that, when ignored, can result in mistakes. In light of this, we have compiled a list of 10 payroll errors to avoid.

In order for a company to grow, prosper and operate, it is imperative that a business engages its employees. The issue with this reality is that engaging employees comes at a cost to a business because it will give an employer several more, and often complicated, responsibilities. Failing to comply with such responsibilities can have dire consequences. Running afoul of these duties can trigger severe penalties, and can also impact the bottom line of a business, as certain tax saving advantages may be overlooked. The IRS extended $6.1 billion dollars in payroll tax penalties in 2016 fiscal year. In addition to IRS taxing requirements like unemployment, each state, county, locality and district has its own filing and paying requirements. In just one year, a small business with three employees could end up with more than 10 to 30 tax returns that need to be filed with federal and state revenue agencies. Payroll is not as easy to understand as some may believe; there are many facets to it that, when ignored, can result in mistakes. In light of this, we have compiled a list of 10 payroll errors to avoid.

1. Inadequate Bookkeeping

Federal and state laws require a business to maintain payroll records. Normally, the timeframe for maintaining these payroll documents is at least four years. These records are to be made accessible and available to the IRS and include, but are not limited to, the following:

- Time sheets

- Additional records of hours worked

- Additional relevant payroll data

- Copies of W-2s

- Copies of I-9s

- Expense accounts

- Accident reports

2. Delegating Payroll Obligations

Although some small business have in-house payroll specialists, most businesses choose to outsource payroll to other companies or people. These outsourced companies or people include bookkeepers, accountants, payroll companies or professional employer organizations (PEOs), all of which take care of withholding determinations, payroll tax return filing and tax deposits.

To be fair, most arrangements with outsourced companies work well but, unfortunately, there are payroll specialists who do not meet their specified obligations. When these unfulfilled obligations, on the part of a payroll specialist, are not met, the employer will experience negative repercussions because it is the employer’s duty to monitor the way payroll is handled. Fortunately, the IRS periodically updates a list of certified PEOs which meet its standards.

3. Giving Compensation Time

Hourly employees, also known as non-exempt employees, are paid time and a half should they work more than 40 hours in a week. Make no mistake- there can be no avoidance of paying a worker overtime; especially of note is that a business cannot offer a non-exempt employee compensation time in lieu of the time and a half pay that worker should receive. The Fair Labor Standards Act (FSLA) governs overtime and comp time regulations in the United States and will violate a company if it is not in compliance.

4. Lack of New Employees Completing Form 8850

As a business owner, it is fairly impossible to look at a new hire and determine whether or not that employee is in a targeted group which would allow the business to claim the work opportunity credit. Therefore, make sure that all new employees complete the IRS Form 8850, which is used to pre-screen new hires for credit eligibility. After the form is fully completed, it needs to be remitted, by no later than the 28th calendar day following the date the targeted employee begins working for a business, to a state employment security agency (SESA). If a company fails to do this, it could miss out on work opportunity credits to which it is entitled.

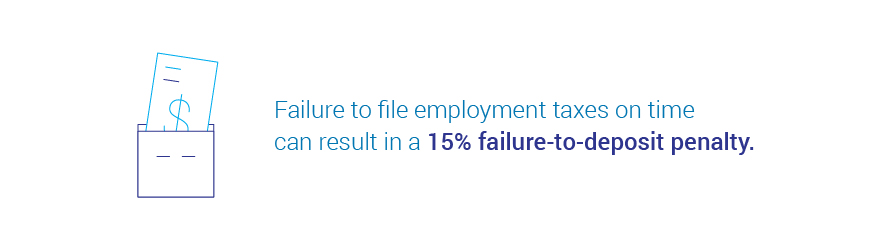

5. Depositing and Reporting Employment Taxes Incorrectly

After you’ve collected payroll taxes from your employees and contributed your share, you need to submit those taxes to the federal, state, and local tax authorities. You can opt to file those taxes on one of two different schedules, but failing to file them on time could result in a 15 percent failure-to-deposit penalty, according to the IRS.

6. Classifying Employees Improperly

6. Classifying Employees Improperly

If a person is a business’ employee, that business owes payroll taxes on that worker’s taxable benefits and wages. Labeling an employee as an independent contractor, when he or she is a legitimate employee, is illegal and will not help a company avoid taxes associated with an employee. The IRS guidelines on worker classification should be used as a point of reference.

7. Non-accountable Plan for Reimbursing Travel and Entertainment (T&E)

If a business reimburses workers for T&E expenses while conducting company business, that business may be paying unnecessary employment taxes if the reimbursement process is not arranged properly. If an employee simply requests a reimbursement and the business pays it, the reimbursement is taxable to the employee and thus subject to payroll taxes. Alternatively, a company can adopt an “accountable plan,” whereby the reimbursement isn’t taxable to the worker and the business doesn’t owe payroll taxes. With this arrangement, a business can deduct the T&E expenses. To be an accountable plan, following IRS guidelines is critical.

8. Paying Creditors Before the Government

A company must be certain to put the IRS at the top of its list if it is experiencing a cash crunch. Payroll taxes should be paid first, even if landlord or other creditors are also requesting payment. A business owner will become personally liable for all outstanding taxes despite the fact that the respective business may be incorporated or established as an limited liability company. A trust fund recovery penalty could be assessed if a company does not make payroll taxes a priority.

9. Postponing Final Paychecks

An employee who resigns or is terminated will usually be owed a final paycheck. Although federal law does not stipulate that the former employee be paid immediately, state law may. Violation of any laws could result in legal action or strong penalties. The rules pertaining to each state can be found here.

10. Ignoring Claims for Unemployment

An application for unemployment compensation may be filed by a worker if that worker departs his or her job at a company. However, certain circumstances, such as a voluntary departure or serious workplace misconduct, including but not limited to intoxication at the job, sexual harassment or theft, mean that the former employee is not entitled to collect unemployment compensation benefits. When unemployment claims are made by former employees guilty of any of the above reasons, the claims are considered erroneous. An erroneous claim that is not detected or challenged will result in a company paying unnecessarily larger state employment taxes.

11. Lacking Employment Posters

A business is legally required to post and display posters for certain state and federal employment laws. If a business fails to do so, it will be monetarily penalized depending on the type and content of the poster that was supposed to be displayed. The Department of Labor’s Poster Advisor is the best resource that a company has for determining which posters are required by federal law. For state required postings, a business should consult its state labor department. Fortunately, most required posters can be downloaded from government websites.

Conclusion

If you want your business to succeed, consider leaving payroll and accounting matters to trusted professionals. As a small business owner, don’t spend your time trying to understand payroll maintenance, accounting software and data entry; spend your time building your business. Thomas Huckabee, CPA of San Diego California is an expert small business CPA who can help you succeed. Please contact our office for further information.

![]()

{kind=link}