Tax Reform’s Implications of the 20% Pass-through Entity Income Section 199a

Understanding the 20% Qualified Deduction for Pass-through Income

Fundamentals of the TCJA’s New Business Tax Legislation

On December 22, 2017, the Tax Cuts and Jobs Act (TCJA) was enacted into law. In code section 199A, the Act’s focus is on particular pass-through income and allows for a 20 percent deduction on that income, in some instances. Please note that, for the purpose of the 20 percent deduction, the TCJA is referring to pass-through income for sole proprietorships, LLCs, partnerships and S corporations. If you don’t already know what a pass-through entity (PTE) is – pass-through entities are businesses (set up as a special business structure for the purpose of reducing the effects of double taxation) that don’t pay the corporate income tax or any entity-level tax. But, rather, the profits “pass through” to the owners of the business. And then the owners report that income on their individual tax returns and pay tax on it, along with the rest of their normal income.

On December 22, 2017, the Tax Cuts and Jobs Act (TCJA) was enacted into law. In code section 199A, the Act’s focus is on particular pass-through income and allows for a 20 percent deduction on that income, in some instances. Please note that, for the purpose of the 20 percent deduction, the TCJA is referring to pass-through income for sole proprietorships, LLCs, partnerships and S corporations. If you don’t already know what a pass-through entity (PTE) is – pass-through entities are businesses (set up as a special business structure for the purpose of reducing the effects of double taxation) that don’t pay the corporate income tax or any entity-level tax. But, rather, the profits “pass through” to the owners of the business. And then the owners report that income on their individual tax returns and pay tax on it, along with the rest of their normal income.

Though LLCs are a legal structure, they aren’t recognized by the Internal Revenue Service for tax purposes. You’ll need to tell the IRS how your business should be levied. To do that, you’ll file a Form 8832 with the “tax man” to indicate how you’d like to be levied: as a corporation, a partnership or as part of your personal tax return.

Because of the ambiguity, combined with myriad exceptions and limitations, as to the types of businesses that may be eligible for the deduction, code section 199A is notoriously complicated and intricate, particularly when compared to other code changes in the TCJA. In fact, practically every provision in the code is directed to Congress or the Treasury Department for issue clarifications.

A majority of code 199A’s calculations, such as the limitations phase-ins or the preliminary deduction, occur at the business or trade level. After these aforementioned calculations are determined, remaining revenue amounts are summed up at the taxpayer level and combined with existing taxpayer income, to garner the overall taxable income limitation.

When the complexity of code 199A is taken into consideration, our mission is to educate our audience on the fundamentals of the pass-through income deduction. We want this to be achieved by covering and reporting on just enough details to not overwhelm readers with all the particulars.

High-level Overview

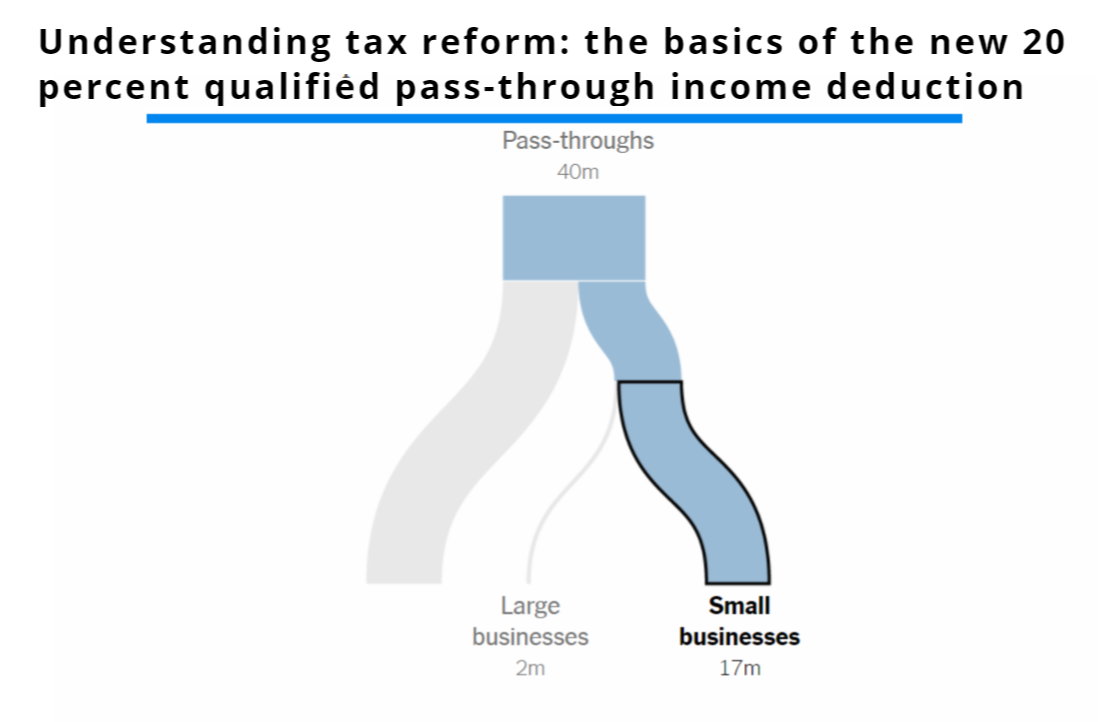

Taxable years before January 1, 2026, and after December 31, 2017, the TCJA is allowing for noncorporate taxpayers, including trusts, estates, and individuals, to take a deduction in the amount of 20 percent of their respective qualified business income (QBI) from sole proprietorships, LLCs, partnerships, and S corporations.

Normally, qualified items of deduction, loss, income, and gains will allow a business to qualify for the deduction, as long as the deduction is with respect to a qualified trade or business. The specifications of qualifying income are that said income is generated by U.S. sources; this excludes numerous investment-related items like nonbusiness interest income, dividends and capital gains and losses.

Compensation of a reasonable amount must be paid to the taxpayer in addition to any and all guaranteed payments for partnership which are not included in QBI. Any services rendered to a partnership are not deduction candidates either and they will also be excluded from QBI. In its current state, the TCJA describes a mandated process whereby each business passes through allocable shares of income or loss to its respective shareholders and/or partners. It then becomes the taxpayer’s burden to determine and file for each deduction related to each business or trade before combining all the deductions from each business or trade. A net QBI less than zero will be carried over into the next taxable year and also included in the calculation of qualified of business income or qualified trades for that same year.

The first important detail to note here is that the deduction is not permitted in computing adjusted gross income (AGI.) Rather, it is a deduction that lowers taxable income. Essentially, this means that these pass-through deductions have no impact on the limitations surrounding or based on AGI. Essentially, this also means that this deduction doesn’t touch self-employment (SE) income or net investment income (NII.) Also of note is that this deduction is permitted regardless of whether or not itemized deductions are filed by a taxpayer.

Parameters & Limitations on Varieties of Qualifying Income-Service Businesses

Both chambers of Congress agreed to exclude particular “specified service trade or business” revenue from qualifying for the deduction. As far as the 20 percent pass-through deduction is concerned, if a “specified service trade or business” is one that involves the performance of services rendered in the fields of accounting, actuarial science, financial services, brokerage services, health, law, performing arts, consulting, athletics or any other type of business or trade in which the principal asset is more or less considered to be a skill or the reputation of one or more of its owners or employees, the deduction is not permitted.

The final portion of the definition is already thought to be the most difficult portion to understand and will, for the most part, require additional support, guidance and clarification from the IRS. In fact, it is anticipated that many disputes between the IRS and taxpayers will be the result of this final portion. As an example, an individual who has mastered the trade of plumbing could easily fall into the category of a “specified service trade or business” that is excluded from qualification for the 20% pass-through deduction. The reasoning behind this high-level example of exclusion is simply that the taxpayer’s skill and mastery is considered the primary skill or principal asset of the respective business. Also deemed to be excluded by the new legislation are specified services conducted in the investment industry such as investment management and trading.

The final portion of the definition is already thought to be the most difficult portion to understand and will, for the most part, require additional support, guidance and clarification from the IRS. In fact, it is anticipated that many disputes between the IRS and taxpayers will be the result of this final portion. As an example, an individual who has mastered the trade of plumbing could easily fall into the category of a “specified service trade or business” that is excluded from qualification for the 20% pass-through deduction. The reasoning behind this high-level example of exclusion is simply that the taxpayer’s skill and mastery is considered the primary skill or principal asset of the respective business. Also deemed to be excluded by the new legislation are specified services conducted in the investment industry such as investment management and trading.

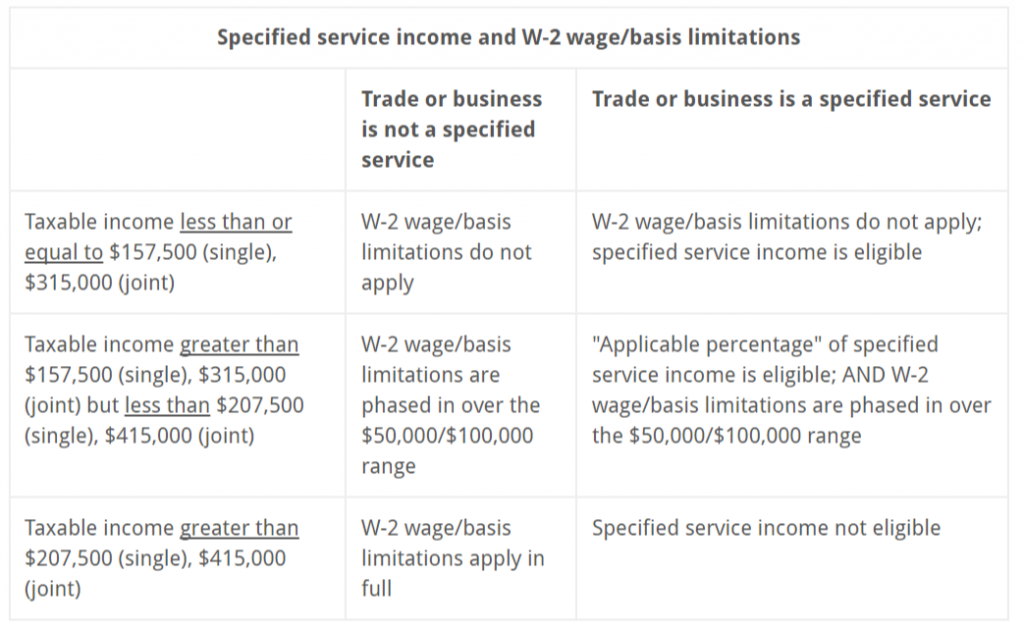

Despite the fact that most specified business or service trade income does not ordinarily qualify for the pass-through deduction, the legislation contained in the TCJA has identified exceptions that are based taxpayer taxable incomes. As an illustration of this, if the taxable income of joint filers is below $315,000, prior to factoring in the deduction, the joint filers would be eligible for the deduction. By the same token, should joint filers have a taxable income is between $315,000 and $415,000, a lower percentage of specified service income is eligible. Taxable income which exceeds $415,000 for joint filers will not have business income or specified service trade income that will qualify for the deduction. The table below elaborates further on taxable income limits and corresponding W-2 wage/basis limits:

(image credit Baker Tilly)

(image credit Baker Tilly)

The deduction is available to electing small business trusts as well as individuals, and owners are allowed to calculate their maximum deduction based on either 50 percent of their share of W-2 wages paid or a combination of 25 percent of their share of W-2 wages paid plus 2.5 percent of the unadjusted basis of all qualified property. Carried interest income retains its treatment as a capital gain, although it will be subject to a longer holding period (three years as opposed to one year in prior law) in order to qualify. Additional provisions covered include:

- Accuracy-related penalty applied to the 20 percent deduction

- Repeal of technical termination of partnerships

- Recharacterization of certain gains in the case of partnership profits interests held in connection with performance of investment services

- Tax gain on the sale of a partnership interest on lookthrough basis

- Modification of the definition of substantial built-in loss in the case of transfer of partnership interest

- Charitable contributions and foreign taxes taken into account in determining limitation on allowance of partner’s share of loss

- Loss limitation rules applicable to individuals

- Special subchapter S provisions

An alternate type of income that can often be overlooked or lost in the shuffle is income derived from a rental property. In such a case, the 20 percent pass-through rate is permitted for business income and qualified trade income. Confusion surrounds the question as to whether a rental should be considered and treated as a business or if it should be considered and treated a trade. For instance, a rental activity in which an owner’s activity is strictly limited to collecting rents and paying real estate taxes (triple net lease situations) is not be considered a business or trade or business.

Taxable Income Limitations

Following the determination of 20 percent of a combined business income for all trades or businesses heavily depends upon taxable income. If applied, the deduction is not permitted to exceed 20 percent of the respective taxable income in excess of net capital gains. Definition-wise, net capital gains, for the purpose of this example, encompasses dividends and capital gains, which qualify for a favorable tax rate (such as the maximum 20 percent rate for capital gains.)

This represents a significant possible tax break for business owners, but it comes hand-in-hand with a tremendous deal of complexity, confusion and uncertainty, as it stands right now. It remains to be seen how existing tax forms will be altered and modified to allow for the new deduction, or even what precise information will be required for reporting by partnerships and S corporations to their respective owners to even calculate deduction.

Conclusion

“Some of my clients who are currently C-corporations, it may be worth electing S-corporation status for the first time, because if you do a side-by-side, it’s a lot better.”

In order for your business to achieve success, it must leave accounting details to the professionals. Collaborating with a CPA firm will give you peace of mind because you will know that your business’ accounting practices are in good hands. Thomas Huckabee, CPA of San Diego, California is a small business accountant expert who can help you succeed. Please contact our office for further information.

{kind=link}