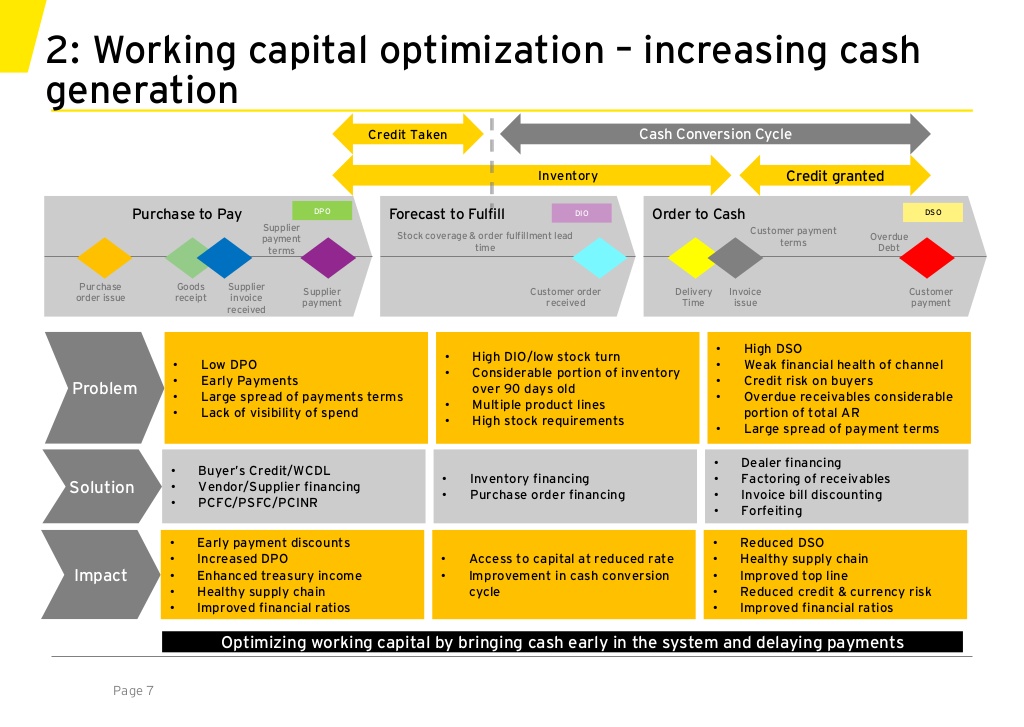

Working Capital Optimization

In good times and bad economic times, a relentless focus on cash flow and efficiency is a crucial part to the success of an organization.

In good times and bad economic times, a relentless focus on cash flow and efficiency is a crucial part to the success of an organization.

Working capital optimization is a CFO level managerial accounting strategy that focuses on maintaining efficient levels of working capital, current assets, and liabilities during all economic cycles. There are a lot of companies, especially in consumer products and industrial sectors which remain capital intensive, see a high level of inventory, low levels of turnover for accounts receivable and higher turnover on the accounts payable side, which could benefit from working capital cash flow management services.

Working capital optimization plans are engineered to improve a business balance sheet and cash flow in order to meet its operating expenses and short-term debt obligations. If there’s a shortage of working capital, the cash flow will also be adversely affected and you’ll not have enough money to run your operations or make more business investments. Ultimately this will can have an adverse effect on the health of the company.

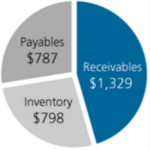

- Working capital – in a business context, is the excess money you have on hand when your short-term assets are greater than your short term liabilities.

- Short term assets – include accounts and notes receivables, any short duration saleable securities, company inventory and any prepaid expenditures.

- Short term liabilities – are your short-term debts, line in credit, short duration payables, long-term debt payment installments and other accumulated expenditures.

- Working capital ratio – is calculated by dividing the sum of your short term assets by the sum of your short term liabilities.

The goals of working capital optimization are to better optimize the balance between assets and liabilities, and since not all assets can be disposed or acquired on a regular or short time basis, it more focuses on optimizing the cash on hand ratio to (and liquid assets that can that can be converted into cash-on-hand within a 90 day period cycle) liabilities. An interim CFO will think about ways to manage the working capital of your company well and determine which elements are the most important. Some of the factors that are common to many companies can include:

- Investments that you make in the business

- The amount of inventory or the inventory worth

- The amounts payable and amounts receivable.

These elements are usually used to convey the financial strength of a company and how efficiently it is operating.

One might think that excess cash signifies that a company is doing great financially. This is not always the case. There can some circumstances where having excess cash could signify an operational inefficiency. Keeping high cash reserves is not a point to brag about unless you are investing it in the most efficient manner. As an example, is your business giving more returns for the cash internally than it would have got you if you’d have kept it externally?

Converting Your Cash

When your business gets profits, one of the ways you can use is to improve your receivables account. When you are selling something on an open account you need to first buy them with cash before you sell them to get cash. This is not only related to the inventory to purchase but also for selling business services as well. The conversion of cash to business resources and vice versa can be an indicator of how healthy your business model is.

But you may be wondering how to calculate the cash conversion cycle. It is a fairly simple process; where you add up the total time taken for holding the inventory, the time taken for making your cash payments and the time taken to collect the receivables. As an example, say you hold your inventory for 90 day, take 25 days to collect the receivables and take 15 days for making your payments. Your cash conversion cycle would be calculated as 90 + 25 – 15, which equals 100 days. You would then add the carrying costs of the conversion cycle to the sales price of the inventory.

Customers and Suppliers Value Drivers

Thomas Huckabee, CPA, works with companies to help optimize their inventory cycles, receivable collections, and supplier payment terms. In other words, we try to reduce inventory cycles and net cash flows on receivables and payables (by collecting receivables faster and extending payments terms longer).

Thomas Huckabee, CPA, works with companies to help optimize their inventory cycles, receivable collections, and supplier payment terms. In other words, we try to reduce inventory cycles and net cash flows on receivables and payables (by collecting receivables faster and extending payments terms longer).

These are all solid strategies for optimizing working capital, but if they are not managed correctly, then supply chain costs can increase. As an example, if you try to force your customer to pay before it can afford to and the customer then has to borrow to do so, that is going to its cost to service their own customers, and if their customer can’t pay, your customer may end up asking you for price reductions at contract renewal time, and that is not a positive and or a good outcome from either parties involved.

If you try to reduce inventory turn-over too aggressively, you will end up doing a lot of expediting or less-than-truckload shipments, which will reduce overall acquisition costs in the long run. And if you extend payment terms beyond which your suppliers can afford, at minimal you risk increasing your costs substantially as they will have to borrow at high financing rates and pass that cost onto you and you could even put their financial solvency at risk. The techniques used for managing differ from business to business and situation to situation.

So how what are some strategies for optimization of each of these areas?

- Inventory Cycle Optimization – (forecast-to-fulfill) You can optimize inventory (carrying) costs versus logistics costs versus a potential loss from

stock-outs and determine the optimal inventory cycle for each product or commodity.

stock-outs and determine the optimal inventory cycle for each product or commodity.

- Accounts Receivable Collection – (source-to-settle) You can start by targeting slow customers, but also focusing on the ones with the most ability to pay first. For public businesses, you can use publicly available financials to determine who is cash rich. For private organizations, you can look at a credit rating data, such a one provided by Dun & Bradstreet.

- Payment Terms Extension – (customer-to-cash) you should try to figure out which suppliers can afford payment extensions such that they would not suffer any negative impact or where the overall supply chain cost that would be borne by the end consumer is lessened and extend the terms.

Conclusion

Real world working capital cash flow management is more complex than the basic ideas listed in this article. There are many other factors to think about such as tax issues, capex efficiency and expenditures and last in first out inventory reserves (LIFO), beyond balance sheet financing, which can play role in making the job of real world working capital management more complex. And when it’s time to reinvest your cash, Thomas Huckabee, CPA can help you identify target areas and integrate assets into your growing business. For companies focused growth and determined to steer strategy, there may be no better place to look for that cash than in working capital improvements.

{kind=link}