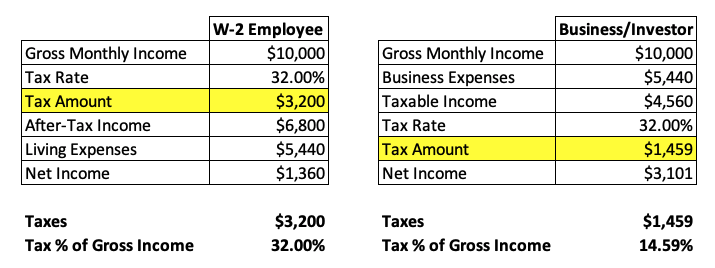

Did you know that as a W-2 employee, you pay the highest taxes? Higher than businesses and investors? No group in America pays more taxes than high-salary wage earning W-2 employees. Whether you are a successful senior executive or engineer in the tech industry, a professional athlete or physician with a high salary, tax planning should be a key component of your wealth management strategy.

W-2 employees are taxed on their gross income first, with the IRS taking a portion before they receive their paycheck. In contrast, businesses and correctly structured investors pay taxes on their net income after expenses and pay the IRS quarterly. This allows business owners and investors to use their money before deducting taxes. For example, Instead of investing in your personal name, John Smith; invest as John Smith, Inc. or John Smith, LLC. When you invest through a properly structured entity, your investment income gets the same tax treatment as a business.

The IRS defines a high-income earner as any taxpayer reporting $200,000 or more in total positive income (TPI) on their tax return. TPI is the sum of all positive amounts from various income sources listed on an individual’s tax return. Although in places such as San Diego, San Francisco or New York City, which are very expensive to live, high income earners might be defined more as people making $400,000 or more each year. In 2024, the top tax rate of 37% applies to those earning over $609,350 for individual single filers, up from $578,125 last year.

The IRS defines a high-income earner as any taxpayer reporting $200,000 or more in total positive income (TPI) on their tax return. TPI is the sum of all positive amounts from various income sources listed on an individual’s tax return. Although in places such as San Diego, San Francisco or New York City, which are very expensive to live, high income earners might be defined more as people making $400,000 or more each year. In 2024, the top tax rate of 37% applies to those earning over $609,350 for individual single filers, up from $578,125 last year.

W-2 salaried employees have fewer tax planning options than business owners but still have some opportunities. Strategies are still available to optimize their tax situation and reduce their overall tax burden. When building wealth for retirement, individuals often focus on generating income and managing their investments. However, it’s crucial to understand that minimizing taxes is equally important to increase asset value.

As the saying goes, “It’s not what you make but what you keep that counts.” You can retain more investment returns by strategically managing your tax exposure.

1 Max out your 401k at work

You also have the choice between Roth (post-tax) and Traditional (pre-tax) 401 (k) plans. 401(k) plans allow you to make up to $22,500 of your own contributions a year, and then you can go above that with your employer match.

Contribute the full $23K pre-tax you can as an employee and get your full employer match. Total contributions are capped at $69K / year, so see if your plan will enable you to do the rest as a “mega backdoor Roth.”

When deciding between Roth and Traditional 401 (k) plans, it’s crucial to consider your future tax brackets. Roth 401(k) plans can be advantageous, especially in your highest income earning years, if you anticipate being in a lower tax bracket in the future.

2 Use a Backdoor Roth IRA

2 Use a Backdoor Roth IRA

Even if your income is too high to contribute directly to a Roth IRA, you still have options. The Mega-Backdoor Roth is an excellent strategy for high-income earners. You can max out your pre-tax 401(k) contributions and then contribute to an after-tax 401(k). IRS rules allow up to $66,000 in total contributions annually, though amounts beyond the $22,500 pre-tax limit are non-deductible.

To execute the Mega-Backdoor Roth (if your plan allows), contribute to the after-tax 401(k) and then roll those funds into a Roth IRA or Roth 401(k). This way, you can still benefit from the advantages of a Roth account.

3 Leverage Other Pre-tax Options

Depending on your healthcare plan, you may have access to a Health Savings Account (HSA) or a Flexible Spending Account (FSA). HSAs offer significant tax advantages:

HSAs:

- Reduce taxable income

- Can be invested and grow tax-free

- Can be used tax-free for future healthcare costs or long-term care insurance premiums

HSAs are the most tax-advantaged accounts available. For high-income earners, contributing to an HSA and allowing it to grow can be highly beneficial. Remember to keep receipts for potential pre-retirement withdrawals. In 2023, you can contribute up to $7,750 for a family.

If you don’t have an HSA, an FSA is still a valuable option as it lowers your taxable income. However, FSAs can’t be invested for future use and typically follow a “use it or lose it” rule within the year, with a small amount potentially allowed to roll over. You can contribute up to $3,050 in 2023.

Another pre-tax option is a Dependent Care FSA, which allows you to save money for qualified childcare expenses on a pre-tax basis. You can contribute up to $5,000 a year, making a significant impact.

4 Invest In Real Estate

Real estate is a highly tax-advantaged asset class, offering benefits through bonus depreciation, cost segregation studies, 1031 exchanges, and more. By leveraging these tools, investors can reap significant rewards.

If your spouse qualifies for Real Estate Professional Status (REPS) or utilizes the short-term rental loophole, you can offset other active income with real estate losses. While this sounds beneficial, it requires passing several stringent tests. Here are some resources to explore these tests further. It’s crucial to work with your tax professional when considering this route.

Another advantageous option is investing in Qualified Opportunity Zones, especially if you have substantial capital gains from equity compensation or other investments. By reinvesting the gains into an opportunity zone, you can defer taxes until 2026 and potentially enjoy tax-free growth if held for 10 years. However, ensure that any opportunity zone investment aligns with your overall investment strategy and is a sound choice.

5 Capital Gains

For high-income earners, a key tax strategy involves capitalizing on the preferential tax rates for long-term capital gains. Here’s how:

- Hold Investments for Over a Year: Ensure you buy and hold investments for at least one year. This qualifies your gains for long-term capital gains tax rates, which are significantly lower than short-term rates.

- Long-Term Compounding: Investments held for decades can compound tax-free, enhancing your overall returns. By minimizing taxable events, you can allow your investments to grow more efficiently.

Adopting a long-term investment strategy can maximize your after-tax returns and effectively build wealth over time.

6 Asset Allocation and Tax Loss Harvesting

Optimizing asset location involves strategically placing different types of investments in various accounts to minimize tax liability:

- Taxable Accounts: Allocate the most tax-advantaged assets here to minimize the impact of taxes.

- Tax-Free Accounts: To benefit from tax-free growth, place the highest appreciating assets in these accounts, such as Roth IRAs.

- Tax-Deferred Accounts: Assign the lowest appreciating assets to these accounts, like traditional IRAs or 401(k)s, to defer taxes until withdrawal.

Properly managing asset location can reduce the tax drag on taxable accounts, leading to significant tax savings over one’s lifetime.

Tax loss harvesting is a strategy where you sell investments at a loss to offset gains elsewhere, thus lowering your overall tax liability:

- Sell Losing Investments: Identify investments that have lost value and sell them.

- Move to Similar Assets: Reinvest the proceeds into a similar asset to maintain your portfolio’s strategy.

- Offset Gains: Use the realized losses to offset capital gains from other investments. You only pay taxes on your net capital gain for the year.

- Year-End Review: Towards the end of the year, review your capital gain tax liability and identify any losing investments you can sell to offset gains, potentially reducing your tax bill to zero. If you have no gains, up to $3,000 of losses can be used to offset ordinary income, with any remaining losses carried forward to future years.

By combining asset location and tax loss harvesting, you can effectively manage your portfolio to maximize tax efficiency and enhance long-term growth.

7 Charitable Contributions

If you have extra funds and are charitably inclined, there are several strategies to lower your taxable income through charitable contributions:

- Donor-Advised Funds and Charitable Remainder Trusts: These vehicles allow you to donate funds and receive an immediate tax deduction while distributing the funds to charities over time.

- Donating Appreciated Securities: Donate highly appreciated securities to avoid capital gains taxes and still receive a tax deduction. Donate the securities before selling them to avoid paying capital gains tax and still get the income deduction to maximize the benefit.

Bunching Charitable Donations

Consider bunching charitable donations every other year to maximize itemized deductions. Here’s how it works:

- Example: You earn $500,000 annually and plan to donate 5% of your income, which amounts to $25,000 annually. This amount is below the standard deduction threshold of $27,700 (for married couples filing jointly in 2023), so you would likely take the standard deduction.

- You might barely exceed the standard deduction threshold if you have additional deductions.

Instead, if you bunch donations:

- Year 1: Take the standard deduction of $27,700.

- Year 2: Donate $50,000 and take the itemized deduction for the full amount, totaling $50,000.

Total Deductions Comparison

- Without Bunching, your total deductions would be $55,400 ($27,700 each year) over two years.

- With Bunching: Your total deductions would be $77,700 ($27,700 in Year 1 and $50,000 in Year 2).

This strategic approach results in $22,300 more in deductions over two years. If you are in the 37% tax bracket plus state taxes, this could result in over $10,000 in tax savings.

This is an example of proactive tax planning, ensuring you maximize your deductions and minimize your taxable income by strategically timing your charitable contributions.

8. Manage Your Equity Compensation

High-income earners working at venture-funded startups or publicly traded corporations often receive equity compensation, including RSUs, ISOs, NSOs, or ESPP plans. Here’s a quick overview of each and how to manage your tax liability:

Restricted Stock Units (RSUs)

- Taxation on Vesting: RSUs are taxed as ordinary income when they vest.

- Holding Period: If you hold RSUs beyond the vesting date, any gains are taxed at short-term capital gains rates if held for less than a year, and at long-term capital gains rates if held for more than a year.

Non-Qualified Stock Options (NSOs)

- Taxation on Exercise: When you exercise NSOs, you are taxed on the difference between the exercise price and the market price at your income tax rate.

- Holding Period: Any additional gain is taxed at short-term capital gains rates if held for less than a year, and at long-term capital gains rates if held for more than a year.

Incentive Stock Options (ISOs)

- Taxation on Exercise: There is no immediate tax on exercise unless the alternative minimum tax (AMT) is triggered, which can result in an additional 26% or 28% tax. Most of this can come back as a credit in future years.

- Holding Period: Gains are taxed at short-term capital gains rates if held for less than a year, and at long-term capital gains rates if held for more than a year.

Employee Stock Purchase Plan (ESPP)

- Discount and Lookback: ESPP plans allow you to buy company shares at a discount, often 15%, with a lookback provision that calculates the purchase price using the lower fair market value of the stock at the beginning of the offering period or the purchase date.

- Taxation: You are taxed immediately on the gain from the lookback and discount. Further gains are taxed at short-term capital gains rates if held for less than a year, and long-term capital gains rates for more than a year. This plan is more complex and may need detailed planning.

Strategic Planning

- Resources and Planning: Each type of equity compensation requires specific strategies to minimize taxes. By understanding the tax implications and planning accordingly, you can manage your tax liability effectively.

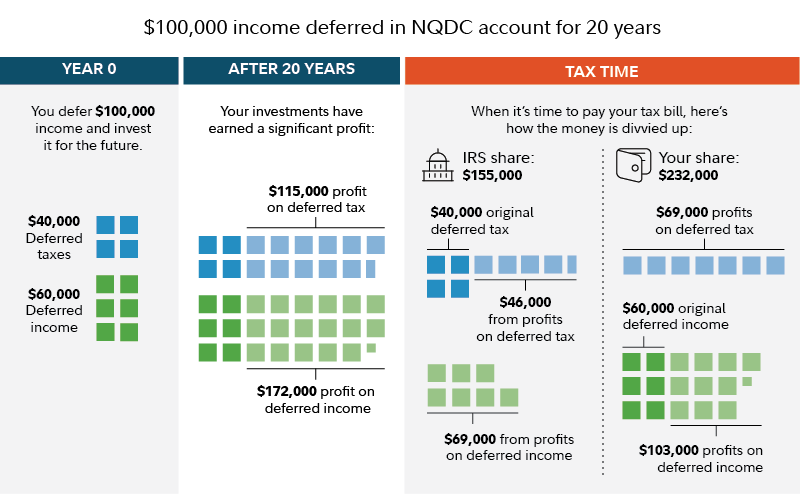

9 Non-Qualified Deferred Compensation Plan

If you’ve already maxed out your 401(k) and other tax-advantaged accounts like HSAs and IRAs but still want to save more for retirement or other financial goals, exploring a nonqualified deferred compensation (NQDC) plan could be beneficial. Most companies provide NQDC plans as an executive retirement benefit because 401(k) plans often are inadequate for high earners.

Benefits of an NQDC Plan

- Higher Deferral Limits: Unlike qualified plans, NQDC plans allow you to defer a significantly larger portion of your income.

- Tax Deferral: Taxes on deferred compensation are postponed until the deferral is paid out, allowing for tax-efficient growth.

How NQDC Plans Work

- Income Deferral: You defer part of your current income to be paid out at a future date, such as retirement.

- Separate from Regular Income: The deferred compensation is not included in your taxable income, potentially lowering your tax liability.

Ideal Situations for NQDC Plans

- High Income Earners: If you have a substantial income, deferring compensation can help manage your tax bracket and retirement savings.

- Strategic Planning: By deferring compensation, you can align your income with lower-tax years, such as during retirement.

NQDC plans can be a strategic move for high earners looking to optimize their tax planning and retirement savings beyond the limits of traditional retirement accounts.

10 Maximize Other Deductions

If you own a home with a mortgage, you can deduct the interest paid, as well as state and local property taxes. While these deductions might not drastically lower your tax bill, every bit helps in reducing your taxable income.

Additionally, if you itemize deductions, you can deduct medical expenses that exceed 7.5% of your adjusted gross income. This can be particularly valuable if you had significant medical expenses for yourself or a household member during the year.

Conclusion

Financial advisors have long tackled the question of how to reduce taxable income for high-income earners. Each year, tax rules evolve, and because everyone’s financial situation is unique, some of these tax reduction strategies may not be universally applicable. Earning a higher salary often results in paying more federal and state taxes due to graduated tax rates that increase with income. However, understanding the tax rules lets you optimize your strategy to retain more earnings. Regularly assessing your tax situation can ensure you don’t miss out on potential savings opportunities. A qualified CPA advisor can also help tailor tax strategies to minimize your tax burden. Feel free to reach out to Huckabee CPA with any questions or get a free consultation.