2020 Elections: How Biden’s Tax Plan could Impact income taxes on Businesses and Executives?

As far as election years go, 2020 is probably one that we will never forget. With the U.S. still in recovery from the Covid-19 pandemic caused recession, and restarting the economy will be a focus for whoever ends up winning in November. And the coronavirus is not only affecting how the candidates are conducting their campaigns, but also how voters will be getting to the polls. While tax policy is not the leading issue in the current election cycle, it will, nonetheless, be one of the likely tools used by November’s winner to address the existing economic crisis.

As far as election years go, 2020 is probably one that we will never forget. With the U.S. still in recovery from the Covid-19 pandemic caused recession, and restarting the economy will be a focus for whoever ends up winning in November. And the coronavirus is not only affecting how the candidates are conducting their campaigns, but also how voters will be getting to the polls. While tax policy is not the leading issue in the current election cycle, it will, nonetheless, be one of the likely tools used by November’s winner to address the existing economic crisis.

For business owners and executives it’s important to stay informed on possible election outcomes, and start planning now on how to mitigate the impact of potential tax law and policy changes from an income and investment portfolio perspective. Market Watch just reported “How wealthy Americans are already prepping their finances for a Joe Biden presidency” about a San Francisco CPA that just helped their client who was planning to stretch the sale of founder shares in a tech-sector company over a three-year period, but now compressed the installment sale into a one-shot transaction this month. They wanted to take advantage of a capital gains at a rate of 23.8% instead of a possible 39.6% rate under a Biden administration.

Elections and the Stock Market

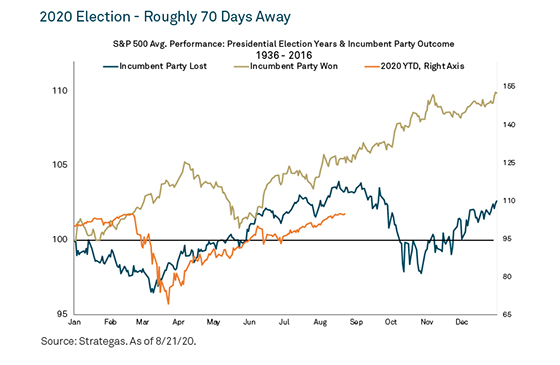

Now that I had already mentioned that is not a normal election with at being said, BNY Mellon Wealth recently published an article titled 2020 Election: Politics, Portfolios and Planning and they stated the U.S. stock market has been a fairly decent barometer of predicting who will win presidential races going back all the way to 1936. According to the article there is a general rule of thumb that the S&P 500 is positive in the three months leading up to the election, the incumbent party wins the White House. And usually if the opposite is true, a change in presidential party leadership is foreshadowed. Of course no one could have predicted a pandemic of this magnitude to hit 6 months before an election that would turn the economy upside down. Since we are fewer than 2 months away from the election, we can get an early indication of what equities may be signaling. BNY Mellon Wealth states that since August 3, the S&P 500 had been up approximately 3%, having delivered the fastest recovery from a bear market of 30% or more. Historically the stock market is positive in August and doesn’t make a decisive move until September. Therefore, it will be important to watch the direction of U.S. equities over the coming weeks. The chart below from BNY Mellon Wealth is from August 21st 2020.

POSSIBLE ELECTION OUTCOMES

POSSIBLE ELECTION OUTCOMES

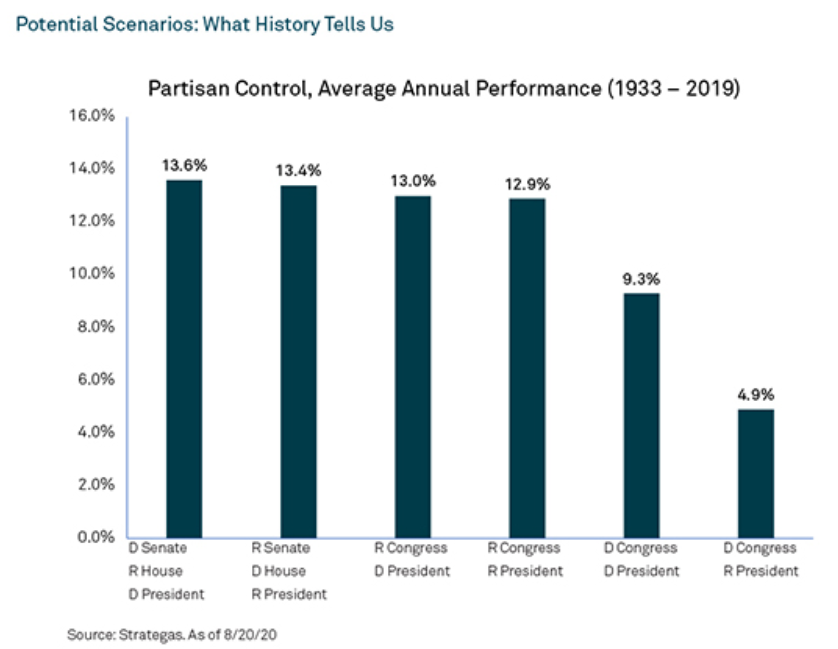

So while policy platforms can have an impact on the direction of the economy, what legislative bills get passed and signed into law is largely dependent on the makeup of congress. At the moment betting odds are that Democrats have a slightly better chance of flipping the Senate. And a “blue wave” where Joe Biden wins the presidency and the Democrats win the House and Senate could result in the most significant policy shift, with potentially more fiscal spending and sweeping tax changes. While this scenario raises a big concern for business leaders and investors, it is not an immediate cause for complete panic; with the economy being a huge priority to have recovered; new policies could take longer to get through or get watered down. And while the stock market may react negatively in the short term, they could fare alright over the long haul.

Now a divided government, with Biden beating Trump and the Republicans still hold a majority in the Senate, could possibly focus policy on infrastructure spending, more regulation and expanded health care coverage. Although Biden has proposed increasing taxes on the top income wage earners and large corporations, progress on this front could be limited or difficult under a divided congress. In this scenario, the stock markets reaction may be calm as it seems that markets are already starting to price in some chance of Biden winning against trump.

Now if President Trump wins a 2nd term, the country will likely see a continuation of pro-business growth policies, bilateral trade agreements including his “tough on China” policy and a continuation of current tax rates. This outcome could be modestly positive for the stock market.

And the BNY Mellon Wealth article says that usually the stock market tends to like a split government, as their chart illustrates below, a single party in power can also be positive for stocks. Basically, what often happens when one party controls the White House and Congress is that the party not in power gets voted back in during the midterm elections.

PLANNING FOR POTENTIAL TAX LAW CHANGES

PLANNING FOR POTENTIAL TAX LAW CHANGES

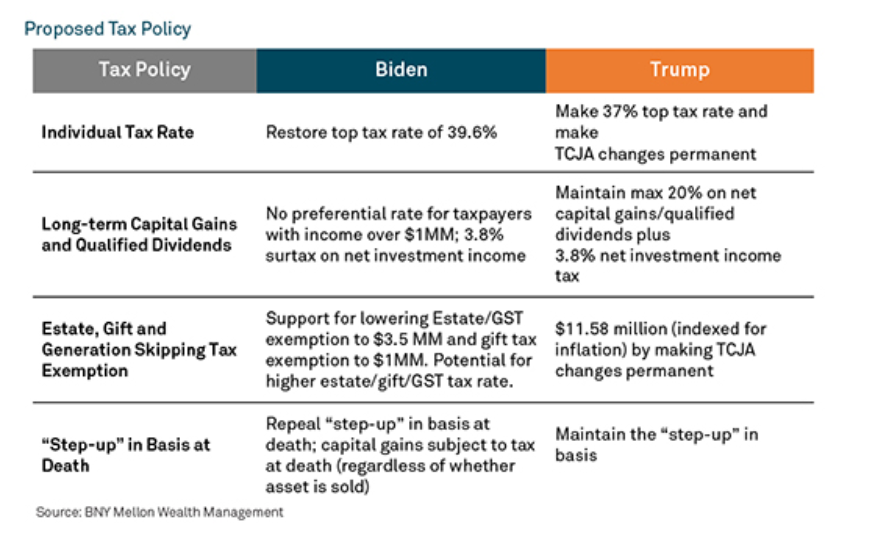

The president’s campaign has not released any detailed tax platform; instead, it has only offered broad ideas. And while President Trump’s focus would most likely be to make some of the changes of the Tax Cuts and Jobs Act of 2017 that are expiring at the end of 2025 permanent, Biden’s tax plan proposal is more progressive. Depending on the outcome of the election, these potential changes could have a significant impact on your income, retirement savings and wealth. According to recent reporting from the Wall Street Journal, Democratic presidential candidate Joe Biden wants to raise taxes by $4 trillion over a decade, concentrating those higher levies on top earners to pay for an agenda that includes fighting climate change and expanding child care, pushing federal revenue about 9% above what it would be without any policy changes in the next decade, according to a study of his tax proposals. The think tank Tax Policy Center analyzed his proposals and determined that under his plan, the highest-income households would see substantially larger tax increases than households in other income groups, both in dollar amounts and as a share of their incomes.

CORPORATIONS

A WSJ article reported that Mr. Biden’s proposed corporate tax increases make up a significant piece of his $4 trillion tax plan. Extremely profitable companies like Amazon Inc. could no longer use legal breaks to drive their U.S. tax bills almost to zero under Joe Biden’s proposal to increase and overhaul corporate taxes.

For corporate taxpayers, Presidential candidate Biden’s tax plan would raise the tax rate to a flat 28%, the mid-point between the 21% flat rate currently in effect and the 35% maximum pre-TCJA rate.,. On top of higher tax rates, to ensure that large profitable companies pay some level of tax, Mr. Biden would impose a 15% minimum tax on book income profits reported to investors for companies reporting $100 million or more, a move that would limit companies’ use of popular corporate tax breaks. That minimum tax would raise $400 billion over a decade by the campaign’s estimate, and $166 billion according to the Tax Policy Center. According to Michael Gwin, a Biden campaign spokesman, “the additional revenue would go toward infrastructure, clean energy and other priorities.” You may be wondering how is it that very profitable companies such as Amazon or GE (a while back) manage to pay little or no tax? The WSJ explains that “they often do so because of the discrepancies between two sets of books. One, reported to investors publicly, follows generally accepted accounting principles for recognizing income and expenses. The other, reported to the Internal Revenue Service privately, follows the tax code.” The rules don’t always match, so companies can report significant profits on their financial statements while paying little or no tax. For example, accounting standards require companies to spread capital investment costs over multiple years, but tax rules let them deduct costs sooner, lowering their tax bills now.

In addition, Biden proposes to double the tax rate applied to the global intangible low-taxed income (GILTI) of foreign subsidiaries of US firms, raising it from 10.5 to 21 percent, likely prompting affected companies to restructure their operations to mitigate its impact. Although it is not clear, the GILTI tax change may be implemented by reducing the GILTI deduction, which is currently 50%, to 25%.

Also, under consideration is a recent proposal for a 10% penalty surtax on profits from goods that are manufactured or produced abroad, but sold in the U.S. market. The new surtax results in a 30.8% corporate tax rate, which consists of the increased 28% corporate tax rate and the resulting penalty of 2.8%. To provide other incentives to U.S. companies making investments in domestic manufacturing and to help revitalize closed U.S. facilities, Biden proposes a 10% advanceable tax credit. The new Biden policies generally seek to roll back parts of the TCJA’s foreign taxation provisions to discourage overseas manufacturing if the same work can be done domestically by U.S. workers.

FURTHER CONSIDERATIONS

The CPA firm Berdon LLP published an interesting article about these potential tax policy changes if Biden were to win, and they gave some of their insights.

The corporate income tax rate reduction under the TCJA induced many pass-through businesses (S corporations, partnerships, and LLCs taxed as partnerships) to migrate to C corporation status, as the spread between the corporate tax rate of 21% and the TCJA top marginal individual tax rate of 37% (for pass-through businesses ineligible for the 20% deduction) became an eye opening 16%. The Biden plan would narrow that spread to 11.6% (39.6%-28%) when combined with the restoration of the top individual tax rate to 39.6% as under pre-TCJA law, which is still a meaningful difference.

Converting into a C corporation made sense for companies that were reinvesting after tax profits in pursuit of growth, as the second layer of tax that applies to dividends at the shareholder level would not be incurred. But for a C corporation that regularly distributes its earnings, the effective corporate/shareholder tax rate is currently 39.8% (21% + (1-.21)*23.8%). The Biden plan would increase that to 45.1% (28% + (1-.28)*23.8%), or 59.2% (28% + (1-.28)*43.4%) for high income taxpayers by making taxpayers with income over $1 million ineligible for the favorable tax rate on long-term capital gains and qualified dividends.

PASS-THROUGH BUSINESSES & SCHEDULE C FILERS

On the flip side, pass-through entity owners and schedule C filers currently pay a top federal income tax rate on business income of 37% or 29.6% to the extent the earnings qualify for the 20% pass-through deduction. The Biden plan increases the top individual tax rate to 39.6% and, for taxpayers with income over $400,000, repeals the pass-through deduction via a phase-out formula.

Currently, for business income, other than income from rental real estate which is expressly exempt, active pass-through owners and Schedule C filers pay a self-employment tax of 12.4% on business income up to $137,700 and Medicare tax of 2.9% (plus the .9% surcharge on income above $200,000) on all such income without any cap. When combined with the proposed repeal of the self-employment income cap on income in excess of $400,000, the top marginal overall federal tax rate for Schedule C filers and active pass-through business owners could be as high as 53.0% (39.6% top income tax rate + 2.9% Medicare tax rate + .9% additional Medicare tax + 12.4% self-employment tax, less the benefit of the 50% of self-employment tax deduction of 2.8%, or 15.3% * 92.35% * 50% * 39.6%). Businesses with employees earning wages in excess of $400,000 annually will shoulder 6.2% of the additional 12.4% social security tax assessed on these wages as well.

FURTHER CONSIDERATIONS

According to Berdon LLP. one strategy used for mitigating self-employment and Medicare taxes has been conducting business through an S corporation, because unlike partnerships and LLCs, S corporation pass-through income is exempt from these taxes. Although an S corporation is required to pay a reasonable salary to its owners that are involved in the business (which is subject to social security and Medicare tax), depending on the context, this often is interpreted as a minimum amount, particularly where significant capital and/or other labor is involved. Income in excess of that is exempt from these additional taxes. While S corporations are generally considered inferior to LLCs as an entity choice due to their comparative inflexibility (e.g., fixed income and loss allocations), under the right circumstances, it could be a wise choice.

Like S corporations, income of a limited partner in a limited partnership is not subject to self-employment tax on the partner’s share of partnership income irrespective of the level of participation in the business, provided that the income is not a guaranteed payment for services performed. If the limited partner is passive, then the pass-through income would be subject to the 3.8% additional tax on net investment income. However, under most modern state limited partnership statutes, a limited partner can be active in the business without shedding liability protection. Thus, in the right circumstances, the needle can be thread between self-employment and Medicare taxes and the net investment income tax by using a limited partnership. While limited partnerships are more flexible than S corporations, they are more cumbersome to form and maintain since to limit general partner liability for entity level liabilities, it is a standard practice to have a corporation or LLC act as the general partner. A limited partnership must have at least one general partner. There is no guarantee, however, that these legal loopholes would not be slammed shut in implementing legislation. Absent that happening, these strategies could be quite useful in the event such legislation is passed.

Pass-through entity owners with total income over $200,000 and that are passive with respect to the pass-through businesses will pay, in addition to regular income tax, the 3.8% net investment income tax on their share of pass-through income. Under current law, such taxpayers pay a maximum overall top federal tax rate of 40.8% (37% + 3.8%) on pass-through income, or 33.4% (37%*(1-.20) + 3.8%) to the extent eligible for the 20% pass-through deduction. Under the Biden plan, these situated taxpayers will pay a top marginal federal tax rate of 43.4% (39.6% + 3.8%).

The foregoing discussion has focused on business income, which is ordinary as distinguished from long-term capital gain. Currently, long-term capital gains tax rates for individual taxpayers range from 0 to 20%, depending on one’s overall income level—making the top marginal tax rate on this species of income 23.8% when combined with the net investment income tax. For taxpayers with income in excess of $1 million, the Biden plan would tax long-term capital gain as ordinary income subject to the top marginal tax rate, making the total top marginal federal tax rate 43.4% (39.6% + 3.8%). Gain from the sale of stock or LLC interests in private businesses, as well as the sale of business property, including real estate, often qualifies under current law as long-term capital gain if held for more than one year. Taxpayers with sales transactions pending or under consideration should try and expedite them for a 2020 closing to be sure this benefit is not lost. Also, strategies such as installment sales may prove useful in certain scenarios.

REAL ESTATE RELATED PROVISIONS

The real estate industry stands to lose some long-standing tax advantages under a Biden tax bill. By far the provision most dear to the industry is the beloved tax-free exchange under section 1031. The TCJA narrowed the availability of section 1031 to only real estate, where previously it was available for tangible personal property, including business airplanes and investment art. The Biden plan looks to eliminate real estate from this benefit, affecting its full repeal, although some have reported that this repeal would be limited to taxpayers with income over $400,000.

FURTHER CONSIDERATIONS

A fixture in the Internal Revenue Code since 1921, section 1031 has been a standard tax deferral strategy in real estate dispositions, supported by a cottage industry of knowledge-based service providers. It is a primary factor in the liquidity of the real estate market. The aggregate amount of deferred gain currently inherent in U.S. real estate assets from section 1031 transactions is likely a significant number. The Joint Committee on Taxation has estimated the tax cost to the Treasury from 2016-2020 at $90 billion. A 20% capital gains tax rate suggests that the deferred gain just for those years equates to some $450 billion. If coupled with the repeal of the step-up in basis at death, discussed below, and elimination of favorable capital gains rates, the current relative liquidity enjoyed by real estate is bound to be impacted, potentially affecting prices heavily.

Berdon LLP cites some other techniques, such as complex partnership mixing bowl transactions, would likely be popular as section 1031 surrogates. In addition, the cash-out nonrecourse refinancing, a standard real estate liquidity strategy for generations, and the tax law provisions supporting its tax-free status, do not appear to be at risk under a Biden tax plan. Already popular long-term ground and master lease transactions would become more so in a world without section 1031.

Other real estate related items that may be in a Biden tax plan include lengthening the recovery period for residential rental property, currently 27.5 years, to equal that of the 39 years applicable to commercial property and repealing the $25,000 special loss allowance for certain active rental real estate owners.

INDIVIDUALS

According to an analysis from the Tax Policy Center, it’s probably likely that Biden’s tax proposals allow all temporary tax provisions to expire as scheduled (e.g., the TCJA’s individual income tax changes will expire after 2025). These provisions are as of February 23, 2020. Biden tax plan policy increases are aimed at those making more than $400,000, and households at the very top of the income scale would see the biggest rises. Let’s take a look at key areas of Biden’s tax plan (illustrated below) and a few early action items you can consider from a planning perspective ahead of potential tax law changes.

While Biden has pledged no income tax increases for individuals earning less than $400,000, those who earn above that amount could see their marginal tax rate increase to 39.6%. Meanwhile, capital gains and dividends tax rates could shift from a maximum of 23.8% to a maximum of 43.4% for taxpayers with income above $1 million.

While Biden has pledged no income tax increases for individuals earning less than $400,000, those who earn above that amount could see their marginal tax rate increase to 39.6%. Meanwhile, capital gains and dividends tax rates could shift from a maximum of 23.8% to a maximum of 43.4% for taxpayers with income above $1 million.

If you have retirement and investment portfolios, the importance of tax-aware investing, which focuses on helping to maximize after-tax returns, only increases in a higher tax environment. The BNY Mellon Wealth article suggests if you are in the process of rebalancing portfolios or paring back concentrated positions, working in consultation with your wealth manager, it may be better to take those gains in 2020. Additional planning strategies focus on how to mitigate taxes in the future. You may want to convert a traditional IRA to a Roth IRA in order to pay taxes today and avoid paying higher taxes in the future. Or, you may want to transfer appreciated assets to family members in a lower tax bracket.

Estate and gift tax is another important area of focus as the proposed changes are significant. Currently, the federal estate/gift exclusion allows individuals to give away $11.58 million of assets ($23.16 for married couples) over their lifetime or at the time of death (with amounts greater subject to a 40% tax). This exemption level could potentially decrease to $3.5 million per individual (and a 45% tax for amounts above that level). In addition, Biden has proposed the elimination of the “step-up” in basis, which adjusts the cost basis of property transferred at death to its fair market value for your heirs.

The Wall Street Journal published a helpful article that analyzes 5 different American households at different income levels and how taxes would change.

- Repeal the TCJA’s individual income tax cuts for taxpayers with incomes above $400,000.

- We assume individual income tax rates revert to their pre-TCJA values for taxable incomes above $400,000,

- itemized deductions begin to phase out at taxable incomes over $400,000,

- the qualified business deduction begins to phase out at taxable incomes above $400,000, and the $400,000 income threshold does not vary by filing status and is indexed for inflation.

- Cap itemized deductions at 28 percent of value. We assume the proposal applies only to itemized deductions and does not apply to employer-provided health and retirement benefits.

- Tax capital gains and dividends at the same rate as ordinary income for taxpayers with over $1 million in income. We assume the proposal adds a fourth bracket for long-term capital gains and qualifying dividends (resulting in brackets of 0 percent, 15 percent, 20 percent, and 39.6 percent).

- Tax unrealized capital gains at death. We assume the proposal’s exemption and treatment of gifts and transfers to spouses and charity is the same as detailed by the US Department of the Treasury (2016, 155–57).

- Increase tax preferences for middle-income taxpayers’ contributions to 401(k) plans and individual retirement accounts. We assume

- the proposal replaces the deduction for worker contributions to traditional IRAs and defined-contribution pensions with a refundable tax credit as proposed by Gale, John, and Smith (2012), and

- a credit rate of 26 percent, which is roughly revenue neutral over the long run.

- Provide automatic enrollment in IRAs for workers who do not have a pension or 401(k)-type plan. Offer tax credits to small businesses to offset the costs of workplace retirement plans. We assume the proposal is the same as detailed by the US Department of the Treasury (2016, 134–38).

- Restore the full electric vehicle tax credit, target it to middle-income consumers, and prioritize the purchase of American-made vehicles. We assume the proposal makes the electric vehicle tax credit permanent, repeals the per manufacturer cap, and phases out the credit for taxpayers with income above $250,000.

- Create a $5,000 tax credit for family caregivers of people who have certain physical and cognitive needs. We assume the credit is the same as in the Credit for Caring Act of 2019 (except with a $5,000 maximum).

- Extend the earned income tax credit to workers age 65 and older without qualifying children.

Conclusion

If Trump wins a second term we don’t know for sure but probably could expect a continuation of the pro business growth policies as far as regulations and taxes. Now even if Biden wins unless the Democrats flip the Senate then you still need legislation to pass thru it to be able to overhaul the tax code. Depending on which party controls the Senate, Biden’s economic agenda may be either easier or significantly more difficult to carry out.

Republicans currently hold the upper chamber, and their continued majority next year could thwart much of Biden’s proposals before they get off the ground. Recently a Wall Street Democratic supporter Roger Altman said on CNBC’s Squawk on the Street show, that “An increase in the capital gains rate would always lead to sales of equity securities prior to the effective date of the increase. That would happen every time,” he also added “But the long-term effects are really not historically negative, and those long-term effects depend on … broad macroeconomic factors. Not just the capital gains rate.”

Businesses, irrespective of size or entity type, should evaluate how their current and future operations and cash flow might be affected not only by Biden’s proposed tax changes, but also the likelihood of tax increases in a second term for President Trump. Taking time to assess potential tax law changes now will allow businesses to identify areas of risk and opportunity and better plan for the future. Contact Huckabee CPA for a free consultation.

{kind=link}