5 red flags that your Small Business Accounting Books aren’t Ready for Tax Time According to Quickbooks Online

Startup entrepreneurs and small business owners have a million tasks to deal with at the beginning of the new year in 2021. One of the best ways to ensure that your tax season goes smoothly is proper planning and preparation. It is recommended that you or CPA take a hard look at your back office books to double check and make sure that everything is being accounted for in an organized fashion. Bookkeeping is the process of recording all financial transactions made by a business. Bookkeeping services are responsible for recording, classifying, and organizing every financial transaction that is made through the course of business operations. Having clean, and accurate financials make it so much easier for your accounting firm to file your business taxes, maximize your deductions to lower your tax liabilities that you will owe to Uncle Sam. Having a clean set of books is vital in strategically & successfully running your business, however the process is intimidating, stressful & time consuming.

Startup entrepreneurs and small business owners have a million tasks to deal with at the beginning of the new year in 2021. One of the best ways to ensure that your tax season goes smoothly is proper planning and preparation. It is recommended that you or CPA take a hard look at your back office books to double check and make sure that everything is being accounted for in an organized fashion. Bookkeeping is the process of recording all financial transactions made by a business. Bookkeeping services are responsible for recording, classifying, and organizing every financial transaction that is made through the course of business operations. Having clean, and accurate financials make it so much easier for your accounting firm to file your business taxes, maximize your deductions to lower your tax liabilities that you will owe to Uncle Sam. Having a clean set of books is vital in strategically & successfully running your business, however the process is intimidating, stressful & time consuming.

Are there signals or red flags to look out for to know if your books are up to date and ready for tax season? Did you know that 25% of businesses are behind in their financial accounting books? No need to ignore it anymore. Quickbooks Online, published an article recently that interviewed 5 accounting experts that gave some of their input into telltale signs of bookkeeping errors and pitfalls to look out for.

1 Your books show negative numbers

Sometimes you can see negative numbers,Alisa McCabe, President of First Steps Financial, stated that “for example, when you accept a payment from a client but there is no invoice to apply the payment, this creates a negative number when you run the A/R report. This should be corrected as quickly as possible to provide accurate reporting and to have your tax prep done quickly and efficiently.” And if a negative shows up in the liabilities or assets section of the balance sheet, most of the time this is a sign that something has been recorded incorrectly or needs to be reclassified. There can be anomaly or one off instances, but this is usually of a sign that there is an accounting error that should be looked into further.

2 Your transactions are not categorized

![]()

If you still have transactions in your bank downloads, or you have items in ‘uncategorized income or expense,’ you need to review and place them in the proper categories. Once this is done, you will have a better idea of your financial picture. Lisa Brann of CPA CGMA, PLLC explains that “there should be no balances in the unclassified assets, unclassified liabilities, unclassified income, unclassified expenses, or ‘ask my accountant’ accounts. These accounts are holding accounts. If there is a balance in any of these accounts, they need to be researched and reclassified to a real account.” One accounting error to look out for is making the mistake of categorizing expenses as “other” or “miscellaneous.” The reason being is that other and miscellaneous account transactions must be identified eventually on a filed tax return. And for tz preparer’s this can be a little unclear or confusing.

Another fundamental accounting setup principle to check on is, making certain that your chart of accounts is set up and categorized correctly. Donna Sooter Lim, CEO of Sooter Consulting, stated that “a common mistake is to have credit card payments listed as an expense” If you carry a balance on a credit card, it is possible you took the expense at the time of the purchase. The payment is not an expense.

One final tip is to make sure your fixed assets are clearly marked for your tax preparer. Ms Lim said “the tax preparer will need to know what the asset is. It’s not enough to put the transaction in the fixed asset accounts.”

3 You haven’t had a tax planning session with your tax planning professional

It is always (especially for this unusual past year with the Coronavirus, shutdowns, remote working, and Cares Act legislation, PPP loans that were passed) recommended that small business owners consult and work with a CPA firm or tax professional to make sure your books are ready for tax season. They can also help to provide insights on your particular financial and tax situation and help you plan for tax season. In the article Alisa McCabe stated that “your books are not tax ready until you have had a tax planning session with your tax professional. Tax professionals are there to help limit your tax liability and use current tax laws to your advantage.” This also a perfect time to ask your CPA about any questions you might have on items in the “ask my accountant feature” or now called uncategorized (that takes on many forms; assets, income, expenses).

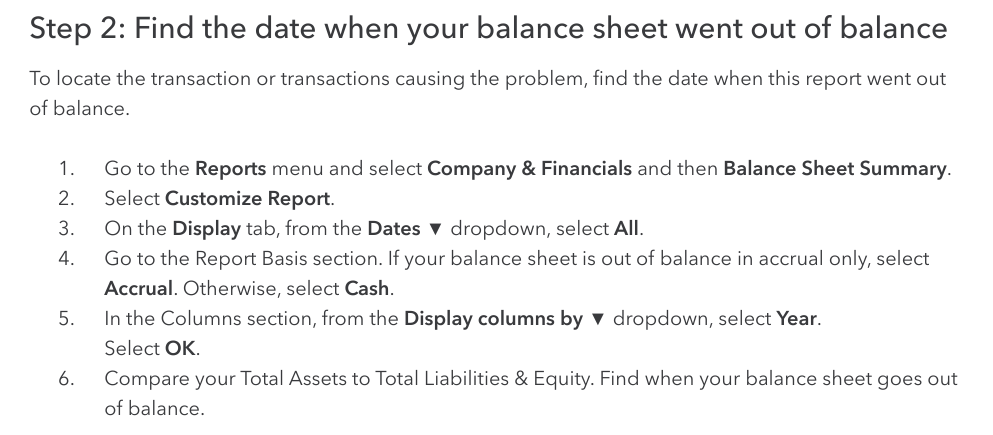

4 Your balance sheet doesn’t balance

Your total assets should match your total liabilities on your Balance Sheet. Balance sheet reports can be tricky. It’s a good idea to ask your bookkeeper or accountant for help before you continue. If you don’t have one, we can help you contact us.

Lisa Brann of CPA CGMA, PLLC, stated that “If the balance sheet does not balance, there is an issue that needs to be fixed, the equity section accounts may need to be closed out, an inventory item may be incorrectly using the wrong accounts, or the file may need to be verified and rebuilt. The balance sheet must always balance.”

Also the prior year balance sheet must tie to the balance sheet reported on the tax return. Ms Brann explains that when she first takes on a new accounting client, The first thing she checks is if the prior year retained earnings ties to the tax return. Which usually means there have been no entries added or deleted in the prior years, which is a good sign the books match the prior year returns, and no adjustment is necessary. It is always a good idea to double check that your loan balances agree with the year-end loan statements on the balance sheet. Make sure that interest, late fees, and principal should be separated into appropriate accounts.

5 Your accounts aren’t reconciled

All accounts should be reconciled through January to make sure all transactions that happened in December of the tax year are recorded properly. Alisa McCabe stated “this will ensure that income and expenses in your books are up to date. Reconciling enables you to see if there are any discrepancies and provides documentation from a third party that backs up your data, if an audit happens.”

Now even if you have bank feeds already setup, you don’t might think that you don’t have to reconcile the bank account, but it’s a good idea to double check it. Lisa Brann stated “if there were no outstanding items that may be the case, but most clients have outstanding items. Outstanding checks and outstanding deposits that are past the normal length of time outstanding should be investigated.”

As an example any uncleared checks should be reviewed to see if perhaps they were cleared but not matched or need to be reissued. The automated bank feeds are great and have become reliable, but it’s not foolproof. You need to make sure all income and expenses are counted. We also don’t know if something was deleted unless we reconcile. It’s better to be safe than sorry.

A few other items worth noting

- Checks are missing vendor names- not a tax ready issue but it is important for sending out 1099s in the correct amount. Each check should have the vendor identified, the amount, and correct categorization. There should also be a W-9 on file for vendors.

- Having transaction types other than accounts receivable in your income accounts- you can Sort your report by transaction type, if you see expenses, bills, checks, etc., these should be investigated for erroneous categorization.

- Your P&L does not match the tax and wage summary – run a payroll report for the year, and reconcile wages, employer taxes, and officer wages (if applicable).

- Your payroll has not been reconciled – make sure payroll is recorded correctly and reconciled to the 941. What’s in your books needs to match what’s been reported to the IRS.

- You haven’t completed a year-end inventory count- it’s important to have a year-end inventory number to shore up the books. Let your tax professional about any obsolete inventory that needs to be disposed of.” While this process can be time consuming, it can also impact your tax return

Conclusion

Get ready for tax season. If this sounds overwhelming, you’re not alone. Analyzing your books, categorizing transactions, and reconciling accounts can be tricky. Don’t worry if you need help and want someone to review them Huckabee CPA is a Quickbooks Online Certified Pro. Feel to contact us with any questions you may have or for a free consultation.

{kind=link}