De-Dollarization efforts are happening: what would happen if the dollar loses its global reserve currency status?

The U.S. dollar is the most powerful currency that exists today. Yet financial analysts have been warning of the dollar’s impending doom since its rise to prominence in 1971. One of the more intriguing financial trends of 2023 has been the de-dollarization movement. This is an effort by a growing number of countries to reduce the role of the U.S. dollar in international trade. Over the past few months, Russia and China have been quite vocal about trying to develop a new currency with the BRICS nations: Brazil, Russia, India, China, and South Africa.

Last month in April, the Financial Times reported that Brazil’s president Luiz Inácio Lula da Silva has called on developing countries to work towards replacing the US dollar with their own currencies in international trade, lending his voice to Beijing’s efforts to end the greenback’s dominance of global commerce. He stated “Why can’t we do trade based on our own currencies?” he added, drawing loud applause from the audience of Brazilian and Chinese dignitaries. “Who was it that decided that the dollar was the currency after the disappearance of the gold standard?”

- Amid the de-dollarization debate, the “BRICs” countries are lining up to try and replace the reserve currencies for trade and payments.

- Sanctions against Russia sound a cautionary tale over the power Washington — and the USD — wields.

- The Chinese yuan, gold, Bitcoin, the euro, and a common BRICS currency aim to chip away at USD supremacy.

- For the first time in 48 years, Saudi Arabia said that the oil-rich nation is open to trading in currencies besides the U.S. dollar.

- Many nations are looking for alternatives to the dollar to reduce their dependence on the US

Foreignpolicy.com published an article on this topic that stated that these developments complicate the narrative that the dollar’s reign is stable because it is the one-eyed money in a land of blind individual competitors like the euro, yen, and yuan. As one economist put it, “Europe is a museum, Japan is a nursing home, and China is a jail.” He’s not wrong. But a BRICS-issued currency would be different. It’d be like a new union of up-and-coming discontents who, on the scale of GDP, now collectively outweigh not only the reigning hegemon, the United States, but the entire G-7 weight class put together.

Here’s what US investors need to know as foreign countries talk about abandoning the dollar ?

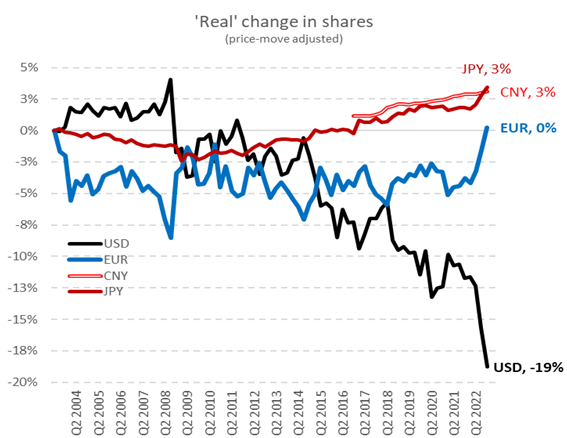

An article in US News posed the question: With so much of the world economy reshaping itself in the post-pandemic landscape, is the reserve status of the U.S. dollar going to be the next domino to fall? According to a recent article in Bloomberg, The greenback’s share in global reserves slid last year at 10 times the average speed of the past two decades as a number of countries looked for alternatives after Russia’s invasion of Ukraine triggered sanctions.

Currently, the Dollar represents 58% of reserves, down from 73% in 2001 when it was the “indisputable hegemonic reserve.” Stephen Jen, Eurizon SLJ Capital Ltd. Mr Jen told Bloomberg “The dollar suffered a stunning collapse in 2022 in its market share as a reserve currency, presumably due to its muscular use of sanctions.” He further wrote “exceptional actions taken by the US and its allies against Russia have startled large reserve-holding countries,” most of which are emerging economies from the so-called Global South.”

(image credit:Bloomberg)

(image credit:Bloomberg)

Geopolitics isn’t the only hot-button issue, however. Inflation is also weakening the standing of the dollar on the international stage. Since the 1980s, the United States has maintained a low and steady inflation rate, giving savers around the world the confidence to hold their assets in dollars. Over the past year, however, inflation has soared to previously unimaginable levels, calling into question the security and stability of the dollar for long-term savings and investments.

Russia and China’s Steps Towards De-Dollarization

Concerned about America’s dominance over the global financial system and the country’s ability to ‘weaponize’ it, other nations have been testing alternatives to reduce the dollar’s hegemony.

As the United States and other Western nations imposed economic sanctions against Russia in response to its invasion of Ukraine, Moscow and the Chinese government have been teaming up to reduce reliance on the dollar and to establish cooperation between their financial systems.

Since the invasion in 2022, the ruble-yuan trade has increased eightyfold. Russia and Iran are also working together to launch a cryptocurrency backed by gold, according to Russian news agency Vedmosti.

In addition, central banks (especially Russia’s and China’s) have bought gold at the fastest pace since 1967 as countries move to diversify their reserves away from the dollar.

History of the Reserve Currency

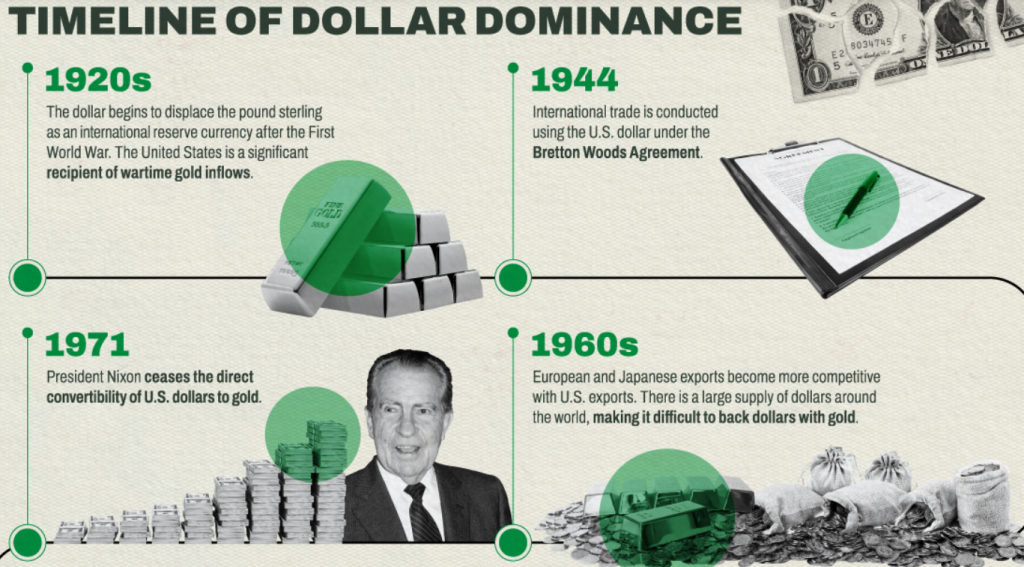

The US News article gives a pretty history lesson on this subject, stating that for centuries, the world has had what’s known as a reserve currency. This is the currency in which the majority of the world’s international transactions are handled. Historically, these were the currencies of a series of European colonial powers, including Spain, France and England at various points. These empires often backed their currencies with precious metals, typically gold, in addition to the implicit backing of the state.

Following World War I, the British economy struggled to regain its vigor. Much of the world’s gold flowed from London to New York for safekeeping and speculation in the roaring 1920s U.S. equity bull market. America’s dominant role in World War II further cemented New York as the financial capital of the world, and the dollar as its most important currency. The greenback was formally made the world’s reserve currency in 1944 as a result of the Bretton Woods Agreement, a status the sterling had previously held.

Fast forward to 1971. When President Richard Nixon got rid of the gold standard. From that point on, the dollar has been backed not by precious metal, but purely by the full faith and credit of the U.S. government along with its military force. And since 1971, numerous people have called for the end of the U.S. dollar as the world’s reserve currency. Will the 2020s be the tipping point when these calls turn to action?

What Would Happen if the Dollar Loses Reserve Status?

It’s important to realize that reserve status is something that, historically, has been gained or lost over a long time horizon. It’s unlikely that the world would wake up one day with dollars no longer holding international appeal. Rather, in examples such as the British pound, there was a multidecade process by which it went from the center of world economics to a second-tier currency.

That said, if the dollar gradually loses its place atop the world financial pyramid, what would happen next? For the U.S., it would likely mean less access to capital, higher borrowing costs and lower stock market values, among other effects. Having the world’s reserve currency has allowed the U.S. to run large deficits in terms of both international trade and government spending. If foreigners no longer want to hold dollars for savings, it would force significant belt-tightening at home.

As for what would replace the dollar, it’s hard to forecast at this point. It’s possible to imagine a world in which the euro or Chinese yuan eventually became the primary reserve currency, but a great deal would have to change in world politics to get to that point. Some economists also propose a financial system backed by either precious metals or cryptocurrency, though implementation of these sorts of models could prove to be a considerable challenge.

Why the Dollar Is Still King ?

There are a couple of factors that have led to the dollar maintaining its international reserve currency status. One is the so-called “petrodollar.” The vast majority of the world’s oil transactions occur in dollars. As the global oil trade amounts to billions of dollars per day and all countries need energy, this creates a great deal of demand for dollars to facilitate these transactions.

While oil is the most obvious example, there’s a broader need for a world unit of exchange. Consider a scenario where a Brazilian farmer sells soybeans to a Japanese condiments company. It’s highly unlikely that the Japanese firm would have Brazilian real on hand to pay the farmer. Similarly, the Brazilian grower is not going to want to accept Japanese yen in exchange for their soybeans. Thus, the logical solution is to use an intermediary to convert yen into dollars, buy the soybeans with dollars, and then have the producer convert those dollars into their local currency.

Stephen Jen told Bloomberg, the dollar’s role as an international currency won’t be challenged anytime soon as developing countries don’t yet have the ability to divest from the greenback for transactions due to its large, liquid and well-functioning financial markets. His final note of caution to investors “the prevailing view of ‘nothing-to-see-here’ on the US dollar as a reserve currency seems too innocuous and complacent,” he wrote. What needs to be appreciated by investors is that, while the Global South is unable to totally avoid using the dollar, much of it has already become unwilling to do so. Not everyone is so scared about the BRICs trying to kill the dollar, a Bloomberg Opinion writer Tyler Cowen wrote a lengthy piece on the subject:

The US has the world’s deepest and most liquid financial markets, and they remain relatively open, in spite of some restrictions on Chinese investment in industries sensitive for national security. There are strong reasons to have a dominant currency in international markets, just as there are strong reasons for having a dominant currency in domestic transactions within the US. Liquidity for a currency begets further liquidity, whether at home or globally.

With the dollar estimated at 88% of all international transactions, the euro at 31% is only a modest competitor (since a transaction may involve two currencies, the total may exceed 100%). The euro, unlike the dollar, will never be tied to a single national government, and the European Union does not come close to the military might of the US.

The yuan is estimated at only 7% of that total of international transactions, and China seems unwilling to open up its capital markets, as that could lead to rapid capital outflows and possibly a financial crisis. But without open capital markets, the yuan is not a strong contender for a global reserve currency.

Conclusion

By one estimate, the dollar is a part of 88% of all international transactions. Some people fear this dominance cannot last, while others question whether it should: Doesn’t a stronger dollar hurt US exports, and thus US workers?

The good news, for Americans at least, is that dollar hegemony is beneficial for the US, its government and most of its citizens. Furthermore, it is likely to last for the foreseeable future. Although if this past year’s involvement in the Ukraine war and the checkered track record of economic sanctions on Russia is any indication, sanctions will become an increasingly ineffective tool of U.S. security policy.

{kind=link}