Do traditional indicators of economic prosperity mean average Americans are doing well? Not necessarily.

In 1929, we had the Great Depression. In 2001, we had the DotCom bubble. In 2008, we had the Housing crash. In 2023, we now have “the Silent Depression” according to some.

While the United States is not battling the 25% unemployment levels seen in the 1930s, many Americans feel financially strained, working harder and more hours just to keep on their monthly bills. Recently a Forbes contributor Jack Kelly reported that On TikTok, some are calling this the “Silent Depression,” citing similarities to the Great Depression era. Abdullah Al-Bahrani, an economist at Northern Kentucky University (NKU) also wrote about this topic and examines the claims of the recent trend on social media that has a group of creators referring to our current economy as the Silent Depression.

The videos usually make two main claims:

- Our incomes are lower today than they were during the Great Depression

- Housing and other essentials are more expensive today compared to the 1930s

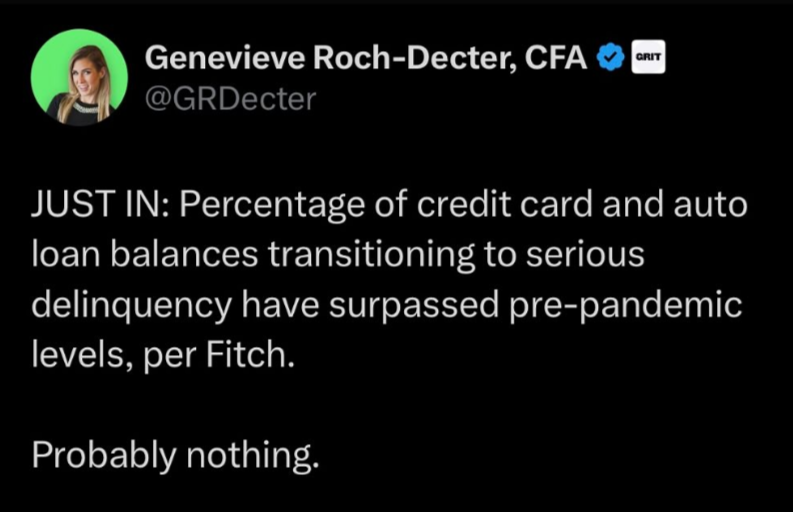

With over $1 trillion in credit card debt, tapped 401(k)s, and soaring mortgage rates locking out homebuyers, households are struggling. Still, the current standard of living, while pressured, remains far ahead of the deprivation during the historic Depression. While today’s challenges are real, invoking Depression-era comparison risks minimizing the acute hardship faced by prior generations.

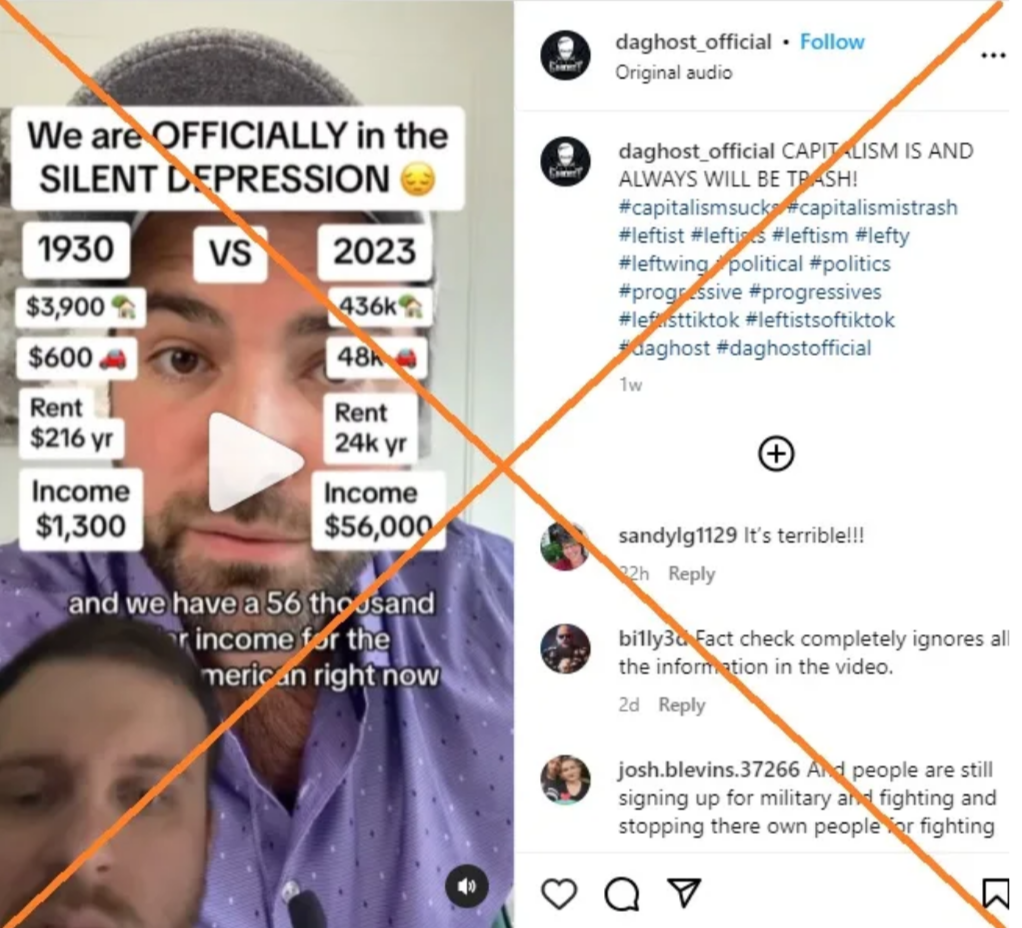

An article in The Troubador Online states that “In 1930, the average annual income of a single American was a little over $4,800, based on the United States Internal Revenue report for that year. Accounting for inflation over the years, that number reaches to just less than $85,000 a year today.” The article goes on to explain that “unfortunately for us, the current average income for a single American is only $56,000 according to the U.S. Bureau of Labor Statistics, meaning that as of 2023, Americans are making less than they were at the height of the Great Depression.” A Yahoo New article contradicts this claim saying the IRS report only reflects data from 3.7 million tax filers in 1930 — a small fraction of that year’s population of 123 million. That is because only the top income tiers were required to file returns at the time. In contrast, some 150 million tax returns were filed in 2022 out of a population of 330 million.

Beyond income, prices for gas, cars, and homes show similar disparities versus inflation-adjusted 1930s levels. While these statistics paint a concerning economic picture, directly equating them to the devastating Great Depression overlooks key differences in poverty rates, unemployment aid, social services, and overall living standards. The current economy warrants serious policy action but has not approached a Depression-level downturn.

According to a recent X, formerly Twitter thread from Brennan Schlagbaum, a CPA at Budgetdog, says “the biggest issue right now in the economy is… Surprisingly still strong. However, things are not okay. Inflation, rent prices, and an increase in social pressure has priced almost everyone out of this market.”

He also lists out some concerning stats about housing affordability;

- 18 Million millennials have moved in with parents this year

- Mortgage demand is at a 27-year low

- Minimum-wage workers cannot afford the average rent in the US

- Institutional investors may control 40% of U.S. single-family rental homes by 2030, according to CNBC

According to another Forbes article about housing predictions “despite ultra-high mortgage rates and home prices, the market remains as competitive as ever, thanks to demand levels surpassing the ongoing inventory crunch and homeowners who locked in low interest rates staying put. These and other factors perpetuate the perfect affordability crisis storm that continues to sideline many aspiring homeowners.”

Mr. Schlagbaum doesn’t believe prices will go down for homes or basic needs. They’re overpriced… But the demand for everything is still there and will stay there.

The Economic Issues

Even though in August, the recent jobs data by the Bureau of Labor Statistics, reported a 0.3% wage growth, it was still notenough to combat the impact of high inflation and the increased costs of living. Because the costs of housing, education, and healthcare are continuing to go up, leaves some households with less discretionary money. That also doesn’t help the mental health crisis that can cause more stress and anxiety of constantly trying to keep up financially.

The Forbes article points out that there has been a significant downward shift in the job market, particularly for white-collar professionals. Competition is fierce, the hiring process seems to take longer, jobs are being relocated to lower-cost cities and countries and workers’ salaries are being cut by employers by 47%.

Unlike past generations, today’s young adults encounter restricted social mobility and difficulty securing financial footing, often carrying substantial personal debt from credit cards, loans, and expenses like medical bills. These burdens can make saving and investing for the future nearly impossible.

The Forbes author’s perspective is that even though previous generations faced difficulties climbing the social mobility ladder, supports like unemployment insurance, food assistance programs, disability benefits, and broader economic opportunity help prevent the extreme deprivation that plagued Depression-era youth. The current landscape poses real challenges but remains far removed from the hopelessness and scarcity of the 1930s.

Many corporations would rather hire gig, contract and temp workers to cut costs and not have to pay full salaried worker benefits. Professionals in temporary roles face precarity, anxiously eyeing contract expiration and the next gig search. Graduates weighed down by debt may be underemployed in jobs below their credentials. Diminishing purchasing power consumes meager savings. If this isn’t enough, the quick ascendancy and deployment of artificial intelligence ominously threaten workforce replacement for some roles in the future.

Is it Really That Bad for The Middle Class?

Mr. Kelly, mentions that the TikTokers ranting about their perceived Silent Depression have legitimate concerns, such as the inability to realize the American Dream, as they can’t afford to start a family or purchase a home. But to compare this to the great depression of the 1930s isn’t really the same. The Great Depression was an extreme and extended period of economic turmoil, with numerous devastating consequences for the country. Key events included the stock market crash of 1929, large numbers of people losing their jobs and homes, rampant bank failures, unemployment surging to 25%, and a harmful deflationary spiral.

Compared to today, of which the current unemployment rate is 3.8%. Stocks are near highs, and the U.S. has thus far been able to avoid recession. The misery index is far lower than the high-inflationary period of the 1970s, let alone the Great Depression.

None of this takes away from the struggles that some families are facing financially and real fears of falling out of the middle class or losing their jobs. Some economists speak about the struggles of the “shrinking middle class” or the notion of a two-tiered “K-shaped recovery.” The term coined by Peter Atwater, a lecturer at William & Mary, a university in Virginia, is back in vogue as the wildly uneven recovery in the U.S. economy since Covid-19 with millions of lower-paid workers struggling, while many other Americans have grown wealthier thanks to surging stock and house prices. According to CNBC, As is often cited, the share of adults who live in middle-class households is shrinking. Now, 50% of the population falls in this group as of 2021, down from 61% 50 years earlier, according to Pew.

Their share of the country’s wealth is also getting smaller, while the top 1% continue to amass more and more, several other studies show.

They worry rising inequality isn’t fully captured by statistics, like GDP. A large segment of workers, especially Gen-Z, face depressed opportunities compared to prior generations despite headline growth.

Mr. Schlagbaum lays out a few strategies to get more financially disciplined:

1 – If you make under $250k

It’s time to budget. Even if you are “good” it’s time to be “great” with money. The sooner you get ahead… The sooner you can give the middle finger to inflation.

2 – Seek Professional Guidance

A lot of people have silent spending problems. That’s where the pressure is really coming from. You know it if you have it. It truly doesn’t matter how much you make if you have spending problems… You’ll never get ahead.

3 – Learn From Others

We’ve all heard the stories of ‘08 and the people who got wiped out. Imagine if you could give them advice… That’s what you need to do RIGHT NOW. The opportunity of a lifetime is on the horizon if you get ahead now.

It’s safe to say… Inflation and lifestyle inflation have caught up to society. Over the next 2 years:

- Some will go bankrupt

- Some will fall further behind

- Others will get ahead

Your choices now impact where you’ll be at 10 years from now.

Conclusion

Nonetheless, economists say there are elements of stress in today’s economy, including income inequality and housing affordability.