So do you work for or own a family business in San Diego or California? Large and small-sized family-owned businesses are the backbone of the U.S. economy. They make up a majority of U.S. gross domestic product (GDP) and generate 60% of the countries employment workforce, and, according to data from Score, create 78% of all new jobs.

So do you work for or own a family business in San Diego or California? Large and small-sized family-owned businesses are the backbone of the U.S. economy. They make up a majority of U.S. gross domestic product (GDP) and generate 60% of the countries employment workforce, and, according to data from Score, create 78% of all new jobs.

Family-owned businesses range in size:

- 1.2 million of family-owned small businesses are run by a husband and wife.

- They can range from 2 people to thousands in a Fortune 500 company.

Some family businesses become huge publicly traded companies and PWC says “a family business is defined as one in which (1) the majority of votes are held by the person who established or acquired the company (or by their spouses, parents, child, or child’s direct heirs) and (2) at least one representative of the family is involved in the management or administration of the business.” Think of Walmart or Dick’s Sporting Goods.

According to data from a Baker Tilly white paper, “over a typical family business history – through founding activity, mergers and acquisitions – the average middle-market family enterprise controls 6.1 businesses.”

And while some statistics show that almost half of all family businesses are owned by “Baby Boomers” who have plans of retiring in the near future, some data shows that:

- around 75% of the owners have no written transition plan

- over 80% have no documented growth plan

Baker Tilly points out that many family-owned business owners may have up to 50-90% of their personal wealth tied up in their business. According to a 2017 Forbes article titled “Study Shows Why Many Business Owners Can’t Sell When They Want To” found that only about 20 percent to 30 percent of businesses that go to market end up getting sold.

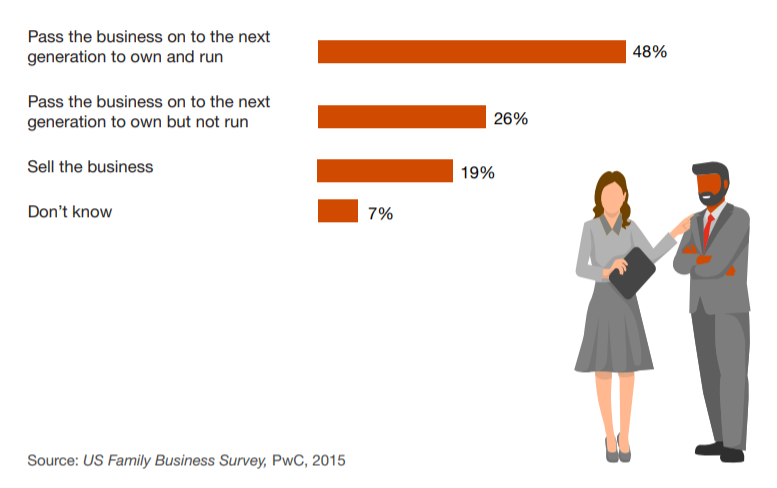

US family business snapshot from PWC

- 18% of US family businesses say they anticipate an ownership change within approximately 5 years.

- What sort of changes do they anticipate?

Many times the issue comes down to the fact that owners do not receive the valuation they feel they deserve, or potential buyers perceive there is too much risk. Today’s global economic and political climate makes it more important than ever for family businesses to implement effective planning strategies aimed at reducing risk and growing value.

Many times the issue comes down to the fact that owners do not receive the valuation they feel they deserve, or potential buyers perceive there is too much risk. Today’s global economic and political climate makes it more important than ever for family businesses to implement effective planning strategies aimed at reducing risk and growing value.

If a sale of the business is contemplated, owners must take into account the financial strength of the business, the financial position of potential buyers, available sources of financing, collateral, guarantees, the tax consequences for both parties and cash-flow issues. The timing of a transfer is also critical. A business owner who is considering selling the business may want to time the completion of the sale for maximum tax advantage. Doing so could result in net after-tax proceeds that are substantially higher than if the deal were accelerated or delayed. To manage such issues, owners should engage advisors who can help them make effective and timely decisions, as well as give them a detailed understanding of the sales process.

![]() RECOMMENDATION

RECOMMENDATION

If you are looking to get your business purchased or acquired by another company, you have to understand that a buyer is willing to a premium for a business based on their perception of risk and return. And if the characteristics a buyer values – which are usually those that both reduce risk as well as improve returns – are there, then a buyer will pay top dollar for the brand. These characteristics can be thought of as value drivers. According to an article in The Street by Ellen Chang, “a company’s goodwill or brand value represents its brand reputation, loyalty, along with patents or proprietary technology and adds significant value.”

All family businesses will, at some point, go through some kind of transition. That could be a leadership succession or ownership transfer. It’s important for family-owned enterprises should start to make themselves ‘transition-ready’ to achieve the family’s larger goals – meaning they need to be equally prepared for a leadership succession as well as an ownership transition and redeployment of that wealth. Warning though, a lack of a formal business succession plan can lead to a number of problems when the current owner ceases to maintain control. For instance, subsequent generations may be reluctant, unprepared, or unable to assume their predecessor’s level of responsibility. Then again, the owner might identify a willing successor but find that family members and other key stakeholders do not support the decision. The business owner could also discover that keeping things in the family simply isn’t practical (e.g., there isn’t enough liquidity to support a family buyout from the generation that currently owns the business). Although such issues can be difficult to confront—and therefore tempting to put off—it is better to deal with them sooner rather than later, when options may be more limited.

Baker Tilly’s formula for helping to guide family-owned businesses through transition has led them to discover a few important principles that are useful to understand during a transition journey.

- Transition does mean retirement

- Start with readiness

- Set your goals before the journey

- Price is not first

- Plan early, start earlier

- Equality is not equal

- Ask before you get lost

Business continuity, grasping transition readiness and thorough planning are key components of success “for families that are in business”. These guiding principles represent families that transition not only wealth but also the skills to grow and enhance that wealth across generations.

1 Transition is about Legacy

Think of family business transition as business evolution. It is about growth, opportunity and building the future from where you currently are today. It means that the current generation must take responsibility for future continuity of the family enterprise by making sure that the next generation of leaders are capable, competent, experienced and possess the skills to take the business to the next level. You can think of transition as the legacy you leave in away. Shareholder retreats and family gatherings can be forums for instilling the values of the business in younger generations and non-participating shareholders. A positive legacy can also be cultivated through the manner in which the company interacts with customers, employees and the community—establishing a well-known company philosophy. Once established, the family will be in a better position to choose the succession strategy or strategies that will get them closer to this vision for both the family and the business. Questions that families should consider include:

- Who are the key stakeholders in the family and the business?

- What is the family’s vision, not just for the near term but for the next 50 or 100 years?

- How does the family define its legacy?

- What is the long-term strategy for the business?

- How does each stakeholder define the success of the business?

Succession plans should be informed by the family’s longer-term vision and strategy. This will help determine what skills are needed and the type of leaders the company will need to get there.

2 Start With Readiness

Before you begin any kind of tough or serious journey, good preparation is a must. And the journey of transitioning a business is no different. Current and next-generation family members must work together to prepare for the transition process as it can be time, commitment and hunger. One way to get a sense of where you are at, is to get an assessment to test both ‘transition readiness’ and “strategic sustainability”. Baker Tilly suggests these assessments can uncover high priority areas to focus on and potential barriers to surpass when achieving a successful transition. Since no transition journey will be exactly alike, similar to how each family business will have unique dynamics – an assessment can help to provide a roadmap to follow, in addition, a timetable and resources.

By taking a look at the following family business dimensions, Baker Tilly says it creates a roadmap assessment plan‘s to help entrepreneurs reach individual, family and business goals:

- Strategic growth and value creation

- Exit strategies and ownership transition

- Leadership succession

- Next-generation

- Estate planning and wealth management

- Family business governance

- Business continuity

- Family communication and conflict management

The strategic roadmap, based on your results and your objectives, capabilities and readiness, could include any combination of the following focus areas: family enterprise strategy, portfolio business strategy and individual plans.

(Image credit: Baker Tilly)

3 Set Your Goals Before The Journey

It is almost impossible to overstress the importance of setting goals before beginning a family-owned transition journey. One way to do this is by creating a family business strategic plan. This type of plan can define a collective vision of the family for future generations to come, as well as outcomes, goals for the entire transition process. It will only work if the goals are both clear and measurable, and most importantly must be enticing enough to inspire and motivate the next generation in the transition process.

Goals within the strategic family plan can:

- Provide the motivation required

- Act as a lighthouse to guide the transition’s direction

- Gain agreement on the intent and expectations of all participants

- Develop a clear path for the transition process

- Serve as a benchmark for measuring the transition’s success

4 Price is not First

Sometimes family business owners mistakenly think the goal of a family business transition is to achieve the best or highest sale price. This is not the case. Instead, the transition process should aim to achieve three main results:

- Business continuity

- Value enhancement

- Risk reduction

No matter what the intent is – whether it is to sell, retain or transfer the business – these goals should not waver.

At its core, a transition is usually about anchoring and growing the value of the business. This can be achieved by delivering certainty, de-risking the business and identifying the right value drivers. Ask yourself the following couple of questions to figure out value-drivers:

- Do we own them?

- Can they be transferred?

- Are they durable?

- Do they deliver greater customer value and therefore competitiveness?

Whether or not the family decides to ultimately sell or retain the business, you can grow enterprise value by thoughtfully defining value drivers and their associated levers while also uncovering and removing risk factors.

(Image credit: Baker Tilly)

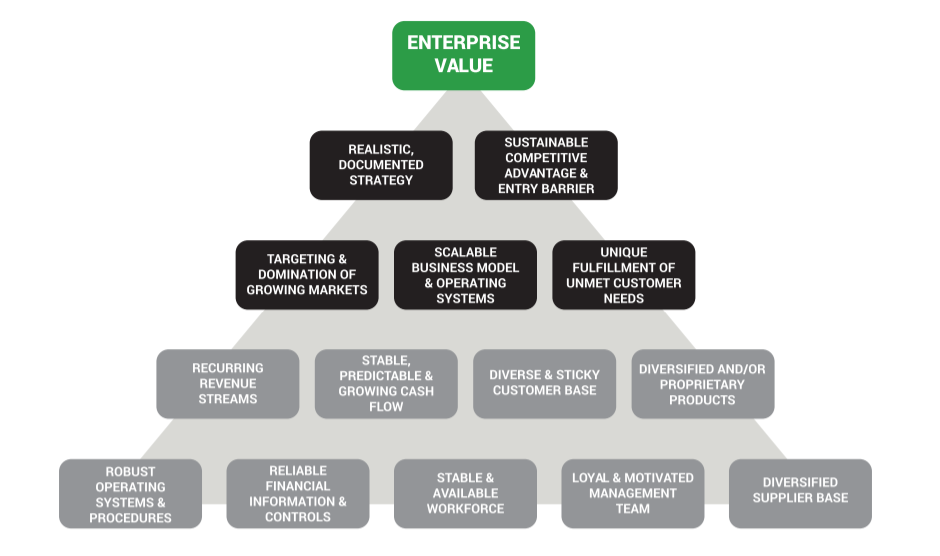

From the buyer or acquirer point of view, risk reduction value drivers improve the likelihood of a successful acquisition by eliminating major risk factors that could erode value post-acquisition. Here are the 9 most import risk-reducing factors according to Baker Tilly.

1 recurring revenue streams – contractually recurring revenue reduces risk and increases return for the buyer in a merger and acquisition purchase transaction. It also produces predictable forecastable cash flows and reduces the surprising factor post-close. Examples may include annual contracts for maintenance, subscriptions, licensing and other annuitized fees.

2 Stable, predictable and increasing cash flow – buyers may pay for cash flow that goes up or increases over time. Usually, buyers purchase companies that are growing and have a proven track record of growth in EBITDA and revenue.

3 Diverse and sticky loyal customer base – red flags can go up with potential buyers when a given customer accounts for more than 10 percent of sales or revenue. Buyers like to see many loyal customers with high switching costs, think of Oracle.

4 Diversified and or proprietary products or services – the market rewards innovation and punishes commodity-type businesses. Proprietary and or diversified products create barriers or moats to entry and also reduce competitive market risks.

5 Robust operating systems and procedures – the business must be able to operate after the seller or founder leaves. Operating systems and processes must be documented, in place and functioning properly.

6 Reliable financial information and controls – a lack of financial integrity is the most common issue or hurdle in the sales process. When a company is analyzing and conducting due diligence about what the think a company is worth. Investors and buyers require financial statements that are audited/reviewed by a reputable CPA firm.

7 Stable and available workforce – a high quality, and stable workforce increases value and reduces risk. Also having access to available high-quality talent in the market place will support future growth.

8 Loyal and motivated management team – The acquiring company cannot be dependent upon the founder or family business owner. Buyers want a competent high-quality team that will stay on and transition after the sale. And continue to operate it after the owner leaves or sells it.

9 Diversified supplier base – being too dependent on key suppliers can create risks related to capacity, quality, financial viability, catastrophe, global trends, and market disruption.

5 Plan early, start earlier

Keeping in mind that transition is about maintaining business continuity and enhancing enterprise value, it’s never too early to start planning for the transition. The outcomes you are wanting to attain truly begin the moment you think about launching a business and continuing throughout the entire business lifecycle. Setting up goals prior to starting your transition journey will enable you to develop a detailed strategic plan that both enhances value and achieves desired business continuity.

An important consideration to think about during the transition planning process is to find out the financial needs of all the stakeholders: the business(es), the generation that may be exiting and the generation that may be entering it. In order to lead a successful transition, the business must find a way to address these combined financial needs and manage the expectations of all parties involved.

The process for developing the financial capacity for the business in a way that covers the changing needs across generations takes time – and it must be understood, planned for and acted on well in advance of needs materializing.

6 Equality is not equal

A major issue for any family-owned business owner is to find the perfect balance of participation, ownership and distribution of wealth throughout the transition process. For example, some family members are, have been or might one day be involved in the business and others won’t … then this challenge needs to be addressed to gain business continuity and overall harmony.

Making decisions about how wealth might get allocated in the future – while simultaneously finding a way to attain family harmony over financial decisions can be challenging. Baker Tilly mentions that a strong guiding principle for dealing with these kinds of situations is “equality does not mean equal”, in other words, family business owners must be fair based on both the historical contributions that family members have made, as well as any future contributions family members will be expected to make.

This will require the current generation to:

- Involve all family members that the decision may impact from early on

- Clearly convey the family values and principles upon which the decision will be made

- Determine and talk about the impact that the decisions may have on individual family members

- It’s important to have open dialogue and everyone in the loop

- Engage with a spouse/ partner in these discussions

- Make a decision that is fair and explain the reasoning behind that decision-making

7 Ask before You Get lost

Family-owned business transitions can be a complex process – one that most often requires professional advice from an independent advisor with relevant experience. Do your research and look for advisors in different areas of specialized practice to speak with. Seek advice early on and continue to retain that support throughout the process. Openly talk about your intentions, thoughts, wishes, concerns, and questions with them. Before creating a plan to guide your transition journey, you must first assess the family’s readiness for that transition. Work with an advisor who thinks strategically understands the importance of business continuity and who can help focus on certain aspects of the business or family and personal goals and outcomes you desire.

Conclusion

A successful transition almost always hinges on a well constructed, written plan that clearly specifies the disposition of ownership interests in the business. The earlier the owner develops the plan, the better. That’s because the more time there is to prepare for succession, the greater the opportunity to maximize the business’s value and reduce the risks involved when an owner or key employee exits the business. A written plan should answer multiple questions, including these:

- Who should receive the ownership interests?

- When should the ownership interests be transferred?

- Should restrictions be placed on the transferred interests?

- How should the transferee be permitted to deal with the ownership interests?

- Should ownership and control (i.e., voting rights) be separated?

- Will the planned transfer cause conflicts that should be anticipated and addressed?

- What are the tax consequences of the planned transfer?

This article does not cover all the complex aspects that would go into thinking about:

- leadership succession planning

- Creating a board structure and board succession planning

- Ownership succession and choosing an entity business structure

- Tax considerations: when determining the right ownership structure

- Business ownership agreements (buy-sell agreement)

- Equity financing arrangement

- Initial public offering (IPO)

- lifetime transfer planning

PriceWaterhouseCoopers (PWC) wrote a comprehensive whitepaper on the subject titled “2019 Business continuity and succession planning for a family business guide”.

Thomas Huckabee CPA offers an integrated suite of advisory services from estate, trust and gift planning to income tax planning to strategic planning, we can help you grow your business to sell or increase the value of your business to pass on for generations to come. Contact us for a free consultation today.