Small Business Budgeting Template – How to Limit Business Spending and Pay Yourself More Income

Setting up a business budget template is a smart financial planning tool you can use to run your small business more profitably and efficiently. However, many small-business owners skip this vital business management step. Therefore, your budget planning workflows should be easy to access and adjust on an ongoing basis. Fortunately, you don’t have to spend a lot of money on fancy budgeting software. There are several free small-business budget templates available online.

Why do you need a business budget template

According to a recent article published in NerdWallet, a business budget template is an essential tool for business owners who want to take care of their bottom line. Why should you invest in a smart template from the start?

Here’s how a business budget template can set you up for success:

-

Track cash flow, expenses, and revenue.

-

Prepare for regular business slowdowns.

-

Allocate your budget to the portions of your business that need capital most.

-

Plan for business investments and purchases.

-

Project all costs to starting and running your business

Recently I came across an interesting article published by Gusto payroll, written by a small business owner named Paco De Leon, where she discussed a budgeting strategy she used to increase her company’s profitability by 132 percent, (she says). Let’s break down her weekly budgeting strategy exercises and see how it could help other small business owners and solopreneurs to manage their finances better. She said that her business was not profitable and in 2017 she opened up a new checking account for her business and she called it an “Income Account’.

So What is an Income Account?

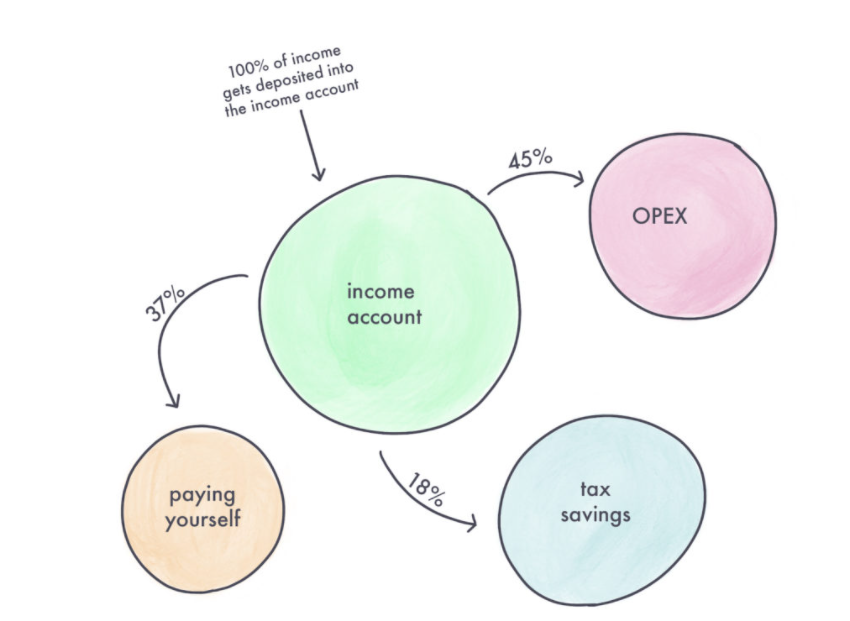

So according to Paco De Leon, “an income account is a checking account that acts as a clearing account—a place where money gets deposited and then transferred out to other accounts. It only has one job: To be the checking account where all the income you earn gets deposited.

Each week, she reviews all of her deposits and transfers funds from her income clearing account to her other accounts accordingly.

![]()

(Image credit: Gusto)

She states in her article that also setup 3 other accounts, where then she disperses or transfers the income to:

- An operating expense checking account

- A tax savings account

- A personal checking account

Let us dive a little deeper into what these other accounts mean.

1 Operating Expense Account, or OPEX Acct

Operating expenses, or OPEX for short, are the costs involved in running the day-to-day operations of a company; they typically make up the majority of a company’s expenses. Operating expenses are typically divided into several categories such as payroll-related expenses, administrative or overhead expenses, and sales and marketing expenses. She explained how she changed her old business checking account into an operating account. Of which she uses to pay all of her company’s business expenses from this account except for her personal salary.

Some of the expenses the lists that she pays each month from this Operating acct include:

- Independent contractors

- Apps and software programs

- Business meals

- Liability insurance

- Business travel

- Business loan payments

- My cell phone

- Business books

2 Tax Savings Account

Next she set up a tax savings account, where she transfers money to save for payroll and income taxes. “It’s important to have a tax savings account so come tax time when your accountant tells you what the damage is, you’ll have enough cash saved to pay the bill.” stated Paco De Leon.

You can also choose to make quarterly tax payments, which you’ll be saving more of that money as you earn it.

3. Personal checking account

This may seem fairly obvious, that the last account she uses to transfer money and pay herself is a personal checking account to pay herself a salary.

She also mentions that before she had made the income account, she would just look at the cash in her business account at the end of the month and pay herself based on what she had left and what she could afford. This method was not very good for budgeting.

Using this income account budgeting method helped her build a routine and commit to paying herself a percentage of income, not just whatever is left over.

This big change helped her shift money away from operating expenses and into her personal savings.

Weekly Financial Cash Flow Management Tasks

She also explained in her article that she logs into her bank accounts and monitors her cash flow and balances. She uses a Google spreadsheet to help her keep track of how much money she will need to transfer. “I recommend keeping a spreadsheet too. It’s good to have for reference and can be faster to look at than logging into your bank or bookkeeping software. “ – stated Paco De Leon.

(image credit: Gusto)

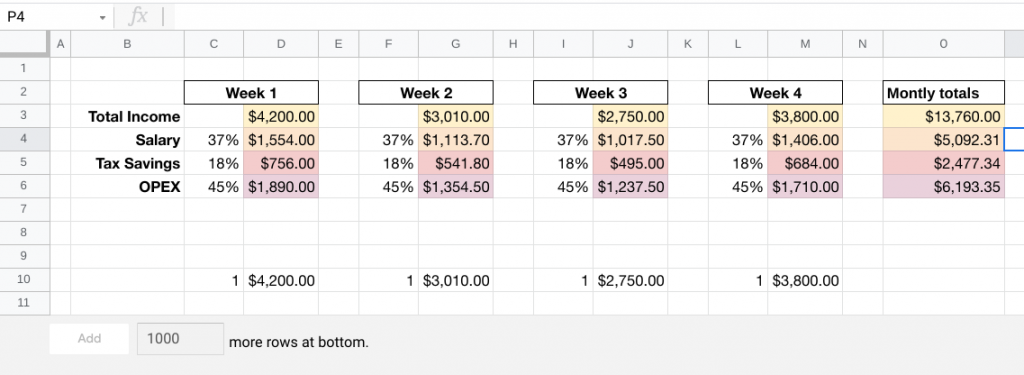

This is how she chooses to distribute her business income, by transferring:

- 18% of my income into her tax savings account

- 45% into the operating checking account, and

- 37% of her income into her personal checking account to pay herself

In her article, she mentions that she consulted a CPA about what her tax savings rate should be. She then brainstormed and made a financial projection of an income goal that was based on what she wanted to pay herself.

- She broke down how much she’d need to earn every day to reach that goal.

- She analyzed her revenue streams. An analyzed how much each stream was bringing in and what it would take to increase them to reach her financial goals.

- From that, she realized she would need to focus her efforts on growing the scalable part of her business and kill the parts that weren’t scaling.

It helped her figure out that she could make 45% work to meet the business needs and 37% for her personal income, leaving 18% for tax savings.

(image credit: Gusto)

She does this exercise on weekly basis not monthly

She does it weekly as a personal preference to build financial discipline. She stated “When I first started using the method, I needed to move money into my operating account to keep, you know, operating. After a while, it just became a habit and I started to enjoy the weekly finance time.”

What made this budgeting tweak work for her small business?

She limited her business spending. When she made the switch to paying herself first as opposed to just taking whatever was left over each month, she figured out that she was limiting the amount of money she put into her operating account. It did a couple of things:

- This meant that she couldn’t rationalize excess spending as things that she could “write off anyways” because the cash simply wasn’t there to spend.

- It also gave her a new perspective or lens to view the business through. It also provided a sort of checks and balances against sudden or frivolous impulse spending.

Amount you will spend = Amount of cash you can access

She came up with a theory she calls “pacos Law” which states that your spending will equal the amount of cash you have available to spend. By limiting your available cash, you can reduce your expenses.

By doing these budget forecasting exercises, and implementing this budgeting method also made her aware of what areas she was coming up short and how that impacted both her business and her personal economics. She then decided to reverse engineer the amount of income she needed to earn if she knew how much she wanted to pay herself and how much my business needed to operate. All of the parts of the equation impact one another. (It’ll be clear once you start to play with the equation.)

She listed a few monthly income equation scenarios she used.

If I wanted to pay myself $3,000/month and I knew my business needed about $3,500/month, I first have to figure out how much the whole pie has to be in order for 37% of it to equal $3,000.

- $3,000/.37 is $8,108.11

- Rounding up to $8,110, let’s see what 45% of that is and if it’s enough to cover the business’ monthly expenses.

- $8,110 x .45 = $3,649.50

Sweet, it is, since $3,649 is more than $3,500.

Now onto another example

Let’s say you need $6,000 for your business and $4,000 for your salary. We’ll start by manipulating the OPEX percentage to 50% instead of 45%. Then, we’ll see where the rest lands.

(If it doesn’t work, then you can manipulate another lever, like total income, or allocations.)

- $6,000/.5 is $12,000

- We’ll assume 18% for taxes or $2,160

- That leaves 32% or $3,840 for salary

She explains that with the second example, you’re short on salary, but you meet the business needs. She suggest that other small business owners should play around with the formulas, by plugging their own income numbers in.

Finally she mentions some examples of how you can change the allocation amounts to see how it changes the rest of the equation.

With $13,000 revenue, we’re right in the ballpark with these distributions:

- 49% going to OPEX is $6,370,

- 33% going to salary is $4,290,

- and 18% going to taxes is $2,340.

And with $12,500 revenue, the original distribution looks like:

- 50% going to OPEX is $6,250,

- 32% going to salary is $4,000,

- and 18% going to taxes is $2,250.

So based on the allocations above, monthly revenue should be between $12,500 – $13,000 in order to pay out a monthly salary of $4,000 and meet the monthly operating expenses of $6,000.

These exercises gave her financial clarity about what her business needed generate in revenue

She explained that “after doing these calculations, I knew exactly what I needed to earn. That meant I couldn’t pretend to be blissfully ignorant anymore. And by revisiting it every week, I could check in to see if I was on target, falling short, or coming out ahead of my goals.”

And as a small business owner, confronting the reality of managing your books and finances will ultimately be a good thing instead of procrastinating.

She said that her behavior changed because increasing income was now at the front of her mind, not the back of it.

It sounds tough, but when you analyze your business through numbers, (like an accountant, financial analyst or investor would)it becomes too clear to ignore.

Conclusion

When your business is not generating enough income to live the lifestyle that you want, then you need to diagnose the issue. The issue can be one thing or a variety of things.

- It could be that your business spends too much money.

- It could be that your pricing is too high for the market you’re serving or too low for the market you want to serve.

- Or it could be that the problem you think you’re solving isn’t really a solution that people would pay for.

Her final takeaway was that by using an income account, it will help you view your business through a new lens. You’ll be forced to be hyper-critical about how you spend and earn income. And if you need to make changes, having the details sooner rather than later will help you save time, energy, and lots of money. I like this article because it was useful and gave actionable steps and tips that other small business owners could use. Feel free to reach out to Huckabee CPA if you have any questions or would like a free consultation.