Should I form an LLC company for My California Real Estate Investments? Advantages and Disadvantages

For the past 30 years, LLCs ( limited liability companies) have been quite popular and the preferred business entity selection type for investing in and holding real estate. The real estate investors and owners often prefer to form an LLC when purchasing real estate—or when transferring titles—so that the LLC becomes the legal owner of record, rather than the individual members. According to an article published by Diane Kennedy, a CPA with US Tax Aid, Prior to that, real estate investors used limited partnerships (LP), with one or more general partners and one or more limited partners. The general partner wouldn’t have asset protection, so that spot was usually filled by an S Corporation. That meant the LP needed at least two entities. It was more expensive and complicated to run.

According to Mrs. Kennedy, “once proven in court, the asset protection from LLCs seemed to be the perfect answer. But then a few things started happening.”

Let’s examine the pros and cons of LLCs for real estate investments and what some other alternative structures could be.

Background: how does the LLC work?

An LLC (limited liability company) is set up at the state level. The asset protection, cost, and state annual filing requirements vary from state to state. Make sure you check on your own circumstances and don’t assume that what works in one state will be the same in your state.

There are a few reasons why people use LLCs:

- For asset and personal liability protection

- Favorable tax advantages

- Professional Appearance

- Simple Transfers

LLCs are a simple and inexpensive way to protect your personal assets and save money on taxes.

In most states, an LLC has “charging order protection”. That means that if the LLC has been set up and run properly, it can offer special protection that protects the business from personal debts or judgments of individual owners and it protects the owners from business debts or judgments. A Legal Zoom article also mentions that another reason to place a property title in the name of an LLC is that it gives you liability protection against monetary judgments if a financial dispute involving the LLC arises.

If a third party succeeds in obtaining a monetary judgment, it—the judgment creditor—can’t force the sale of real estate held by an LLC—the judgment debtor. Instead, the judgment creditor is typically required to obtain a “charging order” from the court that, in turn, becomes a lien on the real estate. While this is by no means cause for celebration, it’s better than losing the property altogether. Watch out for single-member LLCs, Mrs. Kennedy mentions not all states have the same level of protection. The worst state of all for LLCs is Florida. There is NO protection for single-member LLCs. And in most cases, they will not allow a married couple to have multi-member LLCs. They consider those single-member LLCs as well. If you form a business structure that you own or control, it counts as you too. So it’s difficult to get around the single-member LLC issue for Florida. A true multi-member LLC will work in Florida, in fact, charging order protection for multi-member LLCs is written into their state revised statutes.

When a business owner has limited liability protection, they can’t be held personally responsible if the business suffers a loss. This means personal assets (car, house, and bank account) are protected.

In order to have limited liability protection, the LLC must maintain its corporate veil. Other business structure types, like sole proprietorships and partnerships, don’t offer limited liability protection. Corporations offer limited liability but are difficult to maintain and often offer unfavorable taxation for a small business.

LLCs and Pass-Thru Taxation Treatment

There is no such thing as an LLC tax return. Though LLCs are a legal structure, they aren’t recognized by the Internal Revenue Service for tax purposes. You’ll need to tell the IRS how your business should be levied. To do that, you’ll file a Form 8832 with the “tax man” to indicate how you’d like to be levied: as a corporation, a partnership or as part of your personal tax return.

There is no such thing as an LLC tax return. Though LLCs are a legal structure, they aren’t recognized by the Internal Revenue Service for tax purposes. You’ll need to tell the IRS how your business should be levied. To do that, you’ll file a Form 8832 with the “tax man” to indicate how you’d like to be levied: as a corporation, a partnership or as part of your personal tax return.

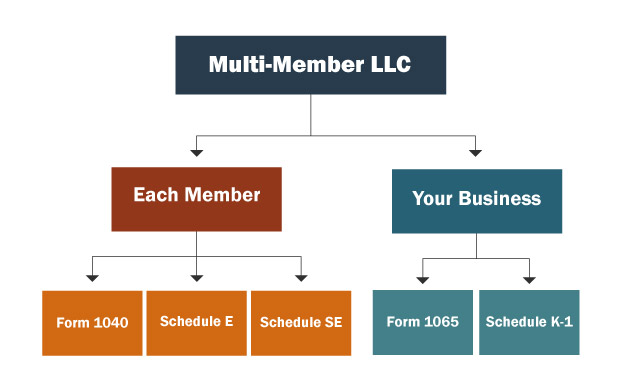

LLCs can elect how to be taxed. So they can be an S Corp or C Corp, or simply use the default tax status. Without the election, a single-member LLC will file either as a Schedule C (Sole Proprietorship) or Schedule E (for rental properties). Without the election, a multi-member LLC will file as a partnership. Members of LLCs who own real estate as part of their investment portfolio also derive favorable tax treatment from the Internal Revenue Service.

Whether you are the sole owner of the LLC (single-member LLC) or one of several members (multimember LLC), you benefit from so-called pass-through taxation.

For federal income tax purposes, pass-through taxation refers to the fact that any income earned by the LLC—including profits generated through real estate (such as rental income from leasing an LLC-owned property)—will pass through the LLC to its individual members.

Any income earned by the LLC is not taxed at the corporate level (as would be the case with a traditional corporation) but only at the individual level. Each LLC member reports the income on their individual federal income tax returns—usually on Schedule C. These pass-through rules help members of an LLC avoid double taxation.

Professional Appearance

An intangible benefit of owning and holding real estate in the name of an LLC is that it appears to the public to be more professional, especially when advertising a property for lease to commercial or residential tenants.

An individual or business looking to lease property may be more comfortable renting a piece of real estate from “Smith Properties LLC” than from “Joe Smith.”

Simple Transfers

An LLC can be sold through a relatively simple transfer of membership interests. The LLC’s real estate will continue to be owned by the LLC but with new LLC members. Continuity is preserved, and the transfer is seamless.

The Cons or Drawbacks of an LLC for Real Estate Investments

Before you jump into an LLC, there are a few challenges you may run into when you use an LLC for your real estate investments. Check these things out first!

Are you in a state that has good asset protection for LLCs? You will need to use an LLC in the state in which you have property. What are the costs, annual filing requirements and most importantly, what asset protection will you get?

The ‘Due on Sale’ Clause

Be careful about transferring any real estate that is held in an individual’s name to an LLC. If an individual initially secured financing and qualified for a mortgage for the real estate, the individual’s name will appear on the mortgage documents as the legal owner of record.

Both the Legal Zoom and US Tax Aid articles bring up this point. How will you handle the due-on-sale clause with a mortgage? This has been a concern for a number of investors when they move a property they purchased with a mortgage into an LLC. Call your mortgage company and ask for the legal department. Ask the lawyer for permission to move your property into an LLC for estate planning purposes. (This seems to be the magic phrase that makes the legal department happy.) You will undoubtedly get permission. Make a note of who you talked to and when send a confirmation email for the conversation and save it for your files.

In the event of a transfer of real estate from an individual owner to an LLC—which is treated as a sale of property—the owner of the LLC must make certain that the name in the property insurance documents matches the grantee on the deed. The mortgage lender will often learn of the transfer when the property insurance bill comes due (if insurance is escrowed) and may claim that the transfer violates the terms of the mortgage’s “due on sale” clause.

The due on sale clause is a standard provision in a mortgage that requires that the borrower (that is, the named property owner) pay the mortgage balance in full at the time of a sale. You may want to seek a waiver from the mortgage lender before transferring real estate from an individual’s name into the LLC.

Transfer Tax Obligations

LLCs may also raise transfer tax issues, depending on the state. In Delaware, for instance, no transfer taxes apply if an individual transfers ownership to an LLC so long as the ownership interests remain the same before and after the transfer. The percentage of membership interests in the LLC must be the same as the ownership percentage interests before the transfer. Be aware that some states—such as Pennsylvania—tax the transfer regardless. Be sure to consult your state’s laws before moving forward with an LLC.

Will you have to pay a transfer tax? Some local jurisdictions charge a transfer tax on each title change, even if you move from your name to an LLC that you own. Check that out first. What is the cost? And is it worth it?

The Alternative to an LLC for Your Real Estate

There are a couple of other options instead of using an LLC for your real estate. One is to keep the property in your name and just take out a lot of insurance. This could be a useful strategy but it also leads to some trouble if a tenant sues. Mrs. Kennedy mentions that one of her clients “was being sued by a tenant on a frivolous charge. He had a good insurance policy, including an umbrella policy to cover his own possible acts. He went into the first meeting with the tenant’s lawyers who had dollar signs in his eyes. His insurance company had two lawyers in the meeting as well, so he felt well covered.”

Mrs Kennedy further explained that “it was an expensive lesson. After that, he always used LLCs that had been properly set up and maintained. I do believe in having insurance, but I also realize it’s not the ultimate solution to everything. You need something else.”

Another popular solution is to set up a trust. But is trust a good asset protection instrument? It depends.

There are a lot of different types of trusts, so it’s important to first understand whether it’s a simple or complex trust. (These are specific terms applicable to trusts.) Is it a revocable or irrevocable trust?

It’s impossible to give a blanket statement as to whether trust is a good idea for you or not.

Most likely, though, the trust most discussed is a grantor type trust, commonly called a land trust. These provide no asset protection but are useful in some states for privacy. They are best used as part of an estate plan and not for asset protection.

Some people use land trusts in conjunction with an LLC. That could be a better solution, but you now have two different entities to set up and manage.

Conclusion

Ultimately asset protection is especially important as you grow your assets. Don’t lose everything you’ve worked so hard for to a silly lawsuit!

If you have a specific situation that you would like to discuss further about accounting, asset protection and tax-saving strategies for real estate investments feel free to contact Huckabee CPA for a free consultation.

{kind=link}