Cryptocurrency investor tax reporting for 2023 tax season

The dramatic crash in cryptocurrency prices in 2022 and the bankruptcies of FTX and other crypto exchanges have added complexity to crypto taxes, while the IRS and Congress continue to crack down on tax cheating with digital assets.

Cryptocurrencies and other digital assets had a tumultuous 2022. The price of bitcoin dropped more than 60% during the year, and a number of crypto exchanges declared bankruptcy. Sam Bankman-Fried, the disgraced CEO of crypto exchange FTX, is awaiting trial on charges of fraud.

Crypto investors with assets at bankrupt exchanges are currently in limbo, according to Shehan Chandrasekera, a CPA who heads tax strategy at CoinTracker, a provider of crypto tax software told the Wall Street Journal, “they’ll have to wait until the bankruptcies are finalized to even think about taking tax deductions for their losses–and whether that will be allowed,” he says.

At the same time, the IRS and Congress have been trying to strip away excuses for millions of people who aren’t complying with tax rules on cryptocurrencies, either inadvertently or on purpose.

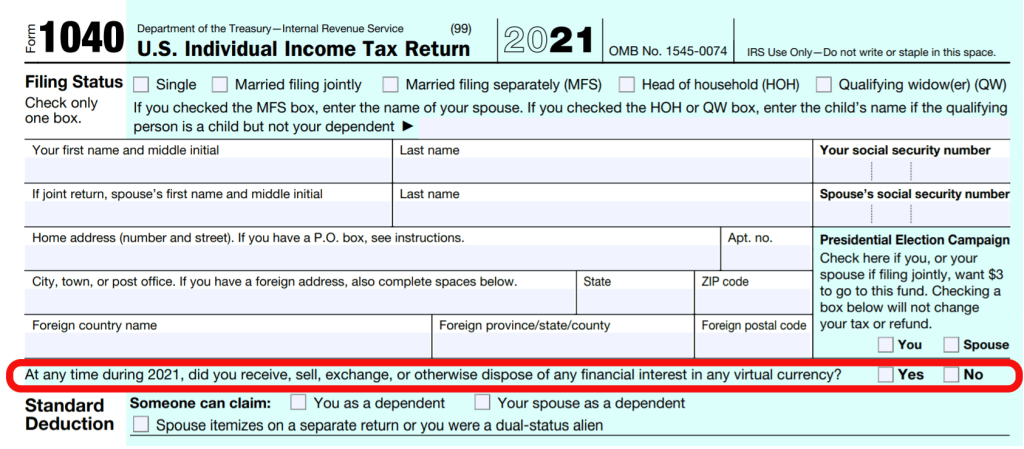

To encourage compliance, the agency now includes a pointed question on the front page of the individual tax return, just below the taxpayer’s name and address. For 2022 returns, the wording has been revised to include digital assets such as nonfungible tokens (NFTs) or stablecoins.

Some questions to ask:

- Do I have to tell the IRS that I own cryptocurrency?

- I have crypto. What do I need to know about taxes?

- Do I owe taxes on crypto if I use it to buy something?

- Do Congress and the IRS really care about unpaid taxes on crypto and other digital assets?

- What if my crypto assets are at FTX or another crypto exchange in bankruptcy proceedings?

(image credit:cnbc)

It says: At any time during 2022, did you:

- (a) receive as a reward, award, or compensation;

- or (b) sell, exchange, gift, or otherwise dispose of a digital asset or a financial interest in a digital asset?

The tax filer must check the box “Yes” or “No.” Cryptocurrency owners who skip the question or are untruthful risk higher penalties if the IRS audits them, as it will be hard to claim ignorance. More explanation of this question is on page 15 of the Form 1040 instructions.

The IRS also initiated other crypto enforcement efforts in 2022. It persuaded federal judges to authorize two new summonses requiring a crypto exchange and a bank to turn over to the IRS account information for customers who had $20,000 or more in crypto transactions in any one year from Jan.1, 2016 to Dec. 31, 2021. This strategy, known as a John Doe summons, is one the agency has used to investigate customers of three other crypto exchanges.

Congress is also trying to improve cryptocurrency tax compliance

Late in 2021, lawmakers passed the Infrastructure Investment and Jobs Act. This included a provision requiring crypto brokers to report customers’ sales proceeds to the IRS on a 1099 form if these assets are held in a taxable account. The requirements are akin to what brokerage firms report for investors’ stock sales.

This new reporting was supposed to take effect on Jan. 1, 2023. In late 2022, however, the IRS and the Treasury Department delayed the effective date until the agencies finish writing rules that clarify thorny issues such as who qualifies as a broker.

The WSJ article points out that IRS guidance on cryptocurrencies dates to 2014 when the agency said bitcoin and other cryptocurrencies are property, not currencies such as dollars or euros. Often they are investment property akin to stock shares or real estate.

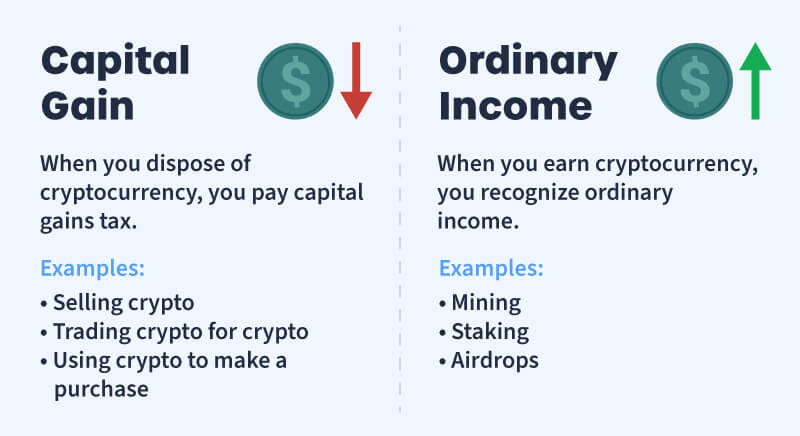

This means that if crypto is held in a taxable account–as opposed to a retirement account like an IRA or Roth IRA–then net profits from a sale are typically taxed as long-or short-term capital gains. Losses can be used to offset gains.

This tax treatment has benefits and drawbacks

The benefits include a lower rate on gains for cryptocurrency held longer than a year. Investors can also sell losers and use losses to offset investment gains from a range of investment assets that include real estate or stock. Unused losses can offset up to $3,000 of ordinary income such as wages, and losses above that amount carry forward for use against future gains.

Learn more about the taxation of cryptocurrencies, including tax triggers, lot identification and wash sales are here.

A key disadvantage is that if crypto is used to make a purchase–even of a sandwich– then the transaction typically generates a taxable sale that the buyer must report to the IRS.

Jack, for example, buys a boat with $12,000 of cryptocurrency that he purchased for $7,000. His transfer of the crypto is taxable. Jack has to report a taxable gain of $5,000 to the IRS–much as if he bought the boat with shares of stock that had grown from $7,000 to $12,000.

This makes cryptocurrencies a cumbersome substitute for cash.

In 2019, the IRS issued further guidance detailing the tax treatment of cryptocurrencies. If there is a reorganization that changes the network protocol of coins and results in the distribution of new tokens and the crypto owner receives something of value, then its fair market value is taxable at ordinary income rates when the taxpayer has control of it.

In late 2020, the Financial Crimes Enforcement Network (FinCEN), a Treasury Department unit separate from the IRS, announced it may require U.S. taxpayers holding more than $10,000 of cryptocurrencies offshore to file FinCEN Form 114, known as the FBAR, to report these holdings. This rule hasn’t yet been adopted, so it wasn’t in effect for 2022.

Taxes on Crypto Payments, Staking and Mining

If you earn cryptocurrency from mining, receive it as a promotion or get it as payment for goods or services, it counts as regular taxable income. You owe tax on the entire value of the crypto on the day you receive it, at your marginal income tax rate.

Any cryptocurrency earned through yield-earning products like staking is also considered to be regular taxable income.

If you hold cryptocurrency from any of these activities, and either spend or sell it later for more than its value when you first received it, you owe short- or long-term capital gains taxes on the profits, based on how long you’ve held it.

Keep Accurate Records

A recent Forbes article mentions that you need to account for all your cryptocurrency transactions, including how much you paid for crypto, how long you held it, and how much you sold it for, as well as receipts for each transaction. You’ll also need to note the fair market value of the cryptocurrency when it was used or sold.

While your crypto exchange may provide a 1099-B reporting your crypto transactions to both the IRS and you, it may not record the cost basis or the original amount you paid for your crypto if you transfer coins between offline cold wallets and your account.

Tools like Koinly and Cointracker connect to exchanges and crypto wallets to track your crypto transactions and complete the forms you need to file your cryptocurrency taxes.

Fill Out Tax Forms

Once you have a record of your crypto transactions, you’ll need to fill out certain tax forms depending on how you used your crypto. Here are some examples of forms that you may need to complete.

- Form 1040. This is the standard form you’ll use to file annual income taxes. On the form, there’s a line to report your total gains or losses from crypto.

- Form 1099-NEC. If you earn crypto by mining it, it’s considered taxable income and you might need to fill out this form.

- Form 8949. This form logs every purchase or sale of crypto as an investment. This should include the amount of crypto, the date and price you bought, the date and price you sold, and your gain or loss for each transaction.

- Schedule C. If you received coins from mining, you need to disclose whether you received them as a business or as a hobby. If you’re running a crypto mining business, you may owe self-employment taxes if your income exceeds your expenses for the year.

- Schedule D. This form summarizes your total capital gains and capital losses from all investments, including crypto.

- Schedule SE. You might use this form if you earned any crypto income through self-employment.

Key takeaways

- The IRS treats cryptocurrency as property, meaning that when you buy, sell or exchange it, this counts as a taxable event and typically results in either a capital gain or loss.

- When you earn income from cryptocurrency activities, this is taxed as ordinary income.

- You report these taxable events on your tax return using various tax forms.

- Keep records of your transactions so that you can inform the IRS of all your crypto activity during the year.

Conclusion

Preparing for cryptocurrency taxes can be complicated, especially since the laws surrounding them are constantly evolving.

You may want to consider consulting with a tax professional or using a tax software program specifically designed for cryptocurrency tax reporting to ensure that you are reporting your cryptocurrency transactions correctly and accurately.

If you’ve made a substantial income from cryptocurrency, it may be worth hiring a certified public accountant (CPA) who specializes in this type of tax work, so you don’t have the IRS chasing you down later.

{kind=link}