One of the most common questions that taxpayers ask is if they can still claim a deduction even if they don’t have the corresponding receipt. The simple answer to this question is yes, you can deduct without a receipt- the caveat is that taxpayers must proceed with extreme caution. The IRS and courts pay particular attention to deductions filed without receipts and have stringent rules that you must adhere to. The purpose of this article is to give small business owners insight into the terms they should follow to avoid penalties.

One of the most common questions that taxpayers ask is if they can still claim a deduction even if they don’t have the corresponding receipt. The simple answer to this question is yes, you can deduct without a receipt- the caveat is that taxpayers must proceed with extreme caution. The IRS and courts pay particular attention to deductions filed without receipts and have stringent rules that you must adhere to. The purpose of this article is to give small business owners insight into the terms they should follow to avoid penalties.

The following will be discussed:

- The Cohan Rule and Tax Deduction Receipts

- Exceptions to the Cohan Rule

- Tax Deduction Receipts vs. the Cohan Rule

- The Statute of Limitations for Receipts

- Accounts the IRS Scrutinizes Most Often

- IRS Concerns Regarding Small Businesses

The Cohan Rule and Tax Deduction Receipts

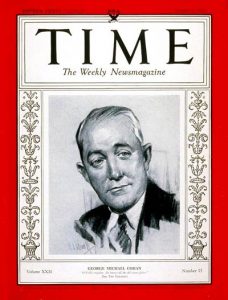

There was a famous Broadway playwriting pioneer named George M. Cohan who made hits such as “Give My Regards to Broadway” and “Yankee Doodle Boy.” His statue still stands in Times Square, though it is eclipsed by the bright lights and chaos. Many a taxpayer has been saved by this case and what it represents. The IRS disallowed Cohan’s large travel and entertainment expenses because he didn’t have receipts. He was a flashy guy and tended to pay in cash. And he wasn’t going to take no for an answer. So when the IRS denied all his deductions, he took the IRS to court. Receipts being the stock in trade of the tax system, the trial court upheld the IRS. Again, Mr. Cohan wouldn’t take no for an answer and appealed to the Second Circuit. The Appeals Court held for Mr. Cohan and against the IRS. The Cohan rule still allows taxpayers to prove by “other credible evidence” that they actually incurred deductible expenses. Mr. Cohan testified that he paid in cash, and others also supported Cohan and remembered big and expensive dinners. Of course, this is a tough way to prove expenses.

There was a famous Broadway playwriting pioneer named George M. Cohan who made hits such as “Give My Regards to Broadway” and “Yankee Doodle Boy.” His statue still stands in Times Square, though it is eclipsed by the bright lights and chaos. Many a taxpayer has been saved by this case and what it represents. The IRS disallowed Cohan’s large travel and entertainment expenses because he didn’t have receipts. He was a flashy guy and tended to pay in cash. And he wasn’t going to take no for an answer. So when the IRS denied all his deductions, he took the IRS to court. Receipts being the stock in trade of the tax system, the trial court upheld the IRS. Again, Mr. Cohan wouldn’t take no for an answer and appealed to the Second Circuit. The Appeals Court held for Mr. Cohan and against the IRS. The Cohan rule still allows taxpayers to prove by “other credible evidence” that they actually incurred deductible expenses. Mr. Cohan testified that he paid in cash, and others also supported Cohan and remembered big and expensive dinners. Of course, this is a tough way to prove expenses.

For background purposes, there is one tax court case you will want to familiarize yourself with: Cohan v. Commissioner, 39 F. 2d 540 (2d Cir. 1930). This court case set forth a national precedent in that it allows for the deduction of an expense even when a corresponding receipt cannot be produced; this is assuming that the taxed entity can produce a reasonable estimate as per exactly what the original expenses were. So it became the birth of the “Cohan Rule” whereby filing for a deduction without a receipt became possible. And, that is the good news.

Exceptions to the Cohan Rule

Now for the “not so good news.” As with most rules, there are exceptions- the Cohan Rule is living proof of this cliche. With the verdict and repercussions of the Cohan Rule, Congress was compelled to pass certain exceptions to the rule [IRC § 274(d)] regarding the following taxable expenses:

- Entertainment

- Travel

- Gifts

- “Listed property” described in [IRC § 280F(d)(4)] (computers, passenger vehicles, etc.)

Don’t waste any time trying to cut corners with the IRS by referencing the Cohan Rule for the expenses described above- this tactic simply will not work. Like it or not, you are required for producing any and all receipts for any expenses that fall into the above referenced four categories. The IRS has been known to meticulously analyze expenses claimed from these areas so maintaining additional records, other than receipts, is strongly encouraged. As an example, for an entertainment expense, it would be in your best interest to include relevant information that can back up your claim that an expense is indeed deductible.

Tax Deduction Receipts vs. the Cohan Rule

Just to emphasize though, it is absolutely always better to produce a receipt than claim your proposed deduction by waving the Cohan Rule flag. Should you be audited, you will most likely have a thorough discussion with an IRS representative regarding what exactly a “reasonable estimate” is- basically, it’s just so much easier to stay organized and keep on top of your receipt maintenance.

Four very relevant side notes should be considered:

- Businesses without adequate bookkeeping processes nearly always fail their audits, even if they have not done a thing wrong.

- Manual bookkeeping is cumbersome and more prone to errors- seriously consider a paperless recordkeeping system.

- Do not maintain your receipts, or any records for that matter, poorly. This might sound a little extreme but some printers are of the higher end than other printers- the same goes for printer ink. If your bookkeeping system is not automated, make sure your paper records can stand the test of time.

- Most taxpayers who use the Cohan Rule as a defense during legal action lose their case. The Cohan Rule explicitly states that a court can “bear heavily if it chooses on a taxpayer whose inexactitude is of his own making.” Good examples of this premise in action are Harlan, T.C. Memo. 1995-309, Sam Kong Fashions, Inc., T.C. Memo. 2005-157 and Stewart, T.C. Memo. 2005-212.

The Statute of Limitations for Receipts

A popular taxpayer question revolves around the length of time for which you need to maintain your receipt records. The general answer to this inquiry is three years. Most taxpayers maintain records, however, for the duration of six years because a court can ask for records dating back that far if the IRS believes gross income understatements or tax evasion might be present.

Accounts the IRS Scrutinizes Most Often

There are obvious and predictable areas where the IRS is going to focus on during an audit. The four previously mentioned non-Cohan Rule areas will, of course, be examined. Another area of scrutiny is accounts/line items, where large expenses occurred. The IRS knows the line items where, large expenses typically occur so if you have an astronomical number for your supply expenses, this is going to raise red flags because you can only spend so much on office materials. Red flags trigger an IRS request for receipts so that is another reason to make sure your records are pristinely maintained. And, more often than not, receipts are simply not enough to validate an expense; an auditor may want to review a corresponding credit card statement or check where the exact charge can be backed-up.

As far as small businesses go, the most popular type of audit is called a “BDA.” BDA is an acronym for “bank deposit analysis” and is basically just a process whereby an auditor sums up all your bank deposits and compares them to the income you stated for the year in question. Should a difference be detected, it is your responsibility to explain the discrepancy. As cash- basis accounting is normally used for this type of business size, it is important that you implement and use an accounting system that can accommodate the tracking of various types of cash and complete bank account reconciliations.

IRS Concerns Regarding Small Businesses

It’s necessary to outline a few documentation issues surrounding small businesses.

Sometimes, the line between a small business venture and hobby is blurry. So you have fun working at your small business, but is your small business really a small business and one that you can deduct losses for? Speak with a professional about issues like this because that individual can guide you in the proper direction.

As a second point, the line is also very blurry between personal expenditures and business expenditures. The IRS wants to know that you classified your expenses properly so it is imperative that your documentation is stellar.

Conclusion

Claiming losses and gains for tax purposes in a legitimate fashion obviously, minimizes any potential risk in an audit. The best advice? Save those receipts so you never have to argue the Cohan Rule. Speaking with a professional accountant like Thomas Huckabee, CPA of San Diego, California can help you with all the areas we mentioned and more. A tremendous amount of effort must go into the development of your accounting documentation and maintenance process. Contact us for a free consultation.