10 year-end tax saving strategies to lower your 2019 tax bill

New Year’s Eve and 2020 are almost here, U.S. citizens only have a few more weeks to get their “so-called” financial houses in order. Now the good thing is that individual tax filers should have better confidence in their strategies for year-end tax planning for 2019 compared to the previous year. The historic TCJA tax reform made filing taxes for 2018 a little confusing as both taxpayers and the IRS raced to deal with all the sweeping changes brought forth by Trump’s new tax legislation that was signed into law in December 2017. Now that IRS has issued more guidance on a number of issues, taxpayers can this year-end with a little more clarity. To assist businesses and individuals with preparing for tax filing season, I would like to give some 2019 year-end tax planning tips. The changes brought on by the Tax Cuts Job Act upends a lot of traditional tax planning so it’s recommended that you revisit the usual year-end strategy.

New Year’s Eve and 2020 are almost here, U.S. citizens only have a few more weeks to get their “so-called” financial houses in order. Now the good thing is that individual tax filers should have better confidence in their strategies for year-end tax planning for 2019 compared to the previous year. The historic TCJA tax reform made filing taxes for 2018 a little confusing as both taxpayers and the IRS raced to deal with all the sweeping changes brought forth by Trump’s new tax legislation that was signed into law in December 2017. Now that IRS has issued more guidance on a number of issues, taxpayers can this year-end with a little more clarity. To assist businesses and individuals with preparing for tax filing season, I would like to give some 2019 year-end tax planning tips. The changes brought on by the Tax Cuts Job Act upends a lot of traditional tax planning so it’s recommended that you revisit the usual year-end strategy.

Grant Thornton LLP wrote an interesting year-end tax tips article recently where Dustin Stamper, managing director in Grant Thornton’s Washington National Tax Office suggested that “A ‘wait and see’ approach to tax planning is no longer a viable option for taxpayers. Businesses and individuals alike have now seen tax reform play out, and they must adjust their tax planning in response. Limits on popular deductions like state and local taxes present challenges, but there are also new opportunities to employ transfer tax planning and defer capital gains with targeted investments.”

A recent article by a CNBC contributor Janet Alvarez titled “tax planning now can make a big difference in your 2020 IRS filing” made the suggestions that:

- It’s never too early so start planning for the 2020 tax season; in fact, the sooner you start the better filing results you can expect.

- Now is a good time to review your tax-advantaged retirement plan contributions, any household changes, potential deductions and withholding status.

Concerned about your upcoming tax bill?

Here ten useful 2019 year-end tax-planning and saving considerations for individuals:

1. Decide whether itemizing is still for you

It’s important to decide whether you expect to take the standard deduction before making decisions about year-end spending that would normally generate itemized deductions. Tax reform doubled the standard deduction while repealing or limiting numerous itemized deductions, such as a $10,000 cap on property and state and local income tax deductions. If your itemized deductions are unlikely to total at least $12,200 (or $24,400 if married and filing jointly), some may say it might make sense to go with the standard deduction, but at the same time, you should work closely with your tax specialist to make sure it’s the right choice, which will depend on factors ranging from your health expenses to charitable giving, which I discuss further in this article.

2. Defer tax

Deferral remains a cornerstone of solid tax planning. Why pay tax today when you can put it off until tomorrow and enjoy the time value of money? Deferring tax is about accelerating deductions and postponing income. You may be able to control the timing of items of income and expense. Consider deferring bonuses, consulting income or self-employment income. On the deduction side, you may be able to accelerate state and local income taxes, interest payments and real-estate taxes, but remember the $10,000 cap on deducting tax.

3. Utilize any stock losses to offset capital gains

Vinay Navani, a CPA at Wilkin Guttenplan wrote a tax tips article in Merrill Lynch and one of his suggestions is using stock losses to offset capital gains. Stating that “now may be a good time to consider selling certain underperforming investments in order to generate a capital loss before the end of the year—which could help offset the capital gains you realize when selling stocks that are performing well.” Also called “tax-loss harvesting”—which means selling investments such as stocks and mutual funds to realize losses. Because losses can offset capital gains, selling stocks or funds that have slumped in value can help reduce your tax bill. In addition, you may generally deduct up to $3,000 ($1,500 if married and filing separately) of capital losses in excess of capital gains per year from your ordinary income. If your net capital losses exceed the yearly limit of $3,000 ($1,500 if married and filing a separate return), you can carry over the unused losses to the following year. Note that under the new law, investors will continue to pay long-term capital gains taxes at a rate of 0%, 15% or 20% (depending on their overall income) but with adjusted cutoffs. Married couples filing jointly and earning $78,750 or less ($39,375 for singles) will pay nothing. Married couples filing jointly earning between that and $488,850 (or that and $434,550 for singles) will pay 15%, while married couples filing jointly and earning more than $488,850 or more ($434,550 for singles) will pay 20%. For more detailed guidance he suggests checking out IRS Revenue Procedure 2018-57.

4. Look for tax-aware investing strategies

If your income is at least $200,000 ($250,000 for married couples filing jointly or qualifying widow or widower, $125,000 for married filing separately), you’re subject to a 3.8% Net Investment Income Tax on either your net investment income or your modified adjusted gross income over the threshold amount, whichever is less. (Your tax advisor will understand.) Putting a portion of your income into investments not generally subject to federal income taxes, such as tax-free municipal bonds, probably won’t affect your tax picture this year, but could potentially ease your tax burden down the road when they start generating income.

5. Make your opportunity zone investment before year-end.

Now there has been a lot of discussions, podcasts, conferences and hype surrounding investing in “Opportunity Zones” and also a lot of confusing rules and guidance on it. Tony Nitti a Forbes Contributor wrote a detailed article titled “IRS Publishes Final Opportunity Zone Regulations: Putting It All Together” He also pointed out some people take issue with the long required holding periods, and the inability to enjoy losses or take distributions in the early years. If you are someone who is excited about investing in a qualified opportunity fund or qualified opportunity zone property to receive these generous tax incentives. If you have sold or are considering selling assets this year that would generate large capital gains, keep in mind the gain can be deferred if you invest an equal amount in an opportunity zone fund within 180 days of the sale. If you hold the investment for 10 years, you won’t recognize any gain on the new investment itself. You still have to recognize the original gain you deferred by Dec. 31, 2026, at the latest, but if you make your investment by the end of the year, an extra 5% will be forgiven. You can get up to 10% of the deferred gain forgiven entirely if you hold the investment for five years, or 15% if you hold it for seven years, meaning December 31, 2019, presents the last opportunity to qualify for the extra 5% step-up in basis. There are more than 8,000 opportunity zones throughout the U.S. in areas ripe for investment, and numerous funds are soliciting investors.

6. Maximize “above-the-line” deductions.

Above-the-line deductions are especially valuable because so many taxpayers will no longer itemize deductions. They also reduce your adjusted gross income (AGI), and AGI affects whether you’re eligible for many tax benefits. Common above-the-line deductions include traditional Individual Retirement Account (IRA) and Health Savings Account (HSA) contributions, self-employment taxes, certain health insurance costs and any bank penalties you may have had to pay for early account withdrawals. Note that tax reform repealed some popular above-the-line deductions, such as moving expenses (except for members of the military) and alimony payments (for divorces finalized after 2018).

7. Don’t squander your gift tax exclusion

You can give up to $15,000 to as many people as you wish in 2019, free of gift or estate tax. You get a new annual gift tax exclusion every year, so don’t let it go to waste. If you combine gifts with your spouse, you can use your exemptions together to give up ($30,000 per beneficiary each year from a married couple), without reporting it to the IRS. So if you have three married children, you could give each couple $60,000 and remove $180,000 from your estate in a single year. You can give even more tax-free if you have grandchildren. Generally, once the gift is made, your estate will not pay estate taxes on it, and it will not be considered taxable income for the recipient. However, also remember that the donor’s tax basis for gifts carries over to the gift’s recipient, subject to a few qualifications—which means that in some cases, waiting to give could make sense. Also, the lifetime federal gift and estate tax exemption have more than doubled, to $11.40 million for individuals ($22.80 million for couples), meaning that far fewer estates will owe estate tax.

Charitable gifts such as cash or appreciated stock are still tax-deductible if you itemize, but not if you take the standard deduction. If you give regularly to charities, consider putting several years’ worth of gifts into a donor-advised fund (DAF) for a single year—that step may make it worth your while to itemize. Vinay Navani suggests. “Then, you can spread out the giving from the DAF over the next several years, based on your charitable intent.”

Another change: Taxpayers who itemize can now deduct cash charitable contributions of as much as 60% of their adjusted gross income, up from 50%. That could work to the benefit of, say, a retired person with significant assets and modest living expenses.

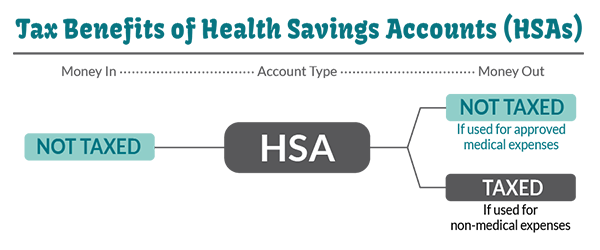

8. Cover health care costs efficiently

Both health savings accounts (HSAs) and flexible spending accounts (FSAs) could allow you to sock away pretax contributions for qualified medical expenses that your insurance doesn’t cover.

Both health savings accounts (HSAs) and flexible spending accounts (FSAs) could allow you to sock away pretax contributions for qualified medical expenses that your insurance doesn’t cover.

But there are key differences to these accounts. Most notably, you must purchase a high-deductible health insurance plan and you cannot have disqualifying additional medical coverage, such as a general-purpose FSA, in order to take advantage of an HSA.

One important benefit of HSAs is that you don’t have to spend all of the money in your account each year. Though some employers allow you to roll over as much as $500 in FSA funds from year to year, generally, the funds you contribute to an FSA must be spent during the same plan year.

Also, while you can deposit funds into an HSA up to the tax filing due date in the following year, up to the maximum dollar limit, and still receive a tax deduction for the current tax year (e.g., you can make your 2019 contribution by April 15, 2020), FSA contributions are generally only elected during open enrollment or when you become an employee of a company.

Be sure to check your employer’s rules for FSA accounts. If you have a balance, now may be a good time to estimate and plan your health care spending for the remainder of this year. In addition, see if the account balance can be used to reimburse you for qualified medical costs you paid out-of-pocket earlier in the year.

9. Leverage retirement account tax savings

Grant Thornton LLP suggests “It’s not too late to maximize contributions to a retirement account. Traditional retirement accounts like 401(k)s and IRAs still offer some of the best tax savings in the tax code.” Contributions reduce taxable income at the time you make them, and you don’t pay taxes until you take the money out at retirement. The 2019 contribution limits are $19,000 for a 401(k) and $6,000 for an IRA (not including catch-up contributions for those 50 years and older). Remember that 2019 contributions to your IRA can be made as late as April 15, 2020. And the IRS just announced the increased 2020 retirement plan contributions and benefits limits.

10. Make up a tax shortfall with increased withholding

Many taxpayers were unpleasantly surprised by smaller refunds or unexpected bills when they filed their 2018 returns because of changes to tax rules and withholding schedules. This year, make sure your withholding and estimated taxes align with what you actually expect to pay while you have time to fix a problem. With just a few weeks left in 2019, it’s important to check whether enough has been taken out of your paycheck this year to cover your taxes. The Internal Revenue Service has a handy calculator that can help you determine whether you should adjust your withholding. Self-employed workers, however, should have been making quarterly payments throughout the year.

If you find yourself in danger of being penalized for underpaying taxes, you can make up the shortfall through increased withholding on your salary or bonuses. A larger estimated tax payment at the end of the year can still expose you to penalties for underpayments in previous quarters, but withholding is considered to have been paid ratably throughout the year, so increasing it for year-end wages can save you in penalties.

This article summarizes many different tax planning matters. We invite you to contact Thomas Huckabee CPA for any questions or free consultation to help navigate any of these.

{kind=link}