How Biden’s Tax Plan Proposals Could Impact Real Estate Investors

CNBC recently reported back in May, that real estate investors may soon pay more taxes on high-dollar transactions.

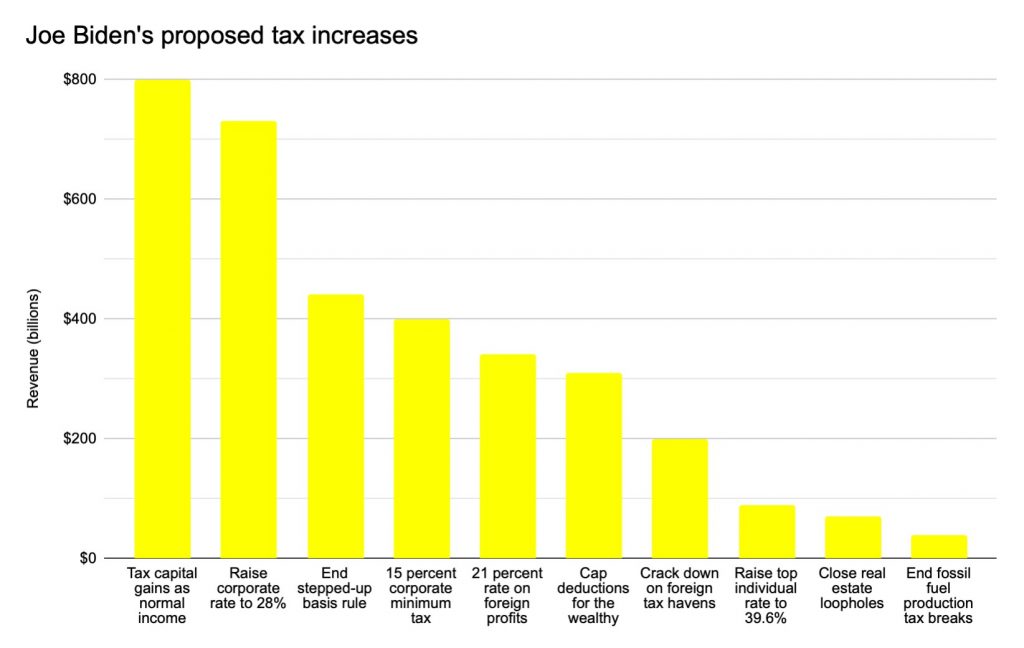

President Joe Biden has been asking for higher taxes on real estate transactions with gains of more than $500,000. This tax plan is aimed at helping to cover the $1.8 trillion American Families Plan, which pumps money into child care, paid family leave, and education programs.

However, financial experts say the tax hike may also put a strain on smaller investors.

The strategy on the chopping block — so-called like-kind or 1031 exchanges — allows investors to defer paying taxes on real estate by rolling profits into their next property. An article published in Kiplinger in June 2021, by Dwight kay, asks “Should you sell your real estate investments before any changes to capital gains taxes or 1031 exchanges get made? That’s what many people are asking.” He went on to say “but before you do anything, understand that there’s no telling what will come of President Biden’s tax proposals with a divided Congress, and you do have some interesting options in the meantime.”

Biden Real Estate Tax Proposals: The Big Picture

(Image credit: Thinkadvisor)

Stephen Nelson, a CPA of Evergreen Small Business, recently blogged about this topic and explains that “a theme appears in Mr. Biden’s proposals. That theme? Investors and entrepreneurs need to pay higher tax rates as their wealth and income grow. In most situations, for example, Mr. Biden proposes to rather substantially bump up the taxes on big investment windfalls and entrepreneurial profits.”

Let’s talk about the ways Mr. Biden proposes to raise taxes on real estate investors.

High-Income Real Estate Investors Hit with Obamacare Tax

A first tax bump? Mr. Nelson, states in his article that President Biden wants real estate investors with high incomes to pay either the 3.8 percent net investment income tax. Or the 3.8 percent self-employment contributions act tax. Mr. Biden wants those real estate investors with large adjusted gross incomes to pay the 3.8 percent tax on the chunk of their business income above $400,000.

He cites an example, as saying “a real estate investor earns $500,000 from her or his real estate investments. This investor pays a 3.8 percent tax on the last $100,000 of income. That amount equals $3800.”

Mr. Biden proposes making this tax increase effective starting in 2022.

Section 1031 Like-kind Exchanges Limited

In terms of tax policy, now on the table from the Biden administration are some proposals with the potential to affect investment in real estate: an increase in the capital gains tax rate and limits on the use of 1031 like-kind exchanges. (Basically, 1031 exchanges allow property investors to defer capital gains and other taxes on investment gains when they reinvest the proceeds in other investment properties.) Biden has proposed raising the capital gains tax rate to 39.6% for people making more than $1 million a year.

According to data from a 2020 survey from the National Association of Realtors, around 12% of real estate sales were part of a 1031 exchange from 2016 to 2019. According to reporting from the WSJ, A U.S. congressional tax committee estimated that the 1031 tax break would save property investors more than $41 billion between 2020 and 2024.

For example, if an investor buys a property for $100,000 and it appreciates in value to $1,000,000? She or he can probably exchange, or swap, that $1,000,000 property for another $1,000,000 property and avoid paying taxes.

Mr. Biden proposes dialing down this tax-deferral trick, however. He suggests tax law limit taxpayers to deferring no more than $500,000 annually using the Section 1031 like-kind exchange rules.

The bookkeeping and tax return arithmetic for like-kind exchanges gets tricky. But we guess that real estate investors who historically used a like-kind exchange to delay paying taxes may want to reconsider that tactic from this point forward.

Mr. Biden proposes making this tax increase effective starting in 2022.

Many investors are hoping that the capital gains tax rate is not increased. The Kiplinger article author believes that a favorable capital gains tax rate encourages just that — capital investment. But let’s say the rate goes up: How would that affect real estate investments? Generally speaking, it would potentially reduce returns, but it would also reduce returns on all manner of investments, including on the sale of stocks, bonds, and other assets. So any hit to your investment real estate portfolio wouldn’t be pretty but could be proportionate.

In that environment, the reasons for a diversified portfolio of stocks, bonds and alternative investments that include real estate would be the same as they are now: to try to reduce risk by holding a mix of assets, including hard assets, that are not all correlated with the stock market. Investment real estate, as a reminder, doesn’t rise and fall, as a class, with the stock market. And there is the potential to generate income (positive cash flow) in addition to potential appreciation. There also are other tax advantages of real estate investment, including depreciation deductions to help shelter income.

Although Biden’s plan targets the wealthy, the proposal may also hit smaller investors.

The Realtors survey showed 84% of 1031 exchanges were by smaller investors — those in sole proprietorships (47%) or S corporations (37%).

Matt Berquist, a Jacksonville, Florida-based certified financial planner told CNBC “there will be some unintended consequences if it all goes through.” Small businesses looking to exchange property may face some tough decisions.

Currently, investors can use 1031 exchanges to buy and sell tax-deferred real estate throughout life. If the investor holds the property until death, they can pass it on to heirs tax-free.

No Preferential Tax Rate for Capital Gains Taxes for High-Income Investors

Another tax increase Mr. Biden is proposing is that investors with seven-figure taxable incomes pay ordinary income tax rates on at least some of their capital gains.

This reminder. Middle-class taxpayers usually pay a zero-percent long-term capital gains tax rate. Upper-class taxpayers usually pay a 15 percent long-term capital gains tax rate. And sometimes, if the taxpayer’s income gets high enough? A 20 percent long-term capital gains rate.

Mr. Biden proposes that all these taxpayers continue to pay the same zero, 15, or 20 percent long-term capital gains rate.

But here is the rub? Once a taxpayer’s taxable income crosses the $1,000,000 threshold, he wants the taxpayer to pay the highest marginal tax rate. For 2021, that tax rate equals 37 percent. He proposes bumping up that rate to 39.6 percent after 2021.

Mr. Nelson gives another example by using some simpler numbers: Say a taxpayer earns $500,000 in W-2 wages and then receives a $1,000,000 long-term capital gain from the sale of a real estate investment.

The first $500,000 of the real estate investment gains get taxed as long-term capital gains. Probably, the rate equals 20 percent. The last $500,000 of the real estate investment gains get taxed as, essentially, ordinary income. Mr. Biden wants that rate set at 39.6 percent.

Accordingly, this taxpayer doesn’t pay a 39.6 percent long-term capital gains tax on all their capital gain. The taxpayer pays a blended long-term capital gains tax rate. Roughly 30 percent with the example numbers given.

Biden wants to Eliminate Step-up in Basis

(image credit: SFtaxcounsel)

Another tax benefit that applies to direct real estate investment, which is the Section 1014 step-up in basis.

Section 1014 says the cost basis of any asset (like real estate) that you own when you die gets “stepped up” to its fair market value at the date of death. Your heirs can then sell the appreciated or the previously depreciated real estate without paying tax.

Or they can continue to rent the property but begin depreciating the property all over again. This is a great benefit.

But recent proposals from Mr. Biden have stated that he wants to eliminate the step-up in basis that currently occurs when a taxpayer dies. As part of his American Families Plan, President Biden wants to change the way capital assets are taxed when you die.

President Joe Biden is calling for the elimination of the step-up in basis, for gains exceeding $1 million, single taxpayers – $2.5 million for couples, which would subject years of accumulated appreciation to taxes. Eliminating the decades-old loophole tax break — known as a “step-up in basis” at death — would raise $113 billion over a decade starting in 2022, when coupled with a higher tax on capital gains, according to an analysis from the University of Pennsylvania’s Wharton School.

Mr. Nelson’s article gives an example, say your grandfather bought an apartment house for $100,000 decades ago and even enjoyed years of tax-free rental income from depreciation deductions. Then, say he died with the apartment part of this estate and he bequeathed the apartment house, now worth $1,000,000, to your mom. Neither the estate nor your mom owes taxes in this situation. In fact, your mom can sell the apartment building for $1,000,000. And pay zero income taxes. Or she can continue to hold the property and restart depreciation deductions based on the stepped-up $1,000,000 value. Under current laws, this strategy can be used for future generations.

Another example, say your father was to hold the property in his estate and then you inherit the apartment house when it’s worth $10,000,000, under current law, you can sell the property for $10,000,000 without paying income taxes. Or you can continue to hold the property and also restart the depreciation deductions based on that $10,000,000 valuation. These are tax savings techniques that wealthy families use to transfer wealth and shield tax liabilities.

Mr. Biden has responded with two proposed tax law changes. First, he eliminates the step-up in basis. Second, he wants to tax the economic gain the decedent would have realized if she or he had sold the property on the date she or he died. According to a recent CNBC article, without the step-up, heirs and tax professionals will have to chase down the decedent’s basis to determine the applicable taxes. This can be complicated for certain assets. Coupled with a bid to raise long-term capital gains rates to 39.6% from 20% for households making over $1 million, wealthy heirs could be in for a pile of taxes.

But determining Uncle Sam’s cut could be difficult for certain assets. That’s because the basis – or the owner’s original investment in the asset – could be hard to track.

Conclusion

In the short term, some property investors may be wondering: “Should I sell now to get ahead of any change in the capital gains tax rate?” The simple answer is maybe. There is no one-size-fits-all answer for everyone. It depends on your individual situation and the property you’re holding. If its value has held up well during the pandemic and you need to sell, it may make sense. If the value has declined but is poised for a rebound and you don’t need the proceeds now, it may make sense to wait. Of course, consult your tax or legal adviser as you consider the options, because everyone’s individual situation is different.

Whether Mr. Biden’s tax proposals become written into law? Who knows for sure. But clearly, taxpayers emphasizing real estate investments want to carefully follow the discussion. Further, if even some of the Biden real estate tax proposals become law, many real estate investors will want to reassess their strategy and tactics. Recently, the Treasury Department’s “Green Book” has also laid out a 114-page explanation of the Administration’s Fiscal Year 2022 Revenue Proposals. Thomas Huckabee CPA has extensive experience finding creative accounting and tax advisory solutions to meet the needs of a wide range of real estate-related businesses. Have questions, feel free to reach for a free consultation.

{kind=link}