Are you getting a feeling of Deja Vu, or that history is repeating itself? Does it feel quite similar to this time of the year back in 2017? Similarly back In the fall of 2017, it was unclear whether the Tax Cuts and Jobs Act (TCJA) would be enacted. There were several provisions being argued about and there was no clear path to passage. Fast forward to where we are today in the fall of 2021. The CPA firm Baker Tilly writes that “the $3.5 billion “human” infrastructure reconciliation package remains mired in debate between moderate and progressives within the Democratic Party.”

This gigantic bipartisan infrastructure bill is also tangled up in a similar battle, with the legislation’s future likely tied to the outcome of a successful budget reconciliation package negotiation. And with little likelihood that the Republicans would support these tax hikes, it remains that all but Democratic votes will be needed in the House and all 50 Democratic senators will be needed for passage using the reconciliation process.

So “the million-dollar question” is what does this mean for you?

At this moment in time, it’s not easy to guess, since the contents of the reconciliation bill are still being debated. And whether the spending package’s top line is $1.5 trillion,(Senator Joe Manchin will only support that number) $3.5 trillion or some amount in between, if Democrats are able to compromise and successfully pass a bill, it’s certain to include major tax changes. These changes could come in the form of a capital gains rate increase, corporate and individual rate increases, and modifications to the estate and gift tax.

Based on the initial House Ways and Means Committee bill, most of the provisions would not become effective until 2022, with the notable exception of capital gains (currently proposed for an effective date of Sept. 13, 2021).regardless, as business owner, you should be monitoring the progress of the ongoing negotiations carefully.

The CPA firm Baker tilly suggests a strategy of “accelerating income into 2021 and deferring significant expenses until 2022 where practical may be the best planning strategy depending upon your tax bracket.” When it comes to the issue that is on the legislative table, Capital Gains, if a September effective date remains, the planning door may have closed; however, it is possible there will be a change in effective dates as negotiations progress, possibly to the date of enactment or even Jan. 1, 2022. This 2021 year end tax planning article will cover what are the tax code modifications being considered, critical issues in healthcare and employee benefits, state and local tax trends as well as important reminders of expiring taxpayer-friendly provisions enacted via previous COVID-19 stimulus legislation.

The Reconciliation Bill

There are two bills moving through Congress. The first is the $1.2 trillion bipartisan infrastructure bill, which has passed the Senate and contains only very modest tax changes. It remains held up in the House, as some progressive congressional members are withholding support while they negotiate for a larger $3.5 trillion “human” infrastructure reconciliation package, officially known as the Build Back Better Act, to also be passed by the Senate. This has effectively linked the two bills, at least for the time being. The future of the bipartisan infrastructure bill likely depends on the success of the Build Back Better Act, which can only pass via the reconciliation process.

Baker tilly also wrote a pretty informative article on these changes, The tax components of the Build Back Better package cleared the Ways and Means Committee in September and await action on the House floor. It is increasingly looking like the Senate will not produce its own version of the bill, but rather negotiate the final package with the House and any changes (such as a state and local tax cap modification or limitations on estate “step-ups”) would be incorporated through amendments on the House floor before the final package is sent to the Senate for consideration.

The current Ways and Means bill, which includes a majority of President Biden’s priorities, is likely to be the initial framework of any successful legislation. Below are a few key provisions from the bill:

Individual provisions

- Top ordinary income rate increase: Rate would bump up to 39.6% from 37%

- Top capital gains rate increase: Long-term capital gains and qualified dividends would be taxed at 25%, up from the current 20%; this would generally be effective for gains recognized after Sept. 13, 2021 (an exception applies to transactions that are under a binding contract but have yet to be executed)

- High-income surtax: A new 3% surtax would be imposed on individuals with modified adjusted gross income (MAGI) over $5 million ($2.5 million for married taxpayers filing separately) and trusts and estates with MAGI greater than $100,000

- Retirement account changes: Individuals with retirement account balances of $10 million or more, who meet certain income thresholds, would have to take required minimum distributions of 50% of the amount by which the account exceeds $10 million, regardless of age; additionally, high-income taxpayers would no longer be able to contribute to Roth IRAs via “back-door” contributions

Trust and estate provisions

- Gift and estate tax exemption reduced: The unified credit that rose to $10 million (indexed for inflation) under the TCJA and is set to expire at the end of 2025 would instead expire at the end of 2021; the unified credit would become $6.02 million (indexed for inflation) in 2022

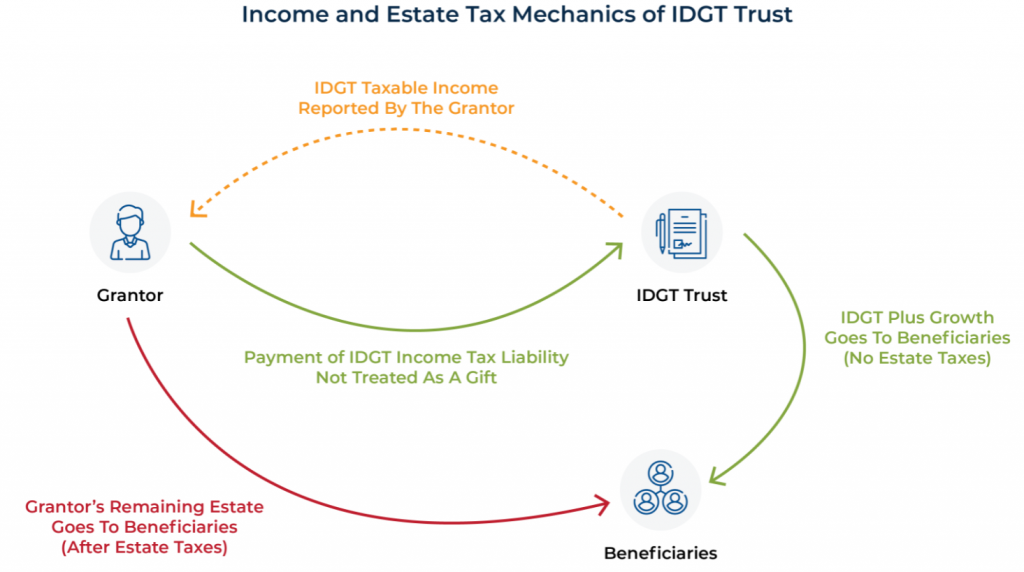

- Grantor trusts included in estate: The transfer to a grantor trusts would no longer be an effective estate planning strategy; for post-2021 transfers, grantor trust assets would be placed into a decedent’s estate when the decedent was the deemed owner of the trust

Business provisions

- Top corporate tax rate increase: Rate would jump to 26.5% from 21% for taxable income over $5 million; a lower 18% rate would apply to taxable income of $400,000 and under, while the 21% rate would continue to apply to taxable income above $400,000 but not grater than $5 million; once a corporation reaches $10 million in income, the graduated rates disappear and all income would be taxed at 26.5%

- Qualified business income deduction limitation: The 20% qualified business income deduction under IRC section 199A would be limited to annual deductions of $500,000 for married filing joint returns and $400,000 for single and head-of-household filers

- Net investment income tax (NIIT) expansion: All trade or business income for taxpayers with taxable income over $400,000 ($500,000 for joint filers) would be subject to the NIIT, regardless of material participation, unless it is subject to self-employment tax

- Excess business loss limitation: The $500,000 current-year loss limitation for noncorporate taxpayers that was set to expire after 2025 would be made permanent, and it would treat any suspended losses as a deduction instead of a net operating loss, thereby subjecting it to testing and potential limitation in subsequent years

- Carried interest modification: In order to obtain capital gain treatment, carried interests would need to be held for five or more years, up from three years

Expiring tax provisions

Over the course of the COVID-19 pandemic, Congress enacted several packages of stimulus legislation, including the Families First Coronavirus Response Act (FFCRA), the Coronavirus Aid, Relief, and Economic Security (CARES) Act, the Consolidated Appropriations Act, 2021 (CAA) and the American Rescue Plan Act of 2021 (ARPA). Each of these laws contained targeted tax modifications to relieve some of the economic burden caused by the coronavirus. Many changes delayed the implementation of Tax Cuts and Jobs Act of 2017 (TCJA) provisions, while others granted temporary relief from long-standing tax statutes. Here are a few that would like to mention.

Payroll tax deferral

The CARES Act allowed employers to defer deposit and payment of the employer’s portion of Social Security taxes and self-employed individuals to defer their equivalent portions of self-employment taxes otherwise due between March 27, 2020, and Dec. 31, 2020. Deferred deposits must be made by the following dates to be treated as timely (to avoid penalties and interest charges):

- 50% of deferred amounts due Dec. 31, 2021

- Balance of deferred amounts due Dec. 31, 2022

Any taxpayers who utilized the deferral must deposit the first 50% (or more) of the amount deferred by the end of the calendar year. It is important to note the IRS recently determined that a failure to deposit any portion of the deferred taxes by the applicable installment date would result in a section 6656 failure to deposit taxes penalty on the entire deferred amount going back to the original due date. To avoid costly penalties, employers and self-employed individuals with deferred payroll deposits or payments should pay a minimum of 50% no later than Dec. 31, 2021.

Employee retention credit

The employee retention credit (ERC) was one of the hallmark tax provisions included in the CARES Act, incentivizing employers to continue paying employees despite operations being affected by COVID-19. The payroll tax credit has been available to eligible trades or businesses as follows:

- 2020: ERC of 50% of qualified wages of up to $10,000 per employee (for the year)

- 2021: ERC of 70% of qualified wages of up to $10,000 per employee per quarter

– Important note! The proposed bipartisan Infrastructure Investment and Jobs Act (IIJA), if enacted, will remove the fourth-quarter eligibility for most taxpayers, ending the credit as of Sept. 30, 2021 - Third and fourth quarter 2021: Recovery startup businesses (broadly, qualifying employers that began operating a trade or business after Feb. 15, 2020, and meet additional requirements) are eligible for an ERC of 70% of qualified wages of up to $10,000 per employee per quarter, subject to a limit of $50,000 per quarter

Retirement plan changes

The CARES Act brought about two retirement plan changes, both of which expired at the end of 2020:

- Waived required minimum distributions (RMDs): This relief only applied to 2020. RMDs are compulsory for 2021 for taxpayers 72 and older. RMDs must be withdrawn by the end of 2021 to avoid potentially significant penalties.

- Retirement account hardship withdrawals: The CARES Act allowed for hardship withdrawals from eligible retirement accounts of up to $100,000 per participant without incurring the 10% withdrawal penalty through 2020. Taxpayers could choose from one of two treatments: (1) take the distribution as taxable income with the election to pay tax over a three-year period, or (2) repay the distribution amount over a three-year period. Taxpayers who made such withdrawals will need to make a repayment or recognize taxable income in 2021, accordingly.

IRS enhances compliance enforcement

The IRS, through its Large Business and International Division (LB&I), has been steadily increasing its compliance enforcement. LB&I oversees and directs tax administration for domestic and foreign businesses with at least $10 million in assets as well as U.S. tax reporting requirements. It also conducts compliance programs for high-wealth taxpayers and international individuals. With almost 60 different enforcement campaigns aimed at various subcategories of taxpayers, resources continue to be poured into LB&I in order to collect the greatest amount of tax revenues.

Areas targeted for expanded enforcement include compliance with the many changes due to the Tax Cuts and Jobs Act of 2017 (TCJA) and other legislation, high-wealth taxpayers, and partnerships and other pass-through entities. These campaigns are designed to identify and audit certain non compliant taxpayers as well as gather data as to how taxpayers adopted recent changes to the tax code and other regulatory guidance. Impacted taxpayers could experience longer examination time frames (from beginning to end) and may be required to supply more information to the IRS agent in order to wrap up the audit. In addition, the IRS may use more soft compliance measures, such as letters, advising taxpayers of an underpayment and advising of a need to file an amended return within months of the correspondence. To learn more about this subject read this Baker Tilly article.

Virtual Currency Tax Compliance

When the IRS first issued tax guidance on virtual currency, a single Bitcoin was worth approximately $573. At the time of this writing, that value has increased to over $55,000. As a result, the IRS and other federal government agencies continue to expand efforts to enforce reporting compliance for taxpayers that transact in virtual currency. Virtual currencies such as Bitcoin, Ethereum, Litecoin and Ripple are gaining traction as viable currencies for a wide range of transactions. However, their increasing acceptance by the public also brings increased scrutiny by the IRS for reporting and compliance. In fact, Congress is currently negotiating stricter reporting requirements on the part of brokers and other handlers of virtual currency in the infrastructure and reconciliation bills. Furthermore, the Department of Justice indicated in a legal filing that there could be instances where virtual currency may not always be considered property for federal tax purposes. Read this in depth Baker tilly article on all compliance developments.

Taxpayers who sell virtual currency are required to report the sale on Schedule D of Form 1040. Unlike stocks held in brokerage accounts, virtual currencies typically are not reported on a Consolidated 1099 Tax Statement. Taxpayers may receive a 1099-K or 1099-B related to their virtual holdings. All copies of 1099 forms are sent by the issuer to the taxpayer and the IRS. If a 1099 is not issued, the taxpayer will need to determine the cost basis and sales price of the virtual currency.

Legislative developments

The largest revenue-raiser included in the infrastructure bill, estimated to generate $28 billion over 10 years, results from increased enforcement on cryptocurrency transactions. Reporting requirements to the IRS for brokers would now include virtual currency transactions, including purchases, sales, transfers and transactions exceeding $10,000.

2021 Form 1040

Slightly modified from 2020, the 2021 draft Form 1040 asks the following question on Page 1: At any time during 2021, did you receive, sell, exchange, or otherwise dispose of any financial interest in any virtual currency? The question appears underneath the name and address fields.

Employee benefits update

As we move into the final quarter of 2021, all eyes are on the budget reconciliation bill, which includes retirement plan provisions to help fund the $3.5 trillion bill under consideration in Congress. If passed, the legislation would require mandatory distributions and IRA contribution limitations for high-income taxpayers with retirement account balances over $10 million and require distributions of Roth balances in excess of $20 million. Additionally, the Securing a Strong Retirement Act of 2021, a bill with bipartisan support, commonly referred to as SECURE 2.0, remains stalled in Congress. SECURE 2.0 builds upon the Setting Every Community Up for Retirement Enhancement (SECURE) Act of 2019 with the goal to increase retirement savings and simplify and clarify retirement plan rules.

For 401(k) plan sponsors, long-term, part-time employee eligibility requirements take effect in 2021

For sponsors of 401(k) plans, long-term and part-time employees are eligible to participate, effective for plan years beginning on or after Jan. 1, 2021. Under this rule, if a part-time employee has worked at least 500 hours in three consecutive years and is at least 21 years old by the last day of the three consecutive-year period, he or she must be offered the opportunity to make elective deferrals to the employer’s 401(k) plan. For purposes of determining whether an employee has worked at least 500 hours per year in three consecutive years, plans are not required to take into account hours of service in plan years beginning before Jan. 1, 2021. As a result, although affected plan sponsors will need to start tracking hours for this purpose beginning in 2021, plans will not be required to permit qualifying long-term or part-time employees to make deferrals under 401(k) plans before plan years starting in 2024.

Pooled employer plans for retirement benefits

Unrelated employers without any commonality may pool their resources by participating in a new type of multiple employer plan (MEP). The new retirement plans, referred to as pooled employer plans or open MEP, are treated as a single plan. In addition, the “one bad apple” rule no longer applies provided the procedure is followed for ensuring that one employer’s failure to meet the qualification requirements will not result in the disqualification of the MEP or open MEP. This is effective for plan years beginning on or after Jan. 1, 2020.

These tax proposals provide accounting method planning opportunities for businesses in 2021

Business taxpayers facing potential tax rate increases under the proposed House Ways and Means reconciliation bill may benefit from making accounting method changes to generate permanent cash tax savings by accelerating income to a lower rate tax year. TFor example, if the top corporate tax rate increases to 26.5% from 21% in 2022 (as currently proposed under the House Ways and Means reconciliation bill), a taxpayer can realize permanent cash tax savings of 5.5% by accelerating income into the lower rate 2021 year or, conversely, by deferring deductions until 2022 to offset higher-taxed income in that year. However, taxpayers should carefully evaluate alternative scenarios and monitor the status of pending legislation before implementing strategies to increase taxable income because the tax rules governing the various provisions are complex and are subject to change under the proposed reconciliation bill. Read this comprehensive article, by Baker Tilly on all the automatic accounting methods changes that a company could do.

BDO wrote a recent article that lays out possible traditional accounting method changes such as:

- Deferring income recognition of advance payments for goods or services, sale or license of computer software, use of intellectual property or eligible gift card sales;

- Deferring taxable income by changing from the overall accrual to the overall cash method of accounting;

- Deducting certain prepaid expenses (e.g., insurance premiums, property taxes, governmental permits and licenses, software maintenance) qualifying under the “12-month rule”;

- Deducting eligible accrued compensation liabilities that are paid within 2.5 months of year end;

- Accelerating deductions of liabilities such as warranty costs, rebates, allowances and product returns under the “recurring item exception”;

- Deducting “catch-up” depreciation (including bonus depreciation) by implementing permissible method changes, such as changing to shorter recovery periods identified through a cost segregation study; and

- Optimizing uniform capitalization methods for direct and indirect costs of inventory, including changing to simplified methods.

Plan your estate before it’s too late

The clock is running down, on estate planning as we know it. Soon, one of the most favorable planning eras will likely come to an end. Recent months have seen a myriad of tax proposals seeking to eliminate many popular wealth-transfer techniques.

Since March of this year, no fewer than four proposals have been released to modify current gift and estate tax rules. Most recently, on Sept. 12, 2021, the House Ways and Means Committee issued its proposal for the budget reconciliation bill. The draft legislation includes several significant changes affecting high-income and high-net-worth individuals, but from an estate planning perspective, it proposes to:

- Add a surcharge on high-income trusts and estates: The proposal would apply a 3% surtax on trusts and estates with adjusted gross income over $100,000. This change would be effective for tax years after Dec. 31, 2021.

- Reduce the gift, estate and GST tax exemptions: The proposal would reduce the gift, estate and generation-skipping transfer (GST) tax exemptions to their 2010 levels. Indexed for inflation, this would result in the 2022 exemptions equal to approximately $6 million per person, or $5.7 million less than the 2021 amount of $11.7 million per person.

- Pull grantor trusts into decedent’s estates: The proposal would require grantor trusts to be included in their deemed owner’s estate. This change would apply to grantor trusts created after the date the provision is enacted (which could be this year) or to any portion of a grantor trust created before enactment attributable to a contribution made on or after such date. Although not clear at this point, the proposal could eliminate planning with grantor-retained annuity trusts (GRATs), qualified personal residence trusts (QPRTs) and certain charitable lead trusts.

- Tax certain sales between grantor trusts and their owners: The proposal would cause sales between grantor trusts and their deemed owners to be taxable. Traditionally, taxpayers have been able to sell assets to their grantor trusts without recognition of gain and without receiving taxable income on any corresponding note payments. This provision, which could be effective this year (on the date of enactment), would change that.

- Eliminate valuation discounts for nonbusiness assets: The proposal would effectively eliminate valuation discounts for passive assets not used in an active trade or business. This provision would be effective on the date it is enacted.

In addition to the House proposal, three other proposals were released earlier this year. Some of the concepts included in those proposals were incorporated into the House bill but others were not. Notable absent provisions include increasing estate tax rates, capping annual exclusion gifts, limiting the duration of dynastic trusts and eliminating the step-up in basis rule. However, clients should keep these in mind, as they may be revived in the Senate’s version of a budget bill.

Importantly, the House bill is a mere proposal at this point. The situation continues to be fluid, and changes are expected as the bill moves through the legislative process. As a result, the final timing and content of the bill are unknown. The Senate Finance Committee will likely advance its own version of a bill, and both the Senate and the House will need to combine their respective bills to form one comprehensive package.

Conclusion

Tax planning should be addressed throughout the year and be an integral part of financial planning. If you have any questions feel free to reach out to Huckabee CPA for a free consultation and discuss how these tax change issues could impact your business and tax liability.