The TCJA tax code overhaul reform, that was signed Dec. 22, 2017, by President Donald Trump, took effect Jan. 1, 2018. Under the law (Pub. L. 115-97), the use of personal exemptions in calculating income tax liability was suspended from Jan. 1, 2018 to Jan. 1, 2026. The IRS revised the federal income tax withholding form and withholding methods in late 2019 to better conform with the new law. As a business owner did you used to enjoy working with withholding allowances to figure out an employee’s federal income tax withholding? Well that is changing.

The TCJA tax code overhaul reform, that was signed Dec. 22, 2017, by President Donald Trump, took effect Jan. 1, 2018. Under the law (Pub. L. 115-97), the use of personal exemptions in calculating income tax liability was suspended from Jan. 1, 2018 to Jan. 1, 2026. The IRS revised the federal income tax withholding form and withholding methods in late 2019 to better conform with the new law. As a business owner did you used to enjoy working with withholding allowances to figure out an employee’s federal income tax withholding? Well that is changing.

Starting Jan. 1, 2020, employers are required to use the new 2020 Form W-4, Employee’s Withholding Certificate, and withholding instructions in 2020 Publication 15-T, ‘‘Federal Income Tax Withholding Methods,’’ for new employees and those wishing to change their withholding. The 2020 Form W-4 requires employees to report dollar amounts instead of withholding allowances to calculate income tax.

The employer worksheets in Publication 15-T include instructions for determining withholding for 2020 Forms W-4 and for withholding forms issued before 2020 using the percentage-method tables for calculating federal income tax withholding and the wage-bracket method tables. The 2020 Form W-4 is the IRS’s second attempt at a revision. Bloomberg Tax published a whitepaper about the “New Form W-4 Withholdings in 2020 guide.” If you handle payroll by hand, it may seem intimidating to have to change up your payroll process. You will likely have a lot of questions.

The agency released a substantially revised draft Form W-4 in June 2018 that was to take effect in 2019, but updates were delayed to 2020 to incorporate comments from payroll professionals. Delayed implementation of the 2020 Form W-4 and withholding methods is not expected, a spokeswoman for the IRS told Bloomberg Tax Sept. 26, 2019. ‘‘If an employer’s automated system is not current, we suggest using the manual instructions provided in Publication 15-T.’’

Bloomberg’s white paper covers the multiple steps to be completed for the 2020 Form W-4, how to fill out the income withholding worksheets in Publication 15-T, withholding for nonresident alien employees, and issues related to states. A Forbes contributor Mike Kappel recently wrote an article about the changes titled “6 things to keep in mind about the 2020 W-4 Form” which summarizes the key points. Another interesting resource from Gusto titled “Here’s How to Fill Out the New W-4 Form for 2020.”

What the Form W-4 For 2020 Means For Your Business

The final version of the 2020 Form W-4, Employee’s Withholding Certificate, was issued Dec. 4, 2019. Employees filling out the form no longer are to be able to claim any withholding allowances.

Two early release drafts of the 2020 Form W-4 were issued by the IRS to allow payroll industry stakeholders to comment on revisions. The second revised draft, Form W-4, Employee’s Withholding Certificate, was released Aug. 8, 2019. The earlier version of the 2020 draft, released May 30, 2019, including the word ‘‘allowance’’ in the name of the form.

The form outlines five steps for reporting tax-filing status, whether household members hold multiple jobs, dollar amounts for other income that would not have withholding, and anticipated tax credits and deductions. The form also allows for additional withholding amounts to be applied to each pay period. General instructions and two half-page worksheets accompany the form. The worksheets are not to be filed with the employer.

You Might Have Different Versions Of Form W-4 On File

New hires and employees who need to adjust withholding are required to file the revised form starting Jan. 1, but employers must honor valid forms that are on file if changes are not needed. Employers may ask, but may not require, employees to replace existing forms, and may not treat employees with older forms as failing to submit a W-4.

The treatment of newly hired employees who do not file a valid Form W-4 depends on when wages first are paid, the IRS said Dec. 5.

New employees who are first paid wages in 2020 and do not file a valid form are to be withheld with a filing status of single with no adjustments on a 2020 Form W-4. This treatment includes employees hired in 2019 if the first payment occurs in January.

Employees who are first paid wages before 2020 and do not file a valid Form W-4 are to be withheld with a filing status of single and zero withholding allowances on a Form W-4 issued before 2020. An employee who is first withheld using the pre-2020 default withholding status may not be switched to the 2020 default withholding status.

Withholding Allowances Are Gone

Forbes contributor Mr. Kappel stated that “the thing that really separates the 2020 W-4 form from the 2019 and earlier forms is the elimination of withholding allowances.” By the IRS now taking away withholding allowances for employers came as a surprise. Employers have used withholding allowances to determine income tax withholding for years. If you are not totally familiar with withholding allowances, here is a quick summary from Mr. Kappel “withholding allowances are exemptions from federal income tax. The more allowances an employee claims, the less you withhold from their wages for federal income tax.” Say goodbye to the Personal Allowance Worksheet from page three of the old Form W-4 is now been removed.

Why? “This is because the TCJA eliminated personal exemptions. These exemptions allowed for deductions against a taxpayer’s personal income, which reduced their taxable income, and therefore, their federal income tax. These exemptions were tied to allowances, but since exemptions are now gone, the need to determine the number of allowances is gone too.” – said Caleb Newquist, editor-at-large Gusto.

“The information contained in lock-in letters is to change to reflect the 2020 Form W-4,” the IRS said.

Starting with lock-in letters sent in 2020 for employees who filed a 2020 Form W-4, employers are to withhold as if the employee is single and checked the box in Step 2c of Form W-4. If, after a lock-in letter is sent, the employee asks the IRS in 2020 for a different withholding rate, the specified rate is to be stated in terms of the information provided on the 2020 Form W-4.

The default lock-in letter in 2019 requires the employer to withhold as if the employee had the filing status of single and claimed zero allowances. Employers are to honor existing lock-in letters from 2019 and earlier unless they are replaced with a new letter.

Layout of 2020 Form W-4

The one-page Form W-4 is divided into five instructional sections:

- Step 1, Enter Personal Information, includes Steps 1a, 1b, and 1c;

- Step 2, Multiple Jobs or Spouse Works, includes Steps 2a, 2b, and 2c;

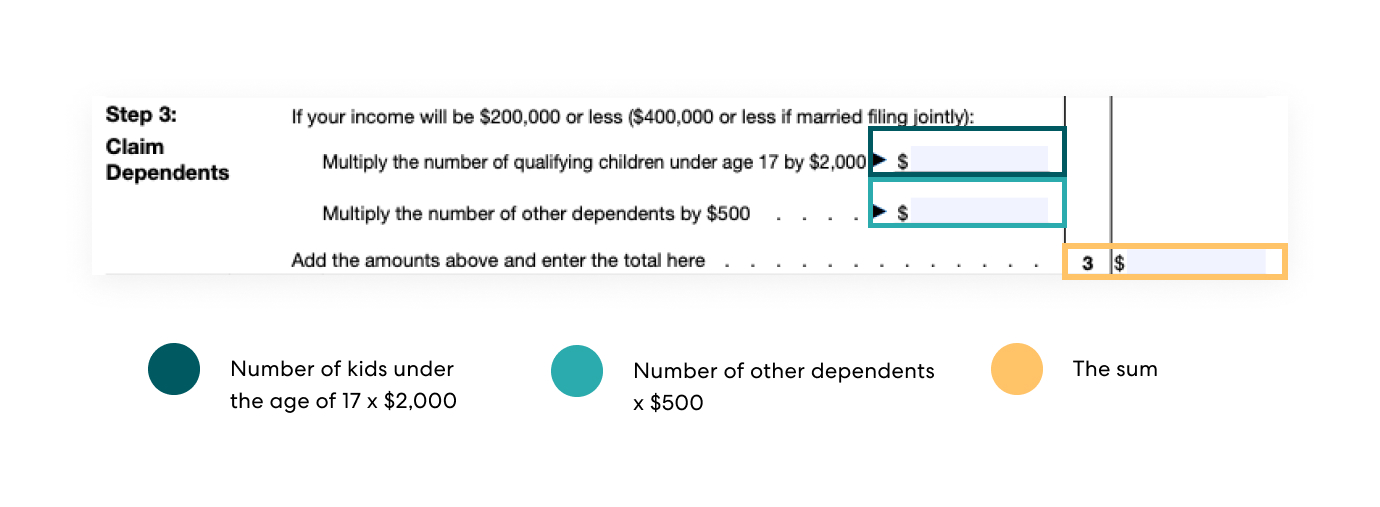

- Step 3, Claim Dependents;

- Step 4, Other Adjustments, includes Steps 4a, 4b, and 4c; and

- Step 5, a field for the employee’s signature and date.

Three fields for the employer’s name and address, the employee’s employment date, and the employer identification number are unnumbered.

The 2019 Form W-4’s Line 5 for the total number of allowances was replaced by Steps 3 and 4 for employees to indicate dollar amounts. Steps 2, 3, and 4 may be skipped if they do not apply to the employee.

All data fields on the 2019 form were renumbered on the 2020 form, though some retained the same purpose and similar wording. The following steps were revamped or renumbered on the 2020 form:

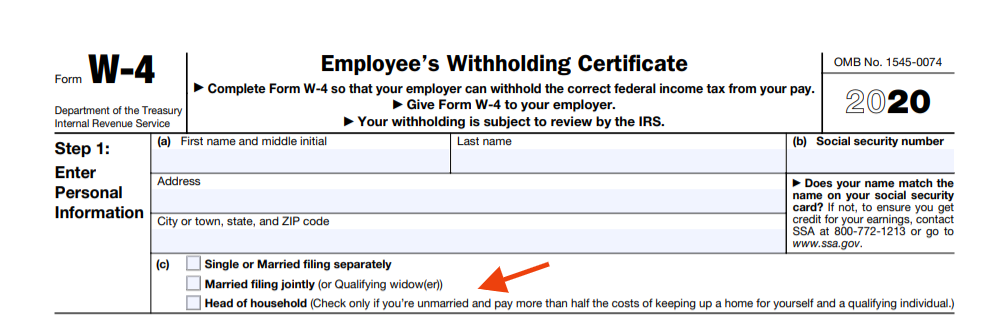

Step 1: The filing status ‘‘Married, but withhold at higher Single rate’’ was removed. A ‘‘head of household’’ status was added that may be selected by unmarried employees paying more than half the costs of maintaining a home that includes a qualifying individual.

Step 1: The filing status ‘‘Married, but withhold at higher Single rate’’ was removed. A ‘‘head of household’’ status was added that may be selected by unmarried employees paying more than half the costs of maintaining a home that includes a qualifying individual.

Line 4 on the 2019 form, used to indicate whether the employee’s name is different from what is shown on their Social Security card, was replaced with an unnumbered notice to contact the Social Security Administration about name and card mismatches.

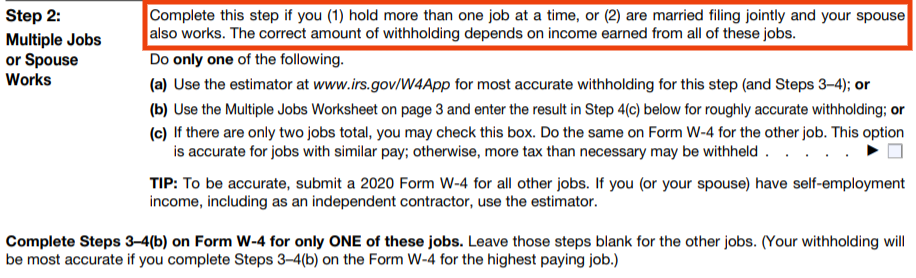

Step 2: Employees are to use this field if they work more than one job at the same time or are married filing jointly and their spouse also works. Employees are instructed to do one of the following: 2a, use the Tax Withholding Estimator for withholding guidance; 2b, use the Multiple Jobs Worksheet and enter additional withholding amounts on 4c; or 2c, check the box to request a higher withholding rate.

The instructions recommend that only employees with two jobs in their household check the box in Step 2c for both jobs. However, employees with one job in the household may check the box in Step 2c to increase withholding, the instructions said.

Employees with privacy concerns are encouraged to use the Step 2 options to avoid reporting amounts on Steps 4a and 4b.

Step 3: Employees enter the amount of tax credits that they expect to claim. This amount reduces the amount of tax withheld.

Step 3: Employees enter the amount of tax credits that they expect to claim. This amount reduces the amount of tax withheld.

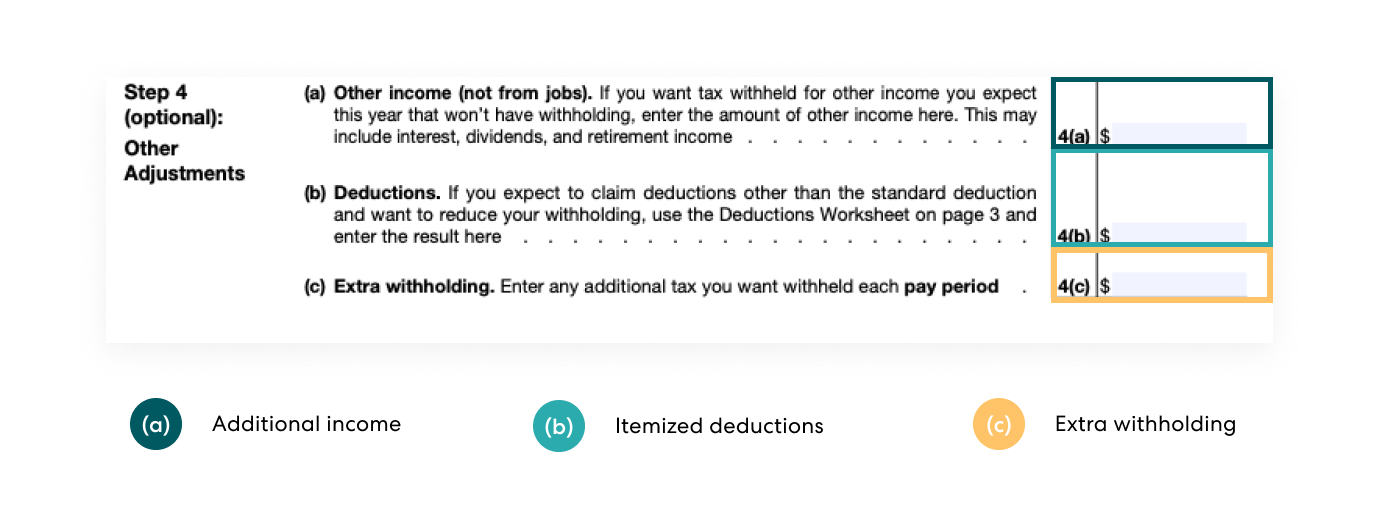

Step 4a: Employees enter the amount of other estimated income that does not come from a job. This amount increases the total amount of taxable wages.

Step 4a: Employees enter the amount of other estimated income that does not come from a job. This amount increases the total amount of taxable wages.

Step 4b: Employees enter the amount of deductions that they expect to claim other than the standard deduction. This amount reduces the total amount of taxable wages.

Step 4c: Employees enter any additional tax amount to be withheld each pay period. Step 4c replaced the 2019 form’s Line 6, and the wording of that field generally did not change. Employees only are to enter amounts on Steps 3, 4a, and 4b for one job in the household. The instructions recommend that these lines be completed for the highest-paying job to ensure more accurate withholding.

The draft form does not have a data field for employees to claim exemption from federal income tax withholding, which was Line 7 on the 2019 form. Employees are to fill out Step 1 and Step 5 and write ‘‘Exempt’’ in the space under Step 4c.

Employers providing electronic Forms W-4 are to create a field for employees to claim exempt from withholding. The field also must include language for employees to certify that they had no federal income tax liability in 2019 and expect to have no federal income tax liability in 2020.

Nonresident aliens are to check ‘‘single’’ and write ‘‘NRA’’ on the form under Step 4c. Further instructions are to be provided in Notice 1392, Supplemental Form W-4 Instructions for Nonresident Aliens.

Employers are to continue to provide a space on electronic Forms W-4 for NRA employees to claim withholding.

PUBLICATION 15-T

Three early-release drafts of Publication 15-T, ‘‘Federal Income Tax Withholding Methods,’’ were issued by the IRS. The latest draft was released Nov. 4, 2019.

The 24-page draft publication has five withholding worksheets for employers, includes information on revised percentage-method and wage-bracket method tables for calculating federal income tax withholding, and applies 2019 amounts to the formulas. The draft also includes withholding guidance regarding alternative methods, gaming distributions, and periodic pension and annuity payments.

The publication’s worksheets and tables show what the 2020 versions would look like using 2019 tax parameters.

Draft withholding tables and worksheets using inflation-adjusted amounts for 2020 were issued Nov. 28, 2019, as an attachment to the Nov. 4. draft of Publication 15-T. The tables, which are to be included in the finalized Publication 15-T, indicate that the value of a withholding allowance for 2020 is $4,300.

The automated percentage method is the only method that allows for withholding for 2019 forms and 2020 forms using one set of tables. The method also is the only one to require annualizing wages. The four-manual methods calculate tax based on wages paid for each pay period.

Methods for 2020 Forms

All withholding methods compatible with 2020 Forms W-4 include a fixed amount of wages exempt from withholding instead of allowance amounts based on the number of personal exemptions claimed by an employee.

The equivalent of zero, two, or three allowances is factored into Publication 15-T withholding methods for 2020 forms, depending on the employee’s filing status and whether the box in Step 2c is checked.

For Forms W-4 with the Step 2c box checked, the fixed amount is zero.

For Forms W-4 when the Step 2c box is not checked, an employee who selects the status ‘‘Married and Filing Jointly’’ has $12,900 annually subtracted from taxable wages (equivalent of three withholding allowances, 2020 figure); an employee selecting single or head of household has $8,600 subtracted from taxable wages (equivalent of two withholding allowances, 2020 figure).

Worksheet 1, the automated-percentage method, includes the fixed amount of exempt wages in the calculation of the annual adjusted wage amount. Worksheet 2, the wage-bracket method for 2020 forms, and Worksheet 4, the manual percentage method for 2020 forms, include the fixed amount of exempt wages in the formula that creates the withholding tables.

Withholding under 2020 forms also requires adjustments depending on amounts included in Steps 3, 4a, or 4b of Form W-4. On Worksheet 2 and Worksheet 4, other income amounts and deduction amounts are converted into pay period amounts from annual amounts. Tax credits are converted into pay period amounts on Worksheets 1, 2, and 4.

All methods for 2020 forms have a standard withholding rate schedule and a higher withholding rate schedule. The higher withholding schedule is to be used with 2020 Forms W-4 with the checkbox in Step 2c selected.

The tables for 2020 forms also contain schedules for those claiming head-of-household status.

Methods for 2019 Forms

Withholding allowances claimed on Forms W-4 issued before 2020 are to continue to apply unless a change is needed. Employers are to calculate withholding without needing to convert information provided on older forms into information requested on the revised W-4.

Each withholding method that may be used for forms issued before 2020 requires subtracting from wages the number of allowances claimed, multiplied by an allowance amount ($4,300 in 2020).

The wage-bracket method tables and manual percentage-method tables for older forms are to have the same structure as those in effect for 2019, with no changes to the calculation of the amount of tax to withhold.

INCOME WITHHOLDING METHODS

Publication 15-T includes five withholding worksheets for employers.

Worksheet 1

Percentage-Method Tables for Automated Payroll Systems

The percentage method for automated systems is the only worksheet that combines withholding using 2020 Forms W-4 and older forms. The amount of tax withheld is calculated based on adjusted annual wages.

Step 1: Adjust the employee’s wage amount

Lines 1a to 1c: Multiply taxable wages for the pay period by the number of pay periods in a year to estimate wages paid in a year.

For employees who have submitted a 2020 Form W-4:

Lines 1d and 1e: Add the amount of estimated other income, reported on Step 4a of the Form W-4, to the estimated annual wages calculated on the worksheet’s Line 1c.

Lines 1f to 1h: If the box in Step 2c of the Form W-4 is not checked, add the amount of deductions, reported on Step 4b, to the fixed amount of exempt wages. The fixed exemption amount is $12,900 (2020) if the employee is married filing jointly; the amount is $8,600 (2020) otherwise. If the employee checked Step 2c to be withheld at a higher rate, no amount is to be added to the deduction amount.

Line 1i: Subtract the result from the sum of other income and estimated annual wages to determine the adjusted annual wage amount.

For employees who have not submitted a 2020 Form W-4:

Lines 1j and 1k: Multiply the number of withholding allowances claimed by $4,300 (2020).

Line 1l: Subtract the result from estimated annual wages to determine the adjusted annual wage amount.

Step 2: Figure the tentative withholding amount

The automated percentage-method table’s standard withholding rate schedules are to be used with pre-2020 Forms W-4 and 2020 Forms W-4 that do not request higher withholding using the Step 2c checkbox.

The higher withholding rate schedules are to be used for employees that select the Step 2c checkbox.

Lines 2a to 2d: Find the row on the percentage-method table where the annual adjusted wage amount is at least the amount in Column A and less than the amount in Column B. Take into account the employee’s pay frequency, filing status, and whether the employee checked the box in Form W-4’s Step 2c.

Line 2e: Subtract the Column A amount from the adjusted annual wage amount.

Line 2f: Multiply the result by the percentage in Column D.

Line 2g: Add to the result the amount in Column C.

Line 2h: Divide by the number of pay periods to determine the tentative withholding amount.

Step 3: Account for tax credits

Lines 3a and 3b: If the employee reported potential tax credits on Step 3 of the 2020 Form W-4, divide that amount by the number of pay periods.

Line 3c: Subtract the result from the tentative withholding amount.

Step 4: Figure the final amount to withhold

Lines 4a and 4b: Add any additional withholding amounts reported on Step 4c of the 2020 Form W-4 and Line 6 of older Forms W-4 to the result on the worksheet’s Line 3c to determine the amount to be withheld from the employee each pay period.

Worksheet 2

Wage-Bracket Method Tables for Manual Payroll Systems With Forms W-4 From 2020 or Later

The amount of tax withheld is calculated based on adjusted pay-period wages.

Step 1: Adjust the employee’s wage amount

Lines 1a to 1d: Divide the amount of estimated other income, reported on Step 4a of the Form W-4, by the number of pay periods.

Line 1e: Add the resulting amount of other income per pay period to the employee’s total taxable wages for the pay period.

Lines 1f and 1g: Divide the amount of deductions, reported on Step 4b, by the number of pay periods.

Line 1h: Subtract the amount of deductions per pay period from the amount calculated on Line 1e. The result is the adjusted wage amount.

Step 2: Figure the tentative withholding amount

The wage-bracket method tables for 2020 Forms W-4 have individual columns for the three filing statuses. Each filing-status division has a column with tax Payroll Strategic White Papers 8 amounts under the standard withholding rate schedule and a column with tax amounts when the Form W-4’s Step 2c is checked.

Line 2a: Use the adjusted wage amount to look up the tentative withholding amount in the corresponding wage-bracket column, taking into account the employee’s pay frequency, and filing status, and whether the employee checked the box in Form W-4’s Step 2c.

Step 3: Account for tax credits

Lines 3a and 3b: If the employee reported potential tax credits on Step 3 of the 2020 Form W-4, divide the amount by the number of pay periods.

Line 3c: Subtract the result from the tentative withholding amount determined on Line 2a.

Step 4: Figure the final amount to withhold

Lines 4a and 4b: Add any other withholding amounts reported on Step 4c of the 2020 Form W-4 to the result on Line 3c of the worksheet to determine the amount to be withheld from the employee each pay period.

Worksheet 3

Wage-Bracket Method Tables for Manual Payroll Systems With Forms W-4 From 2019 or Earlier

The amount of tax withheld is calculated based on adjusted pay-period wages. The wage-bracket tables for forms issued before 2020 have columns for the number of withholding allowances claimed.

Step 1: Figure the tentative withholding amount

Lines 1a and 1b: Use the total wages for the pay period and the number of allowances claimed to look up the tentative withholding amount, taking into account the employee’s filing status and pay frequency.

Step 2: Figure the final amount to withhold

Lines 2a and 2b: To determine the amount to be withheld from the employee each pay period, add additional withholding amounts, reported on Line 6 of pre2020 Forms W-4.

Worksheet 4

Percentage-Method Tables for Manual Payroll Systems With Forms W-4 From 2020 or Later

The amount of tax withheld is calculated based on adjusted pay-period wages.

Step 1: Adjust the employee’s wage amount

Lines 1a to 1d: Divide the amount of estimated other income, reported on Step 4a of the Form W-4, by the number of pay periods.

Line 1e: Add the resulting amount of other income per pay period to the employee’s total taxable wages for the pay period.

Lines 1f and 1g: Divide the amount of deductions, reported on Step 4b, by the number of pay periods.

Line 1h: Subtract the amount of deductions per pay period from the amount calculated on Line 1e. The result is the adjusted wage amount.

Step 2: Figure the tentative withholding amount

The manual percentage-method table’s standard withholding rate schedules are to be used with 2020 Forms W-4 that do not request higher withholding using the Step 2c checkbox. The higher withholding rate schedules are to be used for employees that select the Step 2c check box.

Lines 2a to 2c: Find the row on the percentage-method table where the adjusted wage amount is at least the amount in Column A and less than the amount in Column B. Take into account the employee’s pay frequency and filing status, and whether the employee checked the box in Form W-4’s Step 2c.

Line 2d: Subtract the Column A amount from the adjusted wage amount.

Line 2e: Multiply the result by the percentage in Column D.

Line 2f: Add to the result to the amount in Column C to determine the tentative withholding amount.

Step 3, account for tax credits

Lines 3a and 3b: If the employee reported potential tax credits on Step 3 of the 2020 Form W-4, divide the amount by the number of pay periods.

Line 3c: Subtract the result from the tentative withholding amount.

Step 4: Figure the final amount to withhold

Lines 4a and 4b: Add any additional withholding amounts reported on Step 4c of the 2020 Form W-4 to the result to the result on the worksheet’s Line 3c to determine the amount to be withheld from the employee each pay period.

Worksheet 5

Percentage-Method Tables for Manual Payroll Systems With Forms W-4 From 2019 or Earlier

The amount of tax withheld is calculated based on adjusted pay-period wages.

Step 1: Adjust the employee’s wage amount Lines

1a to 1c: Multiply the number of allowances claimed by the amount listed in the worksheet’s Table 6.

Line 1d: Subtract the result from the employee’s pay period wages to determine the adjusted wage amount.

Step 2: Figure the tentative withholding amount

Lines 2a to 2c: Find the row on the percentage-method table where the adjusted wage amount is at least the amount in Column A and less than the amount in Column B. Take into account the employee’s pay frequency and filing status.

Line 2d: Subtract the Column A amount from the adjusted wage amount.

Line 2e: Multiply the result by the percentage in Column D.

Line 2f: Add to the result the amount in Column C to determine the tentative withholding amount.

Step 3: Figure the final amount to withhold

Lines 3a and 3b: To determine the amount to be withheld from the employee each pay period, add any additional withholding amounts, reported on Line 6 of pre-2020 Forms W-4.

Withholding for Nonresident Alien Employees

Publication 15-T contains instructions for withholding taxes on nonresident alien employee income. The amount of federal income tax to withhold applies to nonresident aliens performing services in the U.S. who have wages subject to withholding.

To calculate withholding, employers must determine if a nonresident alien employee submitted Form W-4 from 2020 or from an earlier tax year. Employers then add to the wages paid to the employee for the pay period the additional amount shown in the accompanying tables for the corresponding payroll period.

The draft publication sets additional amounts using 2019 tax parameters for Forms W-4 submitted for 2020 and later. The additional weekly amount is $234.60, the biweekly amount is $461.50, and the daily amount is $46.90. For Forms W-4 submitted before 2020, the additional amounts are $153.80 for a weekly payroll period, $307.70 for biweekly, $30.80 for the daily amount. Rounding to the nearest dollar is allowed.

The method for nonresident alien employees does not apply to supplemental wage payments if the 22% optional flat-rate withholding is used to calculate withholding or the 37% mandatory flat-rate withholding method was applied on supplemental pay.

Under the U.S.-India income tax treaty, nonresident alien students from India and business apprentices are not subject to the withholding adjustment procedure.

Conclusion

For some small businesses, this might be a bit of a learning curve to get used to.

Most managers or HR people won’t become overnight experts on the new W-4 form or the new process for income tax withholding. And that’s OK—there’s a definite learning curve with new things like this.

Don’t freak out if you’re initially confused. It takes time and repeated research to get to know the changes like the back of your hand.

So just realize that there’s a learning curve for these Form W-4 changes. And if you’re still stressed and confused and are the San Diego area feel free to contact Huckabee CPA for a free consultation. Just an FYI we don’t always do payroll separately for small business but can handle payroll services as a piece of our accounting, tax and CFO packages.