The Economic Recovery of 2021 is Underway. But its a little Different this Time Around

The WSJ recently reported that The U.S. economic recovery is unlike any in recent history, powered by consumers with trillions in extra savings, businesses eager to hire and enormous policy support. Companies and workers are much better positioned to emerge from this downturn with far less permanent damage than occurred after recent recessions, particularly the 2007-09 financial crisis.

Why is this economic recovery different?

The journal points out that during this past year and half of the Covid-19 health crisis, households saved cash and banks amassed capital, but supply shortages are popping up and some employers can’t find workers who want to do the job.

According to another WSJ article, investor deal flow and business valuations are reaching new heights in technology startups, as a flood of cheap cash fuels efforts to find the industry’s next big startup company winners.

The velocity of which workers have been quitting their jobs during this past year, (which happens to be a proxy for confidence in the labor market) is now equal to the peak time period of the year 2000. And according to the WSJ article, “American household debt-service burdens, as a share of after-tax income, are near their lowest levels since 1980, when records began.” And if look at the Dow Jones Industrial Average is up nearly 18% from its pre-pandemic peak in February 2020. Home prices across the U.S. are up nearly 14% higher, since then.

The speed of this economic rebound is also triggering chaos. The shortages of goods, raw materials and labor that typically happen toward the end of an expansion are cropping up much sooner. Many economists, along with the Federal Reserve, expect the jump in inflation to be temporary, but others worry it could persist even once reopening is complete.

According to a recent NYT’s article reporting the U.S. unemployment is still high, but companies are complaining they can’t find enough workers. Prices are shooting up for some goods and services, but not for others. Supply-chain bottlenecks are making it hard for homebuilders, automakers and other manufacturers to get the materials they need to ramp up production. A variety of indicators that normally move more or less together are right now telling vastly different stories about the state of the economy.

(image credit: NYT)

Allen Sinai, chief global economist and strategist at Decision Economics, Inc told the journal “We’ve never had anything like it—a collapse and then a boom-like pickup,” and he further iterated “it is without historical parallel.”

When Covid-19 pandemic restrictions sent the U.S. economy into free fall last March, economists and policy makers worried it would take years for workers and businesses to heal. They now expect the economy’s size to surpass pre-pandemic levels this quarter. Analysts project that by the end of this year GDP will reach 6.5 percent.

The turn in fortunes has been hectic for a lot of businesses. As the economy is starting to open up again some restaurants, travel, and hospitality industries are having issues with finding workers to hire to keep up with the sudden onslaught of business after months of struggle due to pandemic-triggered shutdowns.

A sustained rebound isn’t assured, suggested by the slowing improvement of many economic measures in April. And a resurgence of Covid-19 in the U.S. could derail it entirely.

Nonetheless, economists point to four key ways the current recovery differs from its predecessors:

Natural Disaster vs Financial Crisis

(image credit: CNN)

Previously the past few recession downturn cycles typically resulted from a rise in interest rates or a decline in asset values that hurt output, income and employment, sometimes for more than a year. The damage to household finances and financial institutions after the 2007 housing crash led to lost demand that weighed on the economy for years.

But this Covid-19 health crisis recession, by comparison, didn’t result from financial factors, but from a disruption similar to a natural disaster. Gail Fosler, an economist and president of The GailFosler Group LLC told the journal “the pandemic created a shock that overwhelms the very concept of an economic cycle.”

Natural disasters temporarily interrupt economic activity while leaving intact the underlying demand and supply of goods and services. Once the disaster passes, the economy recovers faster than with a typical recession. The WSJ pointed to a 2018 study of individual tax returns of New Orleans residents, which had revealed that after a large, initial blow from Hurricane Katrina, victims’ incomes bounced back within a few years and even surpassed those of unaffected earners.

Typically during past recessionary downturns, consumers are sometimes nervous about getting laid off or having less income, and will often cut back on spending, which has an amplifying effect on the slump. This time, consumer spending in areas unaffected by lockdowns such as autos barely flagged, and to the extent that some consumers did hold back, it was more out of fear of the virus than fear of losing their jobs, a U.S. Census survey conducted throughout the pandemic suggests.

The Biden Administration’s rollout of the vaccines is containing the natural disaster by allowing consumers to spend more and businesses to reopen. In recent months, restaurant spending by vaccinated people has grown faster than that of the unvaccinated, according to market-research firm Cardify.ai.

As more people get vaccinated, hiring is picking up. Analysis of census data by Aaron Sojourner, a labor economist at the University of Minnesota Carlson School of Management, found that for every 100 working-age people vaccinated, 12 are becoming newly employed, on average.

There is a consumer confidence and a boldness now, as are entering post-vaccination world, that wasn’t there last year.

According to the reporting from the journal, usually in the months or years after a recession, the labor market remains slack as job seekers vastly outnumber job openings. High unemployment and weak wage growth hinder consumer spending and discourage businesses from expanding. The longer it takes for spending to rebound, the greater the risk that businesses will fold and workers will leave the labor force, taking with them the human and organizational capital needed to restore growth.

But currently the economy appears to be dodging that vicious cycle. Stephanie Aaronson, an economist at the Brookings Institution said “the fact that it has recovered so quickly has limited the scope for a lot of scarring relative to, say, in the Great Recession.”

Monetary and fiscal policy

The coronavirus brought about a larger and faster monetary and fiscal response than in any previous recession, limiting damage to the economic system and setting the stage for a faster recovery.

The Federal Reserve cut rates, initiated large-scale bond purchases and outlined a new commitment to keeping interest rates near zero until full employment had returned and inflation was headed above its 2% target. Officials say that rates may not rise until 2024. The Fed’s balance sheet surged from $4.2 trillion in early March of 2020 to nearly $7.1 trillion by late May; the increase was less than $1.3 trillion during the previous recession.

Congress acted faster than in previous downturns. It shored up business and household balance sheets through multiple rounds of stimulus payments, expanded unemployment benefits and the Paycheck Protection Program. Congress’s fiscal response to the Covid-19 pandemic will amount to $5.1 trillion, or 4.4% of gross domestic product through 2024, according to the Committee for a Responsible Federal Budget. By comparison, stimulus legislation enacted in the wake of the 2007-09 recession cost roughly $1.8 trillion, or 2.4% of GDP between 2008 and 2012.

The difference this time around is that household incomes are up substantially from pre-pandemic levels, especially for lower-earning families.

James Knightley, chief international economist at ING explained “this is very different to any previous recession, consequently, we have got a situation where household balance sheets are very strong and this can fuel sentiment and spending for quite some time.”

Republicans and some economists also argue the $300 unemployment top-off is deterring workers from going back to get new jobs. The fiscal measures have shattered the usual link between employment on the one hand, and incomes and spending on the other.

Healthier households and businesses

Karen Dynan, an economics professor at Harvard University, “often recessions happen because of some sort of imbalance—we have too much housing or too much debt or too much inflation.” When those imbalances start to reverse, the damage to the economy can build on itself. Households and businesses will usually rein in spending, which in turn depresses others’ incomes and leads to further cutbacks. But few such imbalances existed when the pandemic hit, and fiscal and monetary support staved off broader damage. Households, banks and businesses are emerging in much sounder shape than after previous recessions.

Saving often rises when recessions hit, as worried households forego purchases and cling to cash, but never this much. Americans were saving at an annualized rate of $2.8 trillion in April—more than double before the crisis, positioning them to spend lavishly as the economy reopens. That compares with a rate of $734 billion in June 2009, or about $909 billion in 2021 dollars.

While federal relief contributed to some of the surge, so did business restrictions that prevented spending on many services. Higher-wage Americans, who were shielded from the pandemic’s labor-market hit because they are more likely to work remotely, were able to accumulate savings.

A surge in startups signals growing confidence among businesses—even amid a wave of small business closures. Filings to start new firms among a subset of owners who tend to employ other workers exceeded 830,000 through early May, a 21% increase over the same period in 2006, the next-highest year.

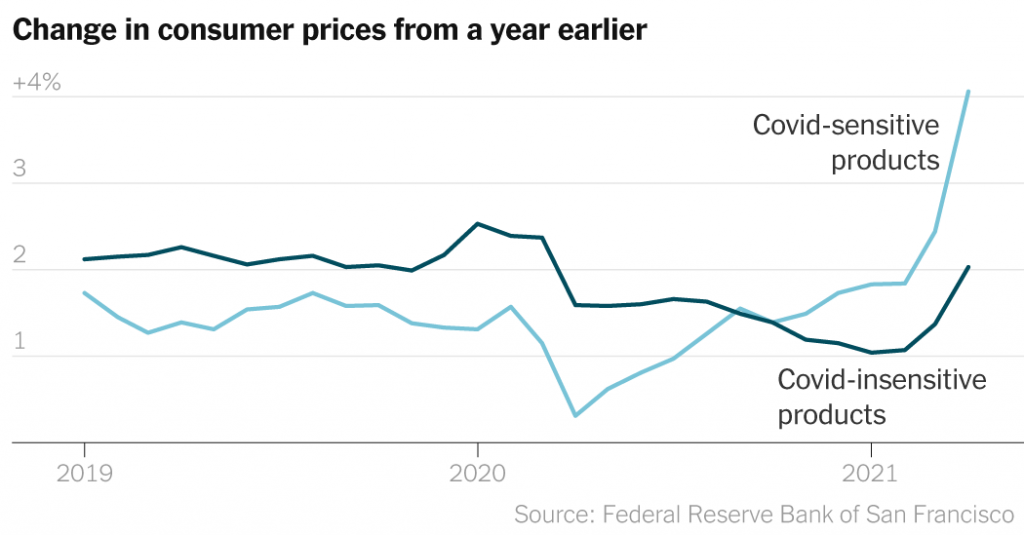

Shortages, bottlenecks, inflationary risks

One of the downsides of the fast recovery is that demand is bouncing back faster than supply can keep up, triggering bottlenecks and wage-and-price pressures that normally emerge years into an economic recovery.

Inflation often falls in recessions and early in recoveries, then slowly picks up as the expansion ages. This time, it is rebounding as the economy reopens. Consumer prices excluding food and energy soared 0.9% from March to April, the sharpest one-month increase since 1982.

The Fed will also be closely eyeing job growth, which was much slower-than-expected in April. Some economists are saying that lack of child care, fear of the virus and extra unemployment insurance are keeping many workers on the sidelines.

Currently employers who are seeking to hire face a relatively small pool of available workers. Millions of people who had jobs before the pandemic aren’t even looking for work.

Conclusion

The most important thing is that recovery has clearly begun, all signs showing it, and gathering momentum. Sure, it will be uneven for a while, with hiccups. Perhaps , this is the first time in a long time, the nation has gone through such a devastating experience, a new experience. Another positive thing is how this will present with new learning experience in dealing/facing the future challenges.

{kind=link}