The Impact of Tax Reform on Choice of Business Entity Selection

Risks and rewards in a ‘C corporation versus flow-through entity’ business decision

One of the most significant outcomes of the Tax Cuts and Jobs Act (TCJA) reform is the startling difference between the new tax rates for C corporations and for pass-through entity business income. For tax purposes, the decision on whether to operate as a “flow-through entity” (generally, a sole proprietorship and a schedule C filer, partnership, or S corporation) or as a C corporation is often referred to as a “choice-of-entity” determination.

One of the most significant outcomes of the Tax Cuts and Jobs Act (TCJA) reform is the startling difference between the new tax rates for C corporations and for pass-through entity business income. For tax purposes, the decision on whether to operate as a “flow-through entity” (generally, a sole proprietorship and a schedule C filer, partnership, or S corporation) or as a C corporation is often referred to as a “choice-of-entity” determination.

While entity choice isn’t just about tax rates, the rate changes are drastic enough to prompt many “pass-through” business owners to consider a conversion to a C corporation. While the new 21 percent corporate rate may favor the C corporation as a choice-of-entity for certain businesses, there are other factors, both tax and non-tax, to consider when making the determination. As a result, many businesses may decide to stay in flow-through form, rather than change to corporate.

This article will model several comparisons between Flow-Through Entities (FTE) and C corporation treatment with a focus on the following important considerations:

- Rate differences factoring in participation in the business, earnings distributed, and eligibility for the 20% deduction

- The potential sale of the business

- State tax differences

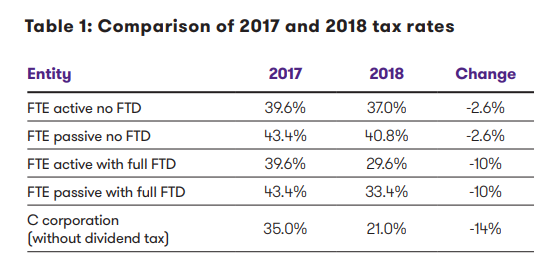

This is hardly the first time legislative changes have moved the needle on entity choice. In a 2013 article, The Impact of Tax Legislation on Choice of Entity, Grant Thornton LLP analyzed how the increase in the top tax rates on individuals and corporate dividends affected a comparison of the tax burdens faced by C corporations and flow-through entities (FTEs). The changes made in the TCJA affecting this choice are much more significant. C corporation tax rates have been reduced from 35% to 21%, while the top tax rate on individuals has only been reduced from 39.6% to 37%. Qualifying FTE owners can use a 199A 20% “pass thru” deduction.

Availability of the New Section 199A 20 Percent Deduction

When they passed the Act, Congress felt that some benefit needed to be provided for flow-through entities to, in a sense, offset the benefit that was provided corporations with the reduction in the tax rate. Therefore, Congress passed a new 20 percent deduction for qualified business income (the “20 percent QBI deduction”) earned by flow-through businesses to reduce the tax liabilities of the owners. Our recent article, “The New 20 Percent Deduction for Pass-Through Businesses,” provides a detailed discussion of this new deduction. Generally though, provided that certain tests are met (subject to many limitations, discussed below), the 20 percent QBI deduction can lower the effective tax rate paid by the active owners of flow-through businesses from a high of 40.8 percent to a low of 29.6 percent for certain business income (assuming the highest federal income tax rates and depending on whether the 3.8 percent tax on net investment income applies). Since these levels of taxation would often be lower than the effective rate of 39.8 percent paid on this same business income by a C corporation and its shareholders, this new 20 percent QBI deduction may encourage eligible businesses to stay in the flow-through form, although the deduction and the reduced rate for individuals is currently slated to “sunset” after 2025. While the C corporation rate cut is permanent. Without any complicating factors, the 21% rate on business income for a C corporation is a compelling reason to consider an entity change. That level of cash flow from tax savings each year is a very powerful tool to enable a business to stay competitive with other C corporations in its industry and to fund future growth.

|

Entity Choice Federal Tax Rates |

||

|

Tax Rate Comparisons |

Prior Law |

Act |

|

C corporation shareholder |

50.47% |

39.8% |

|

Active flow-through owner with no 20 percent pass-through deductions |

39.6% |

37.0% |

|

Passive flow-through owner with no 20 percent deduction |

43.4% |

40.8% |

|

Active flow-through owner with 20 percent pass-through deduction |

N/A |

29.6% |

|

Passive flow-through owner with 20 percent pass-through deductions |

N/A |

33.4% |

(Note in this chart: Calculations assume the highest federal tax rates apply and all of a corporation’s after-tax earnings are distributed to shareholders by way of taxable dividends subject to the 3.8 percent net investment income tax. State income taxes are ignored)

But the analysis of entity choice from a tax perspective is not so simple. There are many tax considerations beyond simply a comparison of rates. For example, a comparison of rates must factor in the ability of pass-throughs to distribute earnings tax-free.

Rate differentials on taxable income

Rate differentials on taxable income

The modeling exercise starts with an understanding of what income tax rates should be used. Before tax reform, rate differentials typically were displayed in a three-column comparison — C corporation rates and both “active” and “passive” FTE income rates because of the 3.8% net investment tax on passive income.

The TCJA has added a fourth and fifth column to this comparison. FTE rates now also depend on whether the owner’s business qualifies for the special deduction allowed for certain pass-through income. This special deduction gives FTEs a portion of the rate reduction given to C corporations, so FTE active and passive income qualifying for this deduction form the fourth and fifth comparisons. The actual amount of the 20% FTE deduction, can be somewhere between zero and 20% due to limitations we will describe below. Only U.S.-source qualifying income is eligible for the FTE deduction. For the purpose of simplification, Table 1 shows the TCJA rates assuming no limitations apply. Hereafter, the FTE deduction is abbreviated as FTD. Entities qualifying for the full FTD, are abbreviated as FTED.

Qualifying for the pass-through deduction

The 20% pass-through deduction is available for most income from qualified trades or businesses, including rent, but not for most investment income like capital gains, dividends and interest. The deduction is also subject to important limits and is not available on income from certain service businesses unless a taxpayer falls under certain taxable income thresholds.

Service businesses disqualified for the deduction are those defined as in the following industries: health, law, accounting, actuarial science, performing arts, consulting, athletics, financial services, brokerage services, investing and investment management (including trading, or dealing in securities, partnership interests or commodities), or any trade of business where the principal asset is the reputation or skill of one or more of its employees or owners. Architects and engineers are exceptions and do qualify for the deduction. The deduction is limited to the greater of either:

- (1) 50% of the owner’s allocable share of W-2 wages paid by the business,

- or (2) 25% of that W-2 wages share plus 2.5% of the original cost basis of qualified property (unless taxable income is below certain thresholds).

Once passing the threshold of owning a qualified business, business owners of FTEs should model the deduction limitation tests to determine if the deduction applies.

The tests can present challenges for owners who have kept operations and real estate in separate entities for liability shield purposes because it is not clear whether the tests can be applied across entities. In this case, businesses with real estate income or wage expenses segregated may need to consider planning actions to fix the problem. Combining entities can sometimes be helpful, but this must be weighed against non-tax considerations.

Factoring in distributions

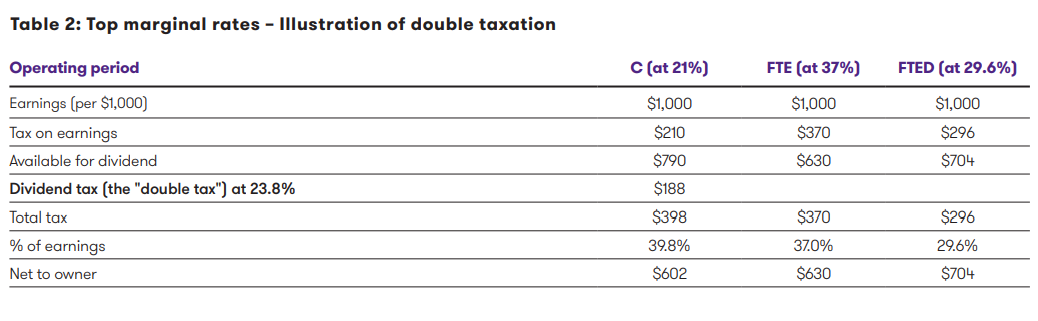

The rate comparison is not complete without factoring in the difference in tax treatment of distributions made by FTEs and C corporations. With a few rare exceptions, owners of C corporations pay tax on the dividends received from the company, while (again, with rare exceptions) owners of FTEs do not pay tax on distributions of earnings. FTEs routinely make distributions to owners to cover the tax on the FTE’s income. But if a certain business plans to distribute additional earnings, rather than use them for growth investments or to reduce debt, being an FTE can have a significant rate advantage. Table 2 shows the difference in total tax burden if all after-tax earnings are distributed.

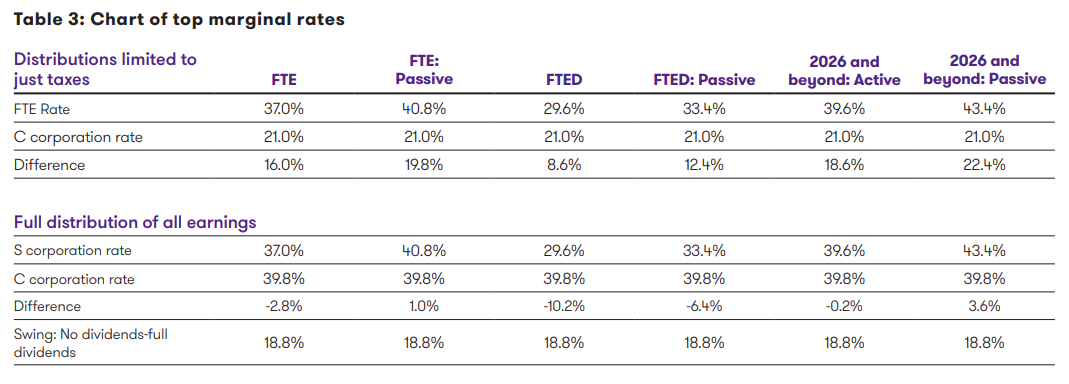

Of course, the result will depend heavily on the amount of earnings distributed. Table 3 below illustrates the wide disparity of rates, depending on how much cash the business retains and how much is distributed.

A company with active owners, in a business that qualifies for the FTD, retaining its cash to grow and reduce debt, making $10,000,000 per year in taxable income, will save $860,000 per year as a C corporation compared to an FTE with active owners (the savings increases to $1,980,000 per year for passive owners), certainly a reason to consider converting to C corporation status. On the other hand, companies paying generous dividends may still be ahead in FTE form.

Taking dividends out of the picture

While Table 3 shows a range of 8.6% to 19.8% savings in tax rates for C corporations if an owner retains all after-tax cash (forgoing dividends), that savings today will be offset by additional cost tomorrow when the owner of a FTE can afford to pay dividends tax-free, or when he or she sells the company and can take out all the undistributed earnings prior to sale tax-free (or reduce his or her gain on sale, effectively getting tax-free distribution of sale proceeds).

But what if an owner never plans to pay dividends, never plans to sell the business, and expects to die owning it? Are the income tax savings permanent? If the owner can confidently say these three conditions are facts, switching to a C corporation will permanently save income taxes. But an owner will generally get a better result by selling a business before death, (selling at the top of his or her career as an owner/manager, eliminating risk from post-retirement CEO(s)), or giving as much as he or she can to heirs before then because the income tax saved in a C corporation solution before the owner’s passing will likely be dwarfed by the estate tax engendered by this strategy.

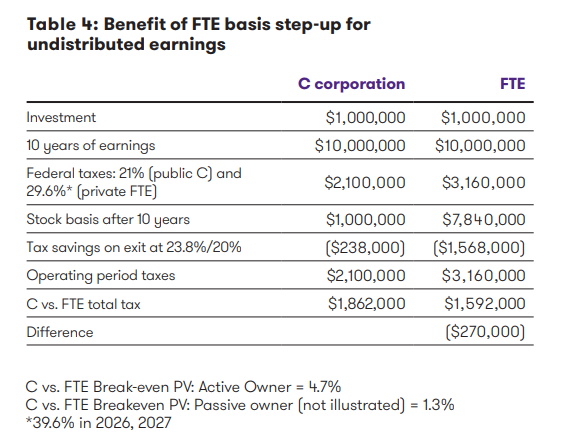

Table 4 provides an example of how the after-tax cash flow compares in a C corporation versus an FTE for a business started in 2018, owned for 10 years, and then sold. The example assumes the FTE qualifies for the FTD, has active ownership and only makes tax distributions:

Note that the FTE pays less total tax, from operations and the sale combined ($270,000), but the overall tax savings is really a tax cost of $86,000 per year ($186,000 in 2026-7), followed by a big tax savings of $1,330,000 in the year of sale from the basis increase.

The savings each year as a C corporation are eliminated by the savings in the year of sale by the FTE from the basis increase. But applying the time value of money to the equation, we can calculate the break-even point of today’s lower tax (C corporation) versus tomorrow’s tax savings (FTE). The breakeven present value (PV) discount rate is 4.7% for active owners. The break-even PV discount rate is reduced to 1.3% for passive owners. This modeling would imply that the immediate benefit of lower C corporation rates may be reduced or eliminated by the benefits of higher basis down the road if plans are to sell the business at some point, or simply to distribute built-up cash as dividends down the road.

One note of caution – the reversion of FTE rates to 39.6% and the elimination of the FTD (both in 2026), makes a significant difference in this calculation. The longer the model continues, the more a C corporation status is favorable. A business owner may want to model alternate scenarios illustrating (1) the 20% FTD and the 37% rate being retained by Congress, or (2) both provisions sunsetting as currently scheduled. Last, as owners consider switching from FTE to C, and holding cash to avoid double taxation, they should be reminded of some old provisions that may be making a comeback. The accumulated earnings tax, the personal holding company tax, rules on unreasonable compensation, and other statutes, regulations and case law that grew from pre-Tax Reform Act of 1986 owner behavior where owners of C corporations used their companies like the family piggy bank. As you consider moving to C corporation status, remember these rules are still on the books.

Selling the business

The FTE advantage of avoiding double taxation on distributions is important, but the FTE advantages when the business is sold can be even more compelling. This is demonstrated by how these benefits arise and how they have changed with the TCJA.

The principal benefits are twofold: first, the owner’s basis step-up from undistributed earnings described above, and second, from the owner being able to sell assets, giving the buyer a step-up in basis while the FTE owner still enjoys capital gains treatment on almost all of the proceeds.

Most buyers prefer to acquire businesses in a manner that steps-up the assets of the business acquired, either in an asset purchase, or one of the many forms of “deemed” asset purchases.

Acquiring a business in a transaction that qualifies for a step-up allows the buyer to record the assets at fair market value and recover the stepped-up basis through depreciation or amortization. Further, now that bonus depreciation is 100% and applies to used property, buyers can immediately expense many tangible assets in an acquisition.

If the buyer pays a premium over the tax basis of the assets, the premium will typically be allocated based on an appraisal. Our experience in dealing with purchase price allocation appraisals is that for profitable businesses, the preponderance of the resulting gain to the seller is capital gain, albeit the allocation does result in some ordinary income.

While the benefit of the buyer’s future tax deductions associated with the step-up in basis is technically the present value of the deductions for all of the assets (and should be carefully calculated in the context of a deal in process), for estimate purposes, treating the entire step-up as having a 15-year life (the tax life used for intangibles) allows the seller to quickly understand the value to the buyer. The formula for estimating the value is simple: using a 10% discount rate, a dollar of step-up results in a present value benefit of 13 cents (or 13% of the step-up) to the buyer (this present value benefit was 20% before the enactment of the TCJA). This amount assumes a C corporation buyer saving 26% (21% federal, 5% state) of each year’s amortization deductions for 15 years.

The ability for buyers to expense the full value of purchased tangible assets that qualify for bonus depreciation changes this math. Based on transactions and planning we have done since the enactment of the TCJA, the expensing of acquired machinery and equipment, and other tangible fixed assets, has enhanced the PV benefit to about 14% from 13%, based on the relative values of the goodwill step-up to the machinery and equipment (M&E) expensed in the cases we have reviewed.

This additional value created by the PV of future tax savings from goodwill amortization and M&E expensing increases the amount the buyer can afford to pay for the company. How much of this value will be captured by the seller in a higher sales price will depend upon negotiation. For the purposes of this analysis, it is assumed that the buyer and seller split the additional value, with 7% of the additional value (roughly one-half) accruing to the benefit of the seller.

Stock and asset sales

Theoretically, this additional value created from the sale of assets rather than the sale of stock can be created whether the business sold is a C corporation or an FTE. However, as we will learn below, C corporations selling assets is almost always too costly from a tax perspective, generally meaning C corporate owners are limited to selling stock, while FTE owners can capture this extra benefit in an asset sale (or deemed asset sale).

Properly structured, the assets of FTEs can be sold so that the buyer gets the valuable step-up, while the seller enjoys capital gains taxation on most of the sales proceeds, just as if stock had been sold. Generally, ordinary income will be recognized to the extent of depreciation recapture and any inventory gain (however, see discussion below regarding new ordinary income assets from changes in the TCJA). Last, the liquidation of the FTE is generally a tax-free event (except “old” C corporations that made S elections may have gains to the extent of C corporation E&P not distributed before the S election).

In contrast, the sale of assets by a C corporation will trigger a first level of tax at the corporate level and a second level of capital gains tax on liquidation. This additional tax burden to the seller will usually exceed the after-tax benefit to the purchaser, meaning most C corporation owners will sell stock, not assets.

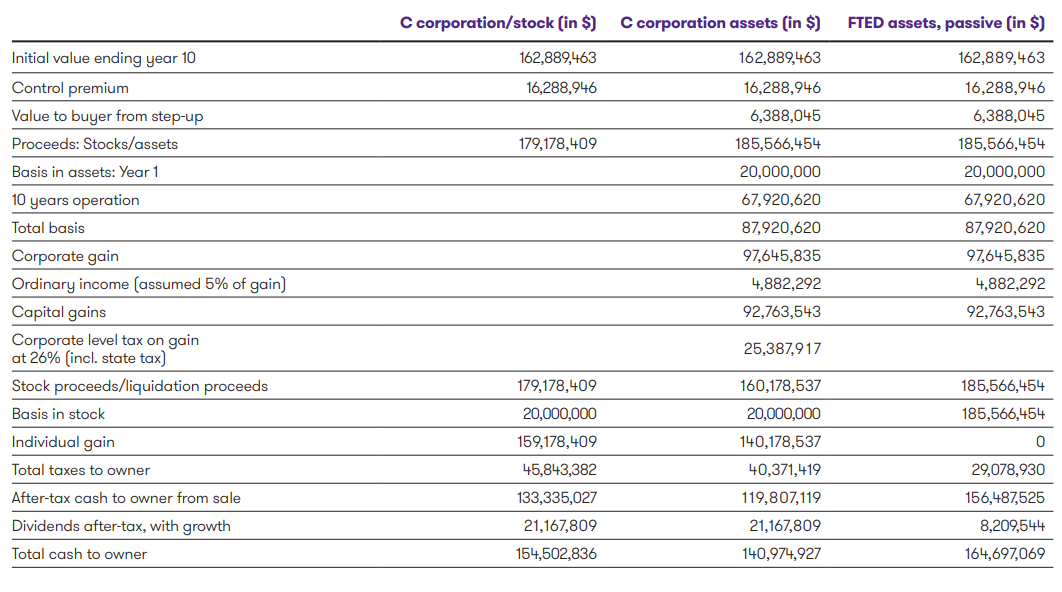

Table 5 demonstrates this effect. Assume two identical corporations had a tax basis in hard assets of $20 million and a business enterprise value of $100 million and pre-tax earnings of $10 million in 2018. One company makes an S corporation election in 2018, and the other one continues on as a C corporation. Over the next 10 years, the company’s value and earnings appreciate at 5% per year, and the company requires retention of 54% of pre-tax cash flow to achieve this growth. At the end of 2027, the company is approached with a buyout offer of its appreciated value (plus a 10% control premium) of $179 million for stock, or $186 million for assets, splitting the step-up value of $13 million equally with the seller.

Table 5 shows that, during the operating period, with a pre-tax free cash flow of 46%, and assuming a 4% growth rate on the owner’s savings, the C corporation owner will accumulate $21 million in cash from the dividends. This accumulation results from annual dividends of 20% (46% free cash flow, less 26% in federal and state tax). The passive owner of a business qualifying for the FTD accumulates $8 million, his effective tax rate being 38.4% (48.4% in 2026-7). But in contrast to this $13 million cash deficit, the sale of the business yields the a passive owner of a FTED a $23 million advantage over the sale of stock of the C corporation, due to a higher price, and the stepped-up stock basis for all the undistributed earnings. Selling assets of the C corporation, while commanding a higher price, yields $37 million less after-tax cash due to the effects of double taxation – tax on the gain on the sale plus tax on the gain on liquidation.

Remember, the further out you model a sale, the less valuable the tax attributes from FTE/FTED status outlined above become

Potential additional ordinary income from the sale of intangibles The tax cost to the seller of an FTE that is selling assets has gone up for certain businesses as a result of tax reform. While the sale of purchased intangibles continues to qualify for capital gains treatment (subject to recapture of prior amortization as ordinary income), companies enjoying the benefits of self-created patents, models, designs, secret processes or formulas, copyrights, and other related intangibles may be subject to ordinary income treatment on the gain resulting from the value allocated to these intangibles upon the sale of the business. This area of the law is complex and evolving, and sellers should consult with tax and valuations specialists to determine how best to cope with these new provisions.

So what are the most important takeaways?

- The C corporation will generate more cash flow for debt repayment or retention for growth, but the benefits on exit may outweigh the cost of less cash in the operating period.

- As shown above, the ability to qualify for the FTD, and to be taxed as an active versus passive owner, significantly lowers the tax on the income of FTEs. • The more cash a company wants to distribute, the less C corporations gain during the operating period (due to double taxation of C corporations dividends).

- It is highly unlikely that a C corporation will sell assets (unless it is selling a subsidiary, or has very significant net operating losses).

- Timing and the future actions by Congress matter. Note that with the loss of the 20% deduction and the reversion of the 37% rate to 39.6% in 2026, the longer the modeling period the more advantageous a C corporation status becomes.

- While FTE’s will typically sell for a higher price due to the buyer receiving a stepped-up basis in assets, this advantage has been dampened by the reduction in C corporation tax rate

State tax considerations

Our modeling has assumed a 5% effective state tax rate for both C corporations and FTEs. This simplistic assumption should not be used for modeling your specific circumstance, particularly because for most taxpayers owning FTEs, state taxes are no longer deductible, while they are deductible for C corporations. The ability to fully deduct state taxes can lower the cost of state taxes by as much as 21%.

To make matters more complex, it appears the legislation may permit owners of S corporations that are held as “electing small business trusts” to deduct state taxes. Individuals, other trusts, and any partnership owners would not have this benefit. Given this unusual and likely unintended result, owners must decide whether to model this benefit as a likely survivor of corrective action by Treasury or Congress.

It is crucial to add detailed modeling of your actual state tax situation into your choice of entity model, as the taxation of a C corporation versus an FTE can vary greatly based on the states where you do business, where your owners reside and allocation and apportionment factors.

Last, it is worth noting a growing trend among FTE owners to own a significant portion of the business in trusts, particularly generation-skipping estate tax-exempt trusts and for those trusts to be resident in states with no state income tax. Planning to take advantage of no-tax states can also influence your choice of entity modeling.

Evaluating making a change, and its risks

The lower tax regime afforded today’s C corporations at 21% is very attractive. This is accentuated by long-term horizon models that show the 20% FTD and the 37% rate sunsetting, and the benefits of a step-up to a purchaser diminished. These C corporation advantages need to be weighed against many factors, not the least of which is the loss of tax benefits on an exit, as discussed extensively above.

Owners need to also consider how easy it is to move from an FTE to a C corporation, and how hard it is to move back. “S-to-C” conversions require a five-year waiting period before re-electing S corporation status. Once re-elected, there is another five-year ”built-in gains” tax period, which greatly reduces the benefits of selling an S corporation. Conversion of a partnership to a C corporation is relatively straightforward. However, changing from a C corporation back to a partnership can require enormous one-time tax burdens. More likely the owners would make an S election than re-seek partnership status from C status. S status is generally not as desirable as having partnership status.

Moreover, political winds may shift, allowing a new Congress to reconsider some or all of the provisions enacted in the TCJA. The corporate rate cut is not set to expire like the individual and pass-through changes, but that doesn’t mean it will never change. Modeling should include sensitivity analysis to see how future changes in the tax law might influence current structuring strategies.

Overall, our advice is to create models with as many details and as many scenarios as are relevant to a business, and to be mindful of getting the right advice on model construction to be confident in both its assumptions and conclusions. The process of making the choices that need to be made in the wake of tax reform should include a team of advisors to make sure business leaders have covered all the bases before making decisions, particularly revoking FTE status that, as noted above, is difficult to restore.

Ideally, a business’s entity choice team should include:

- Company owners to consider operating, growth, and exit strategies as well as succession planning considerations

- Company C-suite executives (and support) to prepare financial projections of the business operations, including required growth capital, capital expenditure requirements, strategic investments and other related functions

- Financial and tax accountants (including federal, state and local, and international experts, as applicable) to prepare or review the financial models and tax modeling of scenarios

- Transaction specialists (investment bankers or other trusted advisors) who can be consulted on growth and exit strategies, valuation, timing and other similar factors

Some circumstances are reasonably easy to figure out, and the analyses can be done quickly and at a high level. But many, particularly those with extensive multi-state and international operations, will require an intensive effort to make informed decisions.

Conclusion

The important tax reform provisions are already in effect for 2018. While in a perfect world, everyone would have completed their analysis in the first 75 days of this year, many are just getting started. And no company should make any decisions around structuring and future transactions without the proper analysis. The analysis is complex and depends on many factors, including tax issues not covered in this paper and non-tax considerations. Despite the difficulties, the analysis is well worth it. The tax differences created under the new tax reform law, and its ramifications, are potentially immense.

{kind=link}