Congress Passes Covid-19 Related Tax Payroll Credit relief & IRS extends Tax filing Deadline to July-15th

In an effort to mitigate some of devastating economic impact of the COVID-19 virus, grinding “non-essential” businesses to a halt temporarily. Congress passed the Families First Coronavirus Response Act (the Act) aid package last week. The Act includes two payroll tax credits to help employers cover wages paid to employees that need time off due to the virus. NPR and Baker Tilly reported on this. An opinion article in The Hill argues it treats small businesses unfairly. In addition Republicans, and Democrats passed a 2 Trillion Cares Act Stimulus package offers deep tax relief to both businesses and individuals. The compromise bill moved quickly through Congress on overwhelming bipartisan support and was signed into law by the president on March 27.

In an effort to mitigate some of devastating economic impact of the COVID-19 virus, grinding “non-essential” businesses to a halt temporarily. Congress passed the Families First Coronavirus Response Act (the Act) aid package last week. The Act includes two payroll tax credits to help employers cover wages paid to employees that need time off due to the virus. NPR and Baker Tilly reported on this. An opinion article in The Hill argues it treats small businesses unfairly. In addition Republicans, and Democrats passed a 2 Trillion Cares Act Stimulus package offers deep tax relief to both businesses and individuals. The compromise bill moved quickly through Congress on overwhelming bipartisan support and was signed into law by the president on March 27.

Families First Coronavirus Response Act

Families First Coronavirus Response Act

To help small businesses deal with the impact of the coronavirus pandemic, the Act provides for two payroll tax credits. It is critical to note that these credits are only available to employers with fewer than 500 employees. The bill establishes a federal emergency paid-leave benefits program to provide payments to some employees.

- Sick leave credit – not to exceed $511 per employee per day. This credit is designed to assist with the cost of providing up to two weeks of paid coronavirus-related sick leave to employees. The credit is limited to 10 days and is in effect for wages paid through December 2020. In addition, the employer cannot use this credit in connection with wages for which the employer is already receiving the employer credit for paid family and medical leave, under a provision previously enacted by the Tax Cuts and Jobs Act (TCJA). On a quarterly basis, the credit is limited to the total taxes imposed on the employer portion of the Social Security payroll tax and is refundable in certain circumstances.

- Self employment sick leave credit – A similar credit is available to self-employed individuals, amounting to the lesser of their average daily self-employment income, or $511 per day, if caring for themselves or $200 if caring for a family member. The credit is limited to 10 days.

- Family leave credit – not to exceed $10,000 per employee. This credit is designed to compensate employers for providing paid coronavirus-related family leave to employees as separately required under the Emergency Family and Medical Leave Expansion Act. Similar to the sick leave credit, this credit is also limited to the employer portion of the Social Security payroll tax on a quarterly basis but is refundable in certain circumstances.

The Act also includes several nontax provisions, which provide paid leave and food assistance to those affected by the virus, makes testing for the virus free, and expands unemployment insurance and Medicaid funding to states.

The Act dictates the Treasury Department to issue guidance on documentation requirements. Until such guidance is issued, taxpayers should track the following information:

- Each employee requesting sick leave due to the COVID-19 virus; document whether the employee is caring for themselves or a family member

- Compute employee wages compared to the requisite $511 or $200 per day in order to determine the actual amount of the credit

Baker Tilly’s article states “Be prepared to supply such information as part of quarterly payroll tax return or annual income tax return filings.”

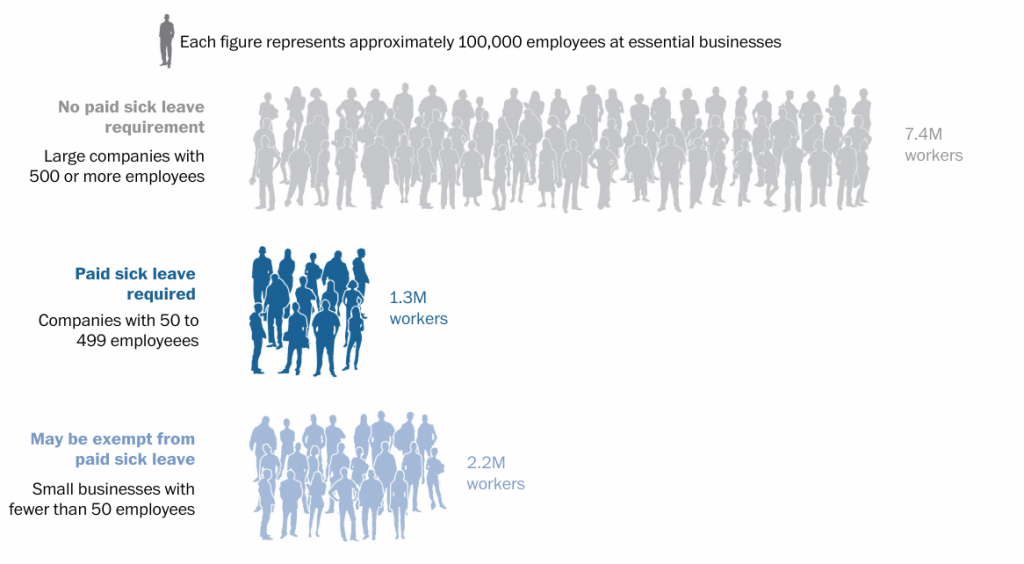

As a Washington Post article titled “Which workers are covered by the Families First Coronavirus Response Act” points out that most essential workers are at companies too big or too small to gain sick leave. The guarantee only applies to employers with more than 50 and fewer than 500 employees. The White House and Congress argue that businesses with under 50 employees could be exempt from the tax.

Coronavirus emergency leave protection

Coronavirus emergency leave protection

The Act creates an emergency paid leave program that requires private sector employers with fewer than 500 workers and government entities to provide two weeks of job-protected leave under the Family and Medical Leave Act (FMLA) for employees who have to:

- Quarantine because of exposure to or symptoms of the coronavirus

- Provide care to a quarantined family member

- Provide care for child younger than 18 whose school or day care has closed in response to the coronavirus

Employees providing care for a child whose day care has closed as described above would be eligible for up to an additional 10 weeks of leave. For these employees, the first 10 days of leave could be unpaid, however, employees can choose to use vacation days, personal leave or other available paid leave. Following the 10-day period, workers would receive a benefit from their employers that will be at least two-thirds of their normal pay rate.

The legislation modifies the FMLA to allow individuals to use unpaid leave if they are diagnosed with the virus, caring for a family member or caring for a child whose school or day care has closed because of a public health emergency through Dec. 31, 2020.

Coronavirus emergency paid sick leave

Employers with fewer than 500 employees and governmental employers must provide employees with temporary paid sick time. Employees must be allowed to use this additional paid sick leave before using any other paid leave benefits.

The duration and amount depends on whether the employee is full time or part time. For a full-time employee, the employer is required to provide 80 hours of paid sick time. For a part-time or hourly employee, employer-provided paid sick leave would be the hours the employee was scheduled to work in the two-week period. For a variable-hour employee, the Act provides for a calculation based upon historical work or anticipated work.

The rate of pay depends upon the reason for the employee’s absence. For absences based upon the employee’s condition, paid sick leave will be paid at the employee’s regular rate. For absences based upon a family member’s situation, pay will be two-thirds of the employee’s regular rate.

Emergency paid sick leave is for an employee who is unable to work or telework because the employee:

- Is subject to a coronavirus-related government order to go under quarantine or isolation

- Has been advised by a healthcare provider to self-quarantine due to concerns related to coronavirus

- Is seeking a medical diagnosis where the employee is experiencing symptoms of coronavirus

- Is caring for an individual for whom quarantine or isolation is required

- Has children whose school or place of care has closed or the child care provider is unavailable due to coronavirus precautions

The Act includes an important exception for certain employers. Employers of healthcare providers or emergency responders may elect to exclude those employees from emergency paid sick leave.

The Act authorizes the Labor Department to issue regulations to:

- Exclude certain healthcare providers and emergency responders from paid leave benefits

- Exempt small businesses with fewer than 50 employees from the paid leave requirements

Workers under a multiemployer collective bargaining agreement and whose employers pay into a pension plan will also have access to paid leave.

IRS Concedes on Extending Tax Filing Deadline to July 15

IRS Concedes on Extending Tax Filing Deadline to July 15

According to an article recently reported in Accounting Web that the IRS conceded to pressure from various sources—from both within and outside the government—the IRS is extending the usual April 15 tax filing deadline to July 15. The announcement was “tweeted” by Treasury Secretary Steven Mnuchin on March 20. Stating “we are moving Tax Day from April 15 to July 15. All taxpayers and businesses will have this additional time to file and make payments without interest or penalties.”

At @realDonaldTrump’s direction, we are moving Tax Day from April 15 to July 15. All taxpayers and businesses will have this additional time to file and make payments without interest or penalties.

— Steven Mnuchin (@stevenmnuchin1) March 20, 2020

The latest move by the IRS is part of the expanding efforts by the government to stem the financial fall-out from the COVID-19 pandemic. It gives taxpayers another 90 days to file their federal income tax returns for the 2019 tax year without incurring any interest or penalties.

Previously, on March 17, Steven Mnuchin said that individual taxpayers would be able to defer up to $1 million in tax payments to the IRS until July 15 because of the COVID-19 outbreak. He noted that this threshold was intended to accommodate pass-through entities, like S corporations and partnerships, where taxes are reported on individual returns. A comparable delay of up to $10 million is available to corporations.

The extension to pay taxes also applies to federal estimated tax payments for the first quarter of 2020 that would normally be due on April 15.

Some lawmakers and several members of the tax community, including the American Institute of CPAs (AICPA) have been vocal about the need for the IRS to push back the April 15 filing deadline in this current environment. Now the agency has taken the feedback and changed the timeline.

Conclusion

Over the last week the mandated social distancing measures has virtually shut down normal life in much of the US. And news reports are starting to forcast or point to a sudden surge in layoffs and a collapse in spending, both historic in size and speed, as well as shutdowns of many schools, stores, offices, manufacturing plants, and construction sites. These developments argue for a much sharper drop in GDP in Q1 and Q2. Efforts to provide small and large businesses some liquidity relief from impacts of the coronavirus (COVID-19) pandemic are starting to develop.

The Trump Administration has announced on March 10 that he would ask Congress to increase funding for the Small Business Administration (SBA) lending program to $50 billion to help companies stay in business. But with the grid lock on the hill, Congress has yet to pass a rescue package that could include about $350 billion in loans for small businesses that would convert into grants if they retain most of their workforce. Those companies can apply for low-interest disaster loans from the Small Business Administration. The catch: it can take as long as 21 days to process an application. Once approved, it might take another week to go through According to a recent report from the Research Institute of JP Morgan Chase, it states that “small businesses tend to have volatile and irregular cash flows. Cash liquidity and cash flow are critical predictors of small business survival—those with less liquidity and irregular cash flows are least likely to keep their doors open. With rapidly unfolding reactions to the coronavirus keeping more and more Americans home, this unforeseen event is a cause for concern to the 30.2 million small business owners who make up this key pillar of the U.S. economy, and the millions more they employ.” Now larger companies with more of a cash buffer may be best equipped to weather the impacts of COVID-19 but JPMC Institute research shows that 50 percent of small businesses have less than 15 cash buffer days, meaning the small business economy could be majorly disrupted by the current climate. So we shall see what happens to Covid 19 crisis and the economic fall out from it the next coming weeks.

During this uncertain time, Huckabee CPA is ready to help you with practical advice on informing and supporting your employees as well as keeping your business running. Are you struggling with critical finance tasks as your workforce is at home? Huckabee CPA leverages best-in-class technology to provide both short-and long-term solutions to perform your critical finance and accounting tasks remotely. Contact us for a questions or for a free consultation

{kind=link}