Despite the Booming Job Market, Labor Force’s Income Is Shrinking

Because Trump and Republicans like to brag that U.S. unemployment levels are at their lowest in nearly 50 years, with some businesses even griping about labor shortages (skills gap), one might infer that American workers, having increased bargaining leverage, would be receiving a larger portion of the economic pie (meaning wage growth would be rising).

Because Trump and Republicans like to brag that U.S. unemployment levels are at their lowest in nearly 50 years, with some businesses even griping about labor shortages (skills gap), one might infer that American workers, having increased bargaining leverage, would be receiving a larger portion of the economic pie (meaning wage growth would be rising).

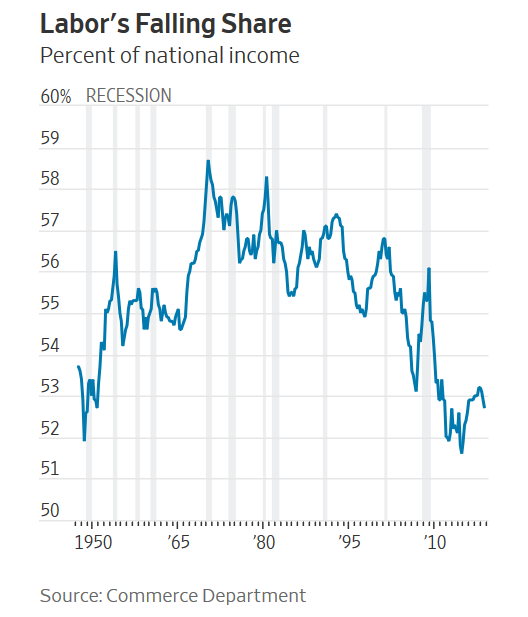

That does not seem to be the case according to data from the WSJ, which firmly maintained that since 1970, labor’s slice of domestic income has been in a decline. According to data from the Bureau of Economic Analysis, employee pay and benefits as a percentage of gross domestic income fell to 52.7%.

For context, back in 1970, it was at 59% and back in 2001 it was 57%. If workers could command as much domestic income as they got back in 2001, it is estimated they would collectively have $800 billion or $5,100 each extra in their pockets. Conversely, as labor’s share of income has dropped, corporate business profits, including pass-through entities, landlords and other businesses have closely doubled since the 80s, when it was 12% of gross domestic income to now it is over 20%.

Let’s Dive a Little Deeper

Let’s Dive a Little Deeper

The economic data tells a story of a trend that has been decades in the making and has occurred alongside dismantling of union membership, stagnating middle class and the increase in global trade. Now, one may argue that corporate profits give some household benefits in the form of higher stock prices and dividends. Unfortunately, the top 10 percent income earners own 84 percent of stocks, not the middle class. Where wages are the largest income source for most middle and lower families means that the distribution of wealth is becoming more uneven as time goes by. What seems a little strange about labor’s current income share decline, in the last few economic quarters, is that coincided with unemployment hitting a 3.7% record low, and growth in wages at the quickest pace in a decade, you had some CEOs complaining about not having enough workers to fill their jobs. Similar economic conditions in previous cycles have actually pushed the labor share up and the profit share down as corporations cut into their margins to retain increasingly scarce workers. For instance, during the tech boom, labor share went up by about 2%. The WSJ interviewed Julia Coronado, the founder of economic-research firm MacroPolicy perspectives, and she said “it should be rising.” She went on to add “this is the point of the cycle where workers should be able to bid back some of the production, and that really hasn’t materialized.”

So, foolheartedly, economists for the most part of the 20th century had believed that both labor productivity and capital would claim more even shares of output (meaning total revenue or units of finished goods) under the premise that an overdependence on either one would be bad for economic returns or GDP. The theory was that having an office with 10 top of the line computers and a single worker would become tremendously more effective by adding more people, compared to an office that had 10 Princeton graduates but had out of date dial-up internet system would benefit from an equipment upgrade.

Famous British economist John Maynard Keynes, in an article back in 1939 titled “Relative Movements of Real Wages and Output,” wrote about the idea or theory that wages or wage productivity claimed a relatively steady share of output, even with varied economic-growth rates. He said, “this is one of the most surprising, yet best-established facts in the whole range of economic statistics,” He also stated that this is “a bit of a miracle.” The wage or labor share is a key indicator for the distribution of income. Since his economic theory about wage share being stable, other economists such as Dorothee Schneider author of “The Labor Share: A Review of Theory and Evidence” have found that the wage share is more “counter-cyclical.” As it tends to fall when output increases and rise when output decreases. Despite fluctuating over the business cycle, the wage share was once thought to be stable, however, as mentioned earlier that the wages or wage share have been declining since the 1970s.

From the time periods ranging from 1960 all the way to 2000, employee compensation averaged a whopping 56.4% of gross domestic income. While that level went up and down during different business cycles – with it rising in the run-up to recessions and then falling after they hit – it never really went below 55% for an entire year during that time period.

The Rise of Technology and Globalization are a Factor

The rise of the globalization of companies was sped up in 2001 when China finally became a member of the World Trade Organization, which gave businesses that make products options to ship their manufacturing overseas to save money with the cheap labor alternatives. For large publicly traded companies such as Google, Walmart, Amazon or Apple, corporate success analyzed by Wall Street is increasingly measured on a global scale of penetration in different markets around the world. This is effectively creating a sort of “winner takes all” dominance for these large technology corporations that use their global supply chain scale to dominate smaller, local competitors. With waning competitive pressure: productivity growth slows down, wages stagnate, and the gap between winners and losers widens.

The Wall Street Journal spoke with John Van Reenen, an economics professor at MIT who said “One of the features of these very big firms is that they’ve got high profits but they have low labor shares.” He went on to define the economic changes further by saying “part of what’s happening is that as more and more of the weight of the economy goes toward these superstar firms, this tends to drag down the share of labor in the aggregate income.” And according to some economic theories, as unemployment rates go down, labor shares should start to go up, and back in 2014 the economy started to show some signals of this. According to Ernie Tedeschi, who is an economist at Evercore ISI said “As we get closer and closer to full employment, you’d expect the labor share to rise…because firms find that in order to maintain wage increases, they need to dip into margins.”

However, these with all of these hopeful predictions about wage growth increasing seem to have not come to fruition. There has been quite a few times in the last few years after the recovery from the 2008 recession that the Congressional Budget Office had projected the labor share of economic income would start rebound a little. But instead, it has continued to stagnate. Again many economists say long-running trends could spark a full recovery. Last October an article titled “The labor market is booming, why aren’t your wages?” originally published in The Hill, offers a few possible explanations for the slow wage growth. The author asserts four possible reasons include; labor markets might be weaker than they seem, increasing employer concentration, changes in labor market institutions, business and labor market dynamism.

Conclusion

A low unemployment rate does not automatically mean that the labor market is working perfectly incongruence. Policymakers should support more market competition, (industry M&A consolidation are bad for competition) so that productivity growth translates into wage growth. Another looming challenge is the disruptive advances in robotic technology and AI that are expected to displace millions of jobs in the next 20 years as mundane or routine duties such as truck driving or reviewing loan documents may become automated.

</a

</a

{kind=link}