Strategies to Reduce the Tax Impacts of Selling your Privately Held Business

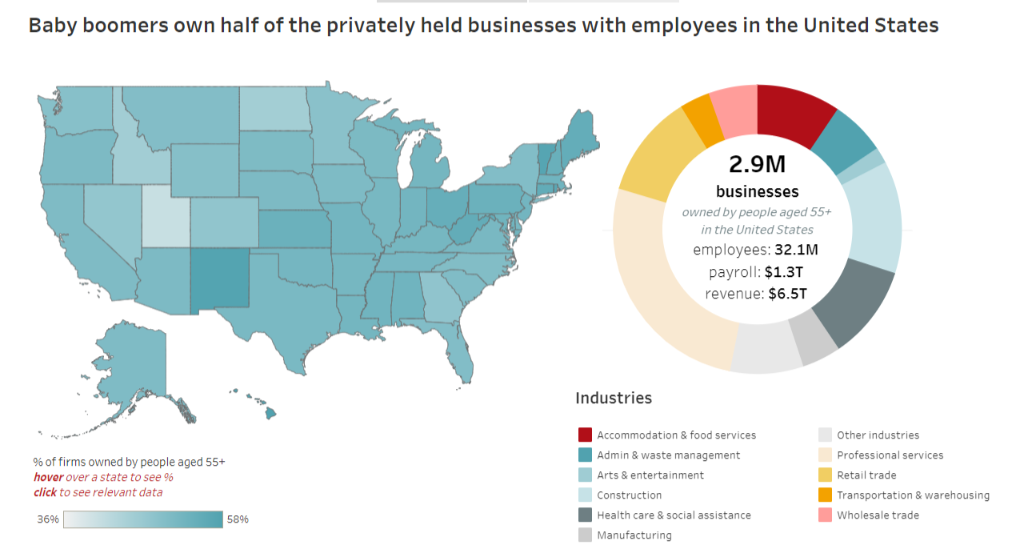

According to a 2021 study from Project Equity, baby-boomers business owners control nearly half of all privately held businesses( 2.9 million companies) which also represents half of all job-creating enterprises in the country. These firms employ over 32 million workers and generate nearly $6.5 trillion in revenue.

And this nonprofit organization is predicting that 6 out of 10 owners plan to sell their businesses within the next decade. If you’re among this number or a younger-generation owner thinking of selling a business, there are a number of tax considerations and impacts that you should be aware of.

(Image credit:PROJECT eQUITY)

I have written about succession planning in family owned businesses. When it comes time for a business owner to transition or sell their business, taxes tend to be one of the most important negotiating points. Can you minimize or defer some of the taxes that you pay? Possibly. It’s best to work with a qualified CPA, tax advisor and M&A consultant as the rules for selling a business are complicated.

Thoughtful tax, trust and estate planning and business succession strategies can also provide opportunities to maximize legacy economic wealth for business owners.

Some common tax consideration issues include:

- Ordinary income vs. capital gains.

- Gains on some of the assets being transferred may have to be taxed at ordinary income tax rates, rather than at the 15 percent maximum long-term capital gains tax rate.

- Installment sales. If you defer receipt of the purchase price to later years with an installment sale, you may be able to postpone paying tax on your gains until you receive them.

- Double taxation of corporations. For businesses organized as corporations, the structure of the deal as an asset or stock sale can have very different tax results.

- Tax-free reorganizations. Where one corporation is buying another, you may be able to structure the sale as a tax-free merger.

The law firm Wolters Kluwer wrote a post about this topic where they mention “the amount of tax that you will ultimately have to pay depends upon whether the money you make from the sale is taxed as ordinary income or capital gains. Profit received from the sale of the business assets will most likely be taxed at capital gains rates, whereas the amount you receive under a consulting agreement will be ordinary income.”

Allocation of sales price governs tax consequences

If you negotiate a total price for the business, you and the buyer must agree as to what portion of the purchase price applies to each individual asset, and to intangible assets such as goodwill. The allocation will determine the amount of capital or ordinary income tax you must pay on the sale. It will also have tax consequences for the buyer.

What is good for the tax picture for the seller is often bad for the buyer and vice versa, so the allocation of price to various components of the deal is frequently an area for negotiation and compromises.

The Wolters Kluwer blog also mentions that “what is good for the tax picture for the seller is often bad for the buyer and vice versa, so the allocation of price to various components of the deal is frequently an area for negotiation and compromises.”

The taxable amount at issue is your profit: the difference between your tax basis and your proceeds from the sale. Your tax basis is generally your original cost for the asset, minus depreciation deductions claimed, minus any casualty losses claimed, and plus any additional paid-in capital and selling expenses. Your proceeds from the sale usually equate to the total sales price, plus any additional liabilities the buyer takes over from you.

As the seller, you will probably want to allocate most, if not all, of the purchase price to the capital assets that were transferred with the business. You want to do that because proceeds from the sale of a capital asset, including business property or your entire business, are taxed as capital gains.

Under current law, long-term capital gains of individuals are taxed at a significantly lower rate than ordinary income. In fact, if you’ve held the asset for longer than 12 months, the maximum tax on long-term capital gains is 15 percent for qualifying taxpayers. (Taxpayers in the 10- and 15-percent tax brackets pay zero percent.)

The IRS states that “the sale of a business usually is not a sale of one asset. Instead, all the assets of the business are sold. Generally, when this occurs, each asset is treated as being sold separately for determining the treatment of gain or loss.”

If your business is a sole proprietorship, a partnership, or an LLC, each of the assets sold with the business is treated separately. (A corporation can also take this route, but it also has the option of structuring the sale as a stock sale.) So, the formula described above must be applied separately to each and every asset in the sale (you can lump some of the smaller items together, however, in categories such as office machines, furniture, production equipment, etc.). Certain assets are not eligible for capital gain treatment; any gains you receive on that property are treated as ordinary income and taxed at your normal rate.

After the sale, the buyer will be able to depreciate or amortize most of the assets that were transferred. Because different types of assets are depreciated differently under IRS rules, the buyer is going to want to allocate more of the price toward assets that can be depreciated quickly, and less of the price to ones that must be depreciated over 15 years (such as goodwill or other intangibles) or even longer (such as buildings) or not at all (such as land).

The IRS lays out some guidelines as to how you should allocate the purchase price.

Assets should be valued at their fair market value in the following order:

- Class 1: Cash and deposits (including checking and savings account deposits)

- Class 2: Actively traded personal property, including certificates of deposits, foreign currency, U.S. securities, and publicly traded stock

- Class 3: Accounts receivable and anything else that you mark-to-market at least annually

- Class 4: Inventory or other property held for sale to customers in the ordinary course of business

- Class 5: All other assets not included in another class. This usually includes furniture, building, land, vehicles, and equipment

- Class 6: Section 197 intangible assets, except goodwill and going concern. Licenses and trademarks are usually included here

- Class 7: Goodwill and going concern value

Capital gains result in lower tax liability

When you sell your business, for tax purposes, you are actually selling a collection of assets. Some of these are tangible (such as real estate, machinery, inventory) and some are intangible (such as goodwill, accounts receivable, a trade name).

Unless your business is incorporated and you are selling the stock, the purchase price must be allocated among the assets that are being transferred. According to IRS rules, the buyer and seller must use the same allocation, so the allocation will have to be negotiated and put in writing as part of the sales contract.

Apportioning the price between assets can be a big bone of contention. The buyer wants as much money as possible to be allocated to items that are currently deductible, such as a consulting agreement, or to assets that can be depreciated quickly. This will improve the business’s cash flow by reducing its tax bill in the critical first years.

The seller, on the other hand, wants as much money as possible allocated to assets on which the gain is treated as capital gains, rather than to assets on which gain must be treated as ordinary income. The reason is that the tax rate on long-term capital gains for noncorporate taxpayers is much lower than the highest maximum individual tax rate.

Given that most small business owners who are successful in selling their company are in high tax brackets, this rate differential is very important in reducing tax liability.

Any gains on property held for one year or less, inventory, or accounts receivable are taxed at ordinary income rates. According to the law firm Wolter Kluwer the “amounts paid under non-compete agreements are ordinary income to you and amortizable over 15 years by the buyer unless the IRS successfully argues they are really part of the purchase price.” Amounts paid under consulting agreements are ordinary income to you and are currently deductible to the buyer.

Negotiate everything for the sale of a sole proprietorship

Barbara Weltman, an SBA contributor wrote an interesting blog post on this subject, if your business is a sole proprietorship, a sale is treated as if you sold each asset separately. Most of the assets trigger capital gains, which are taxed at favorable tax rates. But the sale of some assets, such as inventory, produces ordinary income. It’s up to the parties to negotiate the terms of the sale, which includes allocating the purchase price to the assets of the business.

IRS Form 8594, Asset Acquisition Statement, shows seven classes of assets to which you must allocate the purchase price. The first class includes cash and checking accounts, to which you allocate the purchase price dollar-for-dollar. The final class (class VII) is for goodwill and going-concern value. This is the intangible asset that commands part of the purchase price. The more goodwill the business had, the greater the allocation to this class.

You should also be aware that allocation is a negotiation. The reason: while the seller wants to allocate as much as possible to capital gain assets such as goodwill, the buyer wants a good allocation for assets, such as equipment and realty, that can be depreciated going forward.

Sell a partnership interest

The sale of an interest in a partnership is treated as a capital asset transaction; it results in capital gain or loss. But the part of any gain or loss from unrealized receivables or inventory items will be treated as ordinary gain or loss. Capital gain deferral is possible through an Opportunity Zone investment project.

Decide on a corporate sale of stock or assets

If you own a corporation, there’s a choice in how to structure the sale: sell stock or characterize the transaction as a sale of assets. Generally, sellers like to simply sell the stock to limit tax reporting to capital gain on the transaction. But buyers prefer an asset sale because this creates a higher basis for the depreciable assets they’re acquiring. Again, negotiations between the parties can resolve the structure of the sale. For example, a seller may be willing to take a little less to complete a stock sale, reflecting the higher tax bill that would have resulted from an asset sale.

Make an S election

The characterization of the sale as a stock or asset sale applies equally to C and S corporations. But there are tax savings to be reaped by being an S corporation. Gain on the sale of a C corporation requires the owner to report an additional 3.8% Medicare tax on this net investment income. In contrast, if the business is an S corporation and the owner is actively involved in the business and not merely a silent investor, then the gain is not subject to this tax. If a C-corporation is planning on a sale it can make an S election where advisable, assuming the corporation meets the requirements for being an S corporation.

Use an installment sale

One of the ways to minimize the tax bite on profits from the sale of a business is to structure the deal as an installment sale. If at least one payment is received after the year of the sale, you automatically have an installment sale. If you are willing to finance the sale of your business by taking back a mortgage or note for part of the purchase price, you might be able to report some of your capital gains on the installment method. This is good news because the method allows you to defer some of the tax due on the sale until you get paid over the course of future years. But there are some points to keep in mind. You can’t apply installment sale reporting for the sale of inventory or receivables. And there’s always a risk in an installment sale arrangement that the buyer will default. Details on installment sales in the instructions to Form 6252.

Sell to employees

In the SBA Mrs Weltman suggests a strategy by saying “if your business is a C corporation and you plan ahead, you can sell your business to your staff through an employee stock ownership plans (ESOP). The ESOP is owned by employees (find more information about ESOPs from the IRS). From an owner’s perspective you have captive buyers and don’t have to search around. You set a reasonable price for the sale and receive cash from the ESOP. You can then roll over the proceeds into a diversified portfolio to defer tax on the gain.”

You can also use ESOPs for S corporations, but the deferral option for an owner doesn’t apply. Revoking an S election in anticipation of a sale is something to consider.

Reinvest the gain in an Opportunity Zone

Owners who realize capital gains on the sale of their business have a way in which to defer tax on that gain if they act within 180 days of the sale. They can reinvest their proceeds in an Opportunity Zone (you go into a Qualified Opportunity Zone (QOZ) Fund for this purpose). Deferral is limited because gain must be recognized on December 31, 2026, or earlier if the interest in the fund is disposed before this date. Holding onto the investment beyond this date can result in tax-free gains on future appreciation. An owner who sells his or her business doesn’t have to put all the proceeds into a QOZ, but tax deferral is limited accordingly. Find details about Opportunity Zones from the IRS.

Conclusion

Many business owners find it difficult to walk away from their businesses. They love the action and don’t have personal plans for their time in retirement. They can consider negotiating a consulting agreement with the buyer. This gives the departing owner ongoing income and continuing tax breaks (such as claiming the qualified business income deduction if eligible).

A sale of a business is a highly complex matter from a legal and tax perspective. Don’t proceed without getting expert advice beforehand. Working with a CPA professional can help you navigate some of the complex scenarios and find a strategy that can help to reduce the amount you owe in taxes. If you have any questions feel free to reach for a free consultation.

{kind=link}