There comes a time between points A and B of building a business when money makes the difference. Whether that point is an initial seed raise to jump start an idea or a series A round to grow to the next level, timing differs depending on your business. No matter what, every entrepreneur will tell you that securing investors is no walk in the park.

There comes a time between points A and B of building a business when money makes the difference. Whether that point is an initial seed raise to jump start an idea or a series A round to grow to the next level, timing differs depending on your business. No matter what, every entrepreneur will tell you that securing investors is no walk in the park.

If fundraising a business were easy, everyone would be an entrepreneur.

If you are a first time startup founder, who is fundraising, you should be prepared that you will hear more no’s from VC’s than not. It can be intimidating to go into meetings with investors without having much prior experience. TechCrunch recently wrote a white paper guide article about some of the best practices of pitching VCs to secure funding in 2021. And the article mentioned that if you are new to the startup and VC world, you might have a few questions such as:

- What information should you prioritize?

- How do you break the ice?

- What are the characteristics of a good VC?

- How do you gauge the level of investor interest?

The TechCrunch guide gives an overview of the VC investor fundraising landscape in a post-pandemic world and it is broken up into different topics written by different people with diverse perspectives.

In this article I will cover subjects such as:

- Assembling your Business Basics

- Understanding Pre-seed, Seed, Series A,B,C, funding works

- What to expect as startup founder while fundraising in 2021

- How Investors Use Financial Reports to Assess Risk

- How to pick an investor in good or bad times

- Decoding Investor Questions — What They Really Mean and How You Can Respond

Assembling your Business Basics

Indinero put together a guide on fundraising which is pretty useful and one of their chapters covers some of the fundraising basics. Getting noticed by accelerators, VCs, and other investors starts with having a credible company foundation. Investors want to partner with companies that are functional and stable. Here are a few tips on what you’ll need to get started:

Incorporate Your Business

Venture capitalists, accelerators, and incubators typically prefer to invest in C corporations, which provide a predictable legal structure and allow investors to issue equity or preferred shares of stock. Extra credit: incorporate your startup in the state of Delaware. Delaware laws are particularly friendly to corporations and their investors (no corporate income tax!).

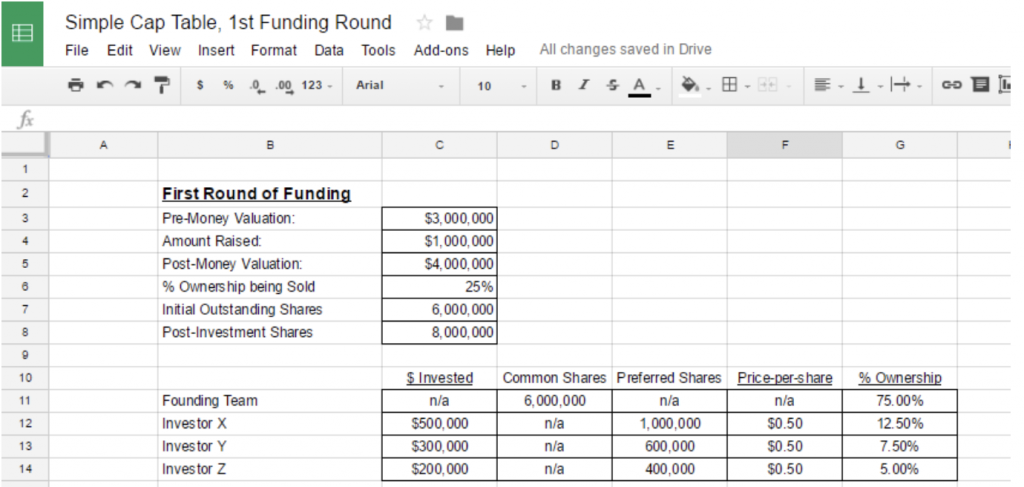

Set up a Capitalization Table

A capitalization table, or cap table, is like a map of a business’s DNA. At a high level, the cap table is a spreadsheet businesses use to track who owns what percentage of a company. A well-organized cap table is an integral part of investor negotiations. Investors will want to see the existing capital structure of the company and where they will fit in, while the founders (that’s you) will use it to forecast how new investments will dilute ownership percentages and the value of each share. This article by Serif Investor titled “Understanding startup capitalization tables” explains that “the cap table tracks the equity ownership of all the company’s shareholders and security holders and the value assigned to this equity.” In case it is not clear, cap tables need to be comprehensive. They should include all elements of company stakeholders such as convertible debt, stock options and warrants in addition to common and preferred stock.

Put Together Your Term Sheet

Once you have a cap table, your term sheet is a non-binding agreement that sets the basic terms and conditions for investments. This dictates the investment type, interest rates, and agreed-upon company valuation.

Get Organized–Financially

When you ask someone for money, be prepared to talk about the money you already have. Show financiers that you mean business by making sure you have the financial reports and accounting policies that accelerators, VCs, and other investors expect based on your growth stage. I will cover what kinds of reports you should have on hand and how to use them later on.

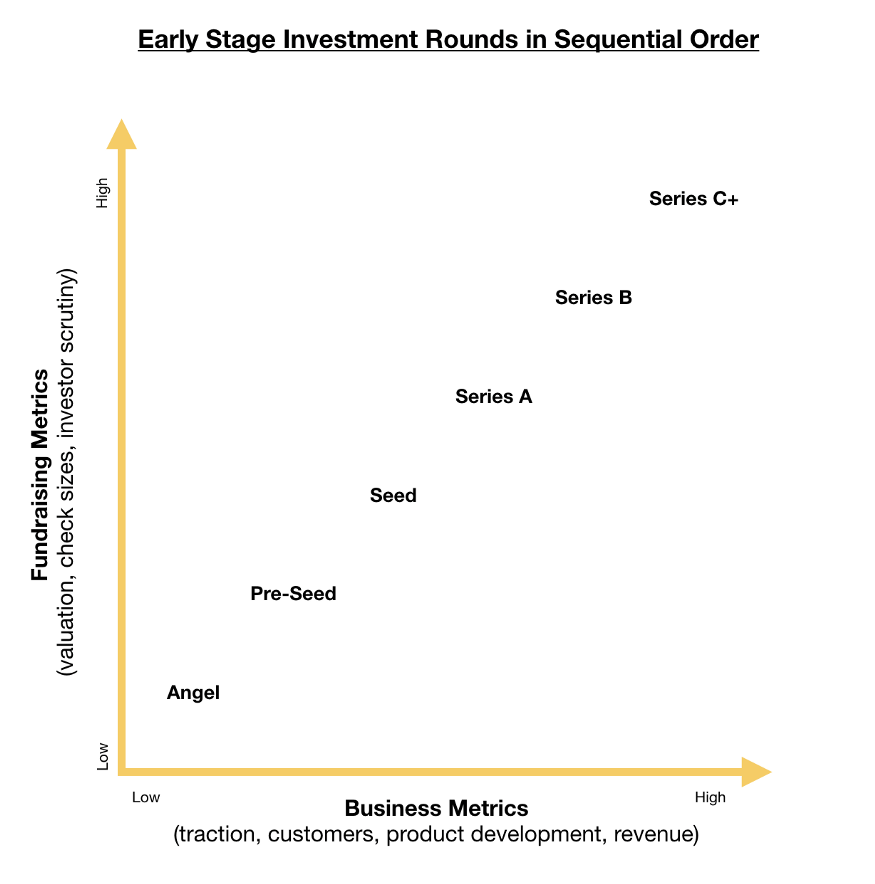

How Seed and Series A, B, C Funding Work

If you’ve never gone after equity financing, it can be hard to know what to expect. What are the differences between each round? What does each one entail? Here we’ve listed the primary types of funding rounds and the financial expectations associated with each one.

An Investopedia article explains that the path for each startup is somewhat different, as is the timeline for funding. Many businesses spend months or even years in search of funding, while others (particularly those with ideas seen as truly revolutionary or those attached to individuals with a proven track record of success) may bypass some of the rounds of funding and move through the process of building capital more quickly.

Once you understand the distinction between these rounds, it will be easier to analyze headlines regarding the startup and investing world, by grasping the context of what exactly a round means for the prospects and direction of a company. Series A, B and C funding rounds are merely stepping stones in the process of turning an ingenious idea into a revolutionary global company, ripe for an IPO.

Before any round of funding begins, analysts undertake a valuation of the company in question. Valuations are derived from many different factors, including management, proven track record, market size and risk. One of the key distinctions between funding rounds has to do with the valuation of the business, as well as its maturity level and growth prospects. In turn, these factors impact the types of investors likely to get involved and the reasons why the company may be seeking new capital.

- Pre-Seed Funding – the earliest stage of funding a new company comes so early in the process that it is not generally included among the rounds of funding at all. Known as “pre-seed” funding, this stage typically refers to the period in which a company’s founders are first getting their operations off the ground. The most common “pre-seed” funders are the founders themselves, as well as close friends, supporters and family.

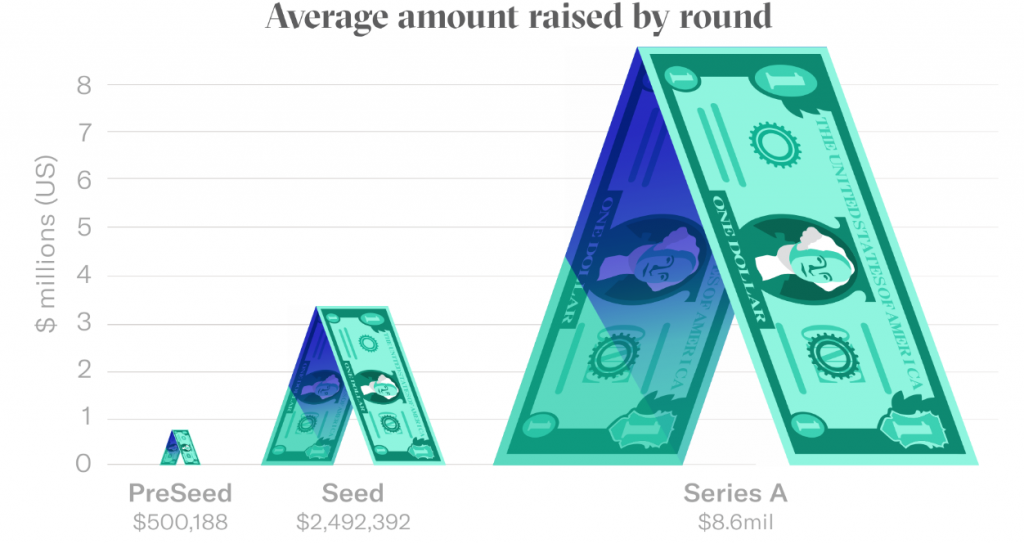

- Seed Funding – is the first official equity funding stage. It typically represents the first official money that a business venture or enterprise raises. Some companies never extend beyond seed funding into Series A rounds or beyond. To get seed funding, it is really about networking as well as selling the dream and team. Seed funding helps a company to finance its first steps, including things like market research and product development. With seed funding, a company has assistance in determining what its final products will be and who its target demographic is. Seed funding is used to employ a founding team to complete these tasks. There are many potential investors in a seed funding situation, one of the most common types of investors participating in seed funding is a so-called “angel investor.” Angel investors tend to appreciate riskier ventures (such as startups with little by way of a proven track record so far) and expect an equity stake in the company in exchange for their investment. Accelerators like YCombinator, TechStars and Micro VCs such as First round Capital also invest seed funding as well. While seed funding rounds vary significantly in terms of the amount of capital they generate for a new company, it’s not uncommon for these rounds to produce anywhere from $10,000 up to $2 million for the startup in question.

- Series A funding – once a business has developed a track record (an established user base, consistent revenue figures, or some other key performance indicator), that company may opt for Series A funding in order to further optimize its user base and product offerings. Opportunities may be taken to scale the product across different markets. According to Fundz, the term “Series A” refers to the class of Convertible Preferred Stock sold to investors in exchange for their investment. In this round, it’s important to have a plan for developing a business model that will generate long-term profit. Oftentimes, seed startups have great ideas that generate a substantial amount of enthusiastic users, but the company doesn’t know how it will monetize the business. Typically, Series A rounds raise approximately $2 million to $15 million, but this number has increased on average due to high tech industry valuations, or unicorns. The average Series A funding as of 2020 is $15.6 million. at this stage investors are looking for companies with great ideas as well as a strong strategy for turning that idea into a successful, money-making business. The investors involved in the Series A round come from more traditional venture capital firms. Some of the biggest Series A investors in software startups include Accel, 500 Startups, Bessemer Venture Partners, Andreessen Horowitz and Greycroft Partners.

- Series B Funding – are all about taking businesses to the next level, past the development stage. Investors help startups get there by expanding market reach. Companies that have gone through seed and Series A funding rounds have already developed substantial user bases and have proven to investors that they are prepared for success on a larger scale. Series B funding is used to grow the company so that it can meet these levels of demand or to pour the gas on for growth with a larger investment round. Building a winning product and growing a team requires quality talent acquisition. Bulking up on business development, sales, advertising, tech, support, and employees costs a firm a few pennies. The average estimated capital raised in a Series B round is $33 million. Companies undergoing a Series B funding round are well-established, and their valuations tend to reflect that; most Series B companies have valuations between around $30 million and $60 million, with an average of $58 million. Oftentimes the Series B is led by many of the same VC investors of the earlier round.

- Series C Funding – rounds generally take place to make the startup more appealing for acquisition or to support an IPO listing. This is the first of what are called “later-stage” investments. This can continue into Series D funding, Series E funding, Series F funding, Series G funding, private equity funding rounds, etc. While there is a lot of capital ready, a lot of companies don’t even make it to Series C. The reason for this is because Series C investors are looking for breakout companies that have already demonstrated significant traction. In Series C rounds, investors inject capital into the meat of successful businesses, in an effort to receive more than double that amount back. As a funded startup’s operation gets less risky, more investors come to play. In Series C, groups such as hedge funds, investment banks, private equity firms, and large secondary market groups accompany the type of investors mentioned above. Most commonly, a company will end its external equity funding with Series C. However, some companies can go on to Series D and even Series E rounds of funding as well. Thus, the deal size of Series C funding rounds has continued to increase. According to Fundz data, Average Series C Funding Amount: An analysis of 14 Series C deals in the U.S. in June, 2020 showed the mean Series C round to be $59 million; the median was $52.5 million. Many of these startup companies utilize Series C funding to help boost their valuation in anticipation of an IPO.

Venture Debt/Debt Financing – While this article focuses on fundraising, it’s important to note that some startups may prefer other funding routes. Opening a line of credit at a credit union or bank is one way of accessing large amounts of capital without giving up a stake in the business to a board of investors. Financial institutions always required GAAP financials as a means of managing risk. The trade off for venture debt? Higher interest rates. If you have ever watched an episode of CNBC’s SharkTank, Kevin O’leary aka “Mr Wonderful” will sometimes propose this option to some of the startups that come on their show. Mr O’leary tweeted back in 2016 “Sometimes venture debt is a better option than an equity deal… but NOTE: venture debt is NOT the same as credit card debt! “

Venture Debt/Debt Financing – While this article focuses on fundraising, it’s important to note that some startups may prefer other funding routes. Opening a line of credit at a credit union or bank is one way of accessing large amounts of capital without giving up a stake in the business to a board of investors. Financial institutions always required GAAP financials as a means of managing risk. The trade off for venture debt? Higher interest rates. If you have ever watched an episode of CNBC’s SharkTank, Kevin O’leary aka “Mr Wonderful” will sometimes propose this option to some of the startups that come on their show. Mr O’leary tweeted back in 2016 “Sometimes venture debt is a better option than an equity deal… but NOTE: venture debt is NOT the same as credit card debt! “

What to expect while fundraising in 2021 and beyond

Over the past of 2020 and into 2021, the pandemic forced people to dramatically change how they work and interact with colleagues and clients. When the pandemic finally subsides and more people are vaccinated, in-person meetings and gathering back at the office will definitely resume, but it’s safe to say the old ways of networking and fundraising won’t shift back 100%. Both startup founders and VCs alike have had to work through the ups and downs of remote networking and fundraising interactions and there are definitely some lessons and best practices as takeaways for the future.

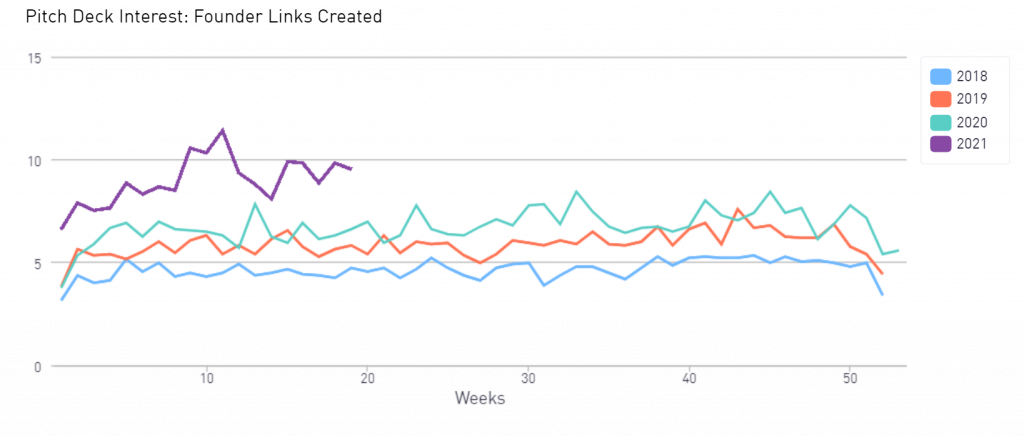

Russ Heddleston the CEO of Docsend, a secure document sharing platform, that just got acquired by Dropbox recently published a resource titled 2021 DocSend Startup Index: Pitch Deck Interest that is tracking VC interest for receiving pitch decks from startups by using analyzing three key metrics using the DocSend Startup Index in 2020-2021. The tracked metrics included:

- The amount of pitch decks potential investors are reviewing

- How long they’re spending reading those decks

- How many pitch decks founders are sending out

(Image credit: Docsend Startup Index)

(Image credit: Docsend Startup Index)

As of May 17th, 2021 the report found that all three Pitch Deck Interest metrics fell slightly last week. Investor activity was down 2.2% but VC demand remains high overall, especially relative to previous years: investor activity is up 38.34% over last year at this time and 71.15% over the same time in 2019. Investors ae still readily examining pitch decks for potential deals, and as the economy continues reopening we can expect this optimism to remain high for the time being. VC time spent on pitch decks was virtually unchanged last week, decreasing by just 0.73%.

Founders, for their part, were also slightly less active: they sent out 3.45% less pitch deck links on average. Despite this dip, though, founder activity has been relatively stable since mid-April (with the exception of one week). We continue to see sustained optimism in the fundraising marketplace, and small dips shouldn’t take our attention away from just how robust both deck supply and investor demand are right now.

How will pitching and networking Change?

Mr Heddlesson gives some of his insights in the TechCrunch white paper starting with in-person vs virtual (phone, video etc). He said “is traveling to a conference the best way for a founder to have a chance at meeting the VC who is right to support their business?

Will a VC want to drive an hour through Bay Area traffic for an in-person status update meeting on their latest investment? Zoom fatigue aside, video conference calls do have some benefits — efficiency, no travel time — although not all meetings are best conducted virtually.”

He also suggested that the extent to which businesses go in-person or stick to virtual meetings could depend directly on what round of fundraising they are working toward or have completed. Businesses in the pre-seed round might stick with more Zoom meetings in order to conserve resources. Going forward pre-seed startup companies will need to withstand more scrutiny, demonstrate more product readiness, and show a clear competitive edge.

Mr Heddlesson also speculates that founders in the seed round will likely split between video and in-person meetings as they are under pressure to show traction in this round, as they found in their report on seed fundraising, yet will also need to conserve resources and time.

For Series A, they might have to meet less in person because they have established relationships with their investors. Series B might see more in-person meetings as their business has reached a level of complexity that is difficult to communicate via a deck or video conference.

The funding divide may grow wider for startups outside Silicon Valley

When the pandemic struck, founders suddenly operated on a more level playing field when it came to connecting and networking with VCs outside of their region. With video conferencing and online networking widely accessible, barriers based on geographic location were knocked down. However, as in-person events might fill our calendars once again in the 2nd half of 2021, founders outside of VC hotspots like Silicon Valley and New York might find themselves at a disadvantage once again.

Key industry sectors driven by tech will prevail and grow

While the pandemic had shut down a number specific industries, such as in-person entertainment, hospitality and travel, COVID-19 has reinvigorated other industries as the demand for products and services has shifted. Consumer tech products and enterprise tech have seen surges in demand as people have been (and some still are) working from home and also finding new ways to stay entertained and connected with friends and family.

The Docsend Startup Index data shows an increase of pitch decks being sent to potential investors in the areas of digital health, remote wellness, clean tech and energy, so we anticipate those sectors will continue to see more growth and opportunity.

Even with vaccines being steadily rolled out as of mid May 2021, we still don’t know when the US will reach herd immunity or when every adult will be vaccinated, so Mr heddlesson is guessing that we’ll we still see demand demand for products and services in these areas, adding fuel to startup activity.

Four tips for fundraising success in 2021

Four tips for fundraising success in 2021

Mr Heddlesson had a few final tips for fundraising and pitching investors regardless of what the summer and 2nd half of 2021 end up being like as far as normalizing and getting back to business.

Continue to network

Find people to meet. Networking can not only help you get connected to the right VC, but you never know what you’ll learn or who you’ll meet. It’s always helpful to expand your circle of contacts, as well as your knowledge base.

Find mentorship

Recognize that serendipity isn’t everything, and you need to continue to make those connections. Keeping the right people in your corner is always a good strategy. Not just for the fundraising phase of your business, but for guidance in managing the business to its next stage of success (or if you’re not successful, knowing when to move on).

Take advantage of both the virtual and physical world

Be prepared to continue to connect with potential investors online, use Zoom for meetings, share your pitch deck online and adopt virtual data rooms to facilitate due diligence. At the same time, be ready to take advantage of opportunities to meet with your VCs and investors in person and attend special-purpose VC networking events with clear agendas when it becomes safe again and as it makes sense for where you are with your fundraising journey.

Remember that fundraising is hard

Keep in mind fundraising is going to take longer than normal. Despite being in this new normal Covid-19 fundraising landscape for a while, we are all still learning to adapt. Be cognizant of how much time you will need to get through this process. Also, if you find one great investor, don’t beat yourself up if you don’t get five competing offers for funding. Focus on the win and move forward.

How investors use financial reports to assess risk

When meeting with investors, it’s important they are on board with your product or idea you are trying to build or problem to solve. If they can see you’re also passionate about getting into the financial details, then it will really set you apart as an investment opportunity.

Your propensity to drive an ROI-focused business will be tested as they dig into different financial ratios. Here are a couple of figures worth focusing on and what they’ll tell investors about your business:

Lead with asset to liabilities ratio analysis

Investors will compare your long term liabilities to the business’s equity. You should be able to access and present this information from both columns in your balance sheet. From here you can also show investors how wise you are at allocating your resources and spending with a plan for return. Use your balance sheet once again to determine your Return on Assets (the higher, the better here):

Return on Assets = Net Income/Average Total Assets

Now, determining a desired outcome for your return on assets can be tricky and somewhat arbitrary for early stage startups. Basically, if you’re a growing tech software startup company, this number may seem low. Don’t be discouraged, just be aware that questions may arise and use that knowledge to prepare to justify your spending. Investors and venture capitalists want to have as much financial knowledge about your company as possible when evaluating the opportunity. After all, they are most interested in their profitability, how they can diminish their risks, and the ultimate return of your business as an investment.

Use your burn rate and cash runway to explain your fundraising timeline

I have written about this subject previously. A “Cash Burn Rate” refers to the change in the amount of cash a company has over a specific period of time (typically a month). For example, if a company spends $10,000 a month, its burn rate would be $10,000. This goes hand in hand with your cash runway, which is the amount of time your company can survive on its current cash stores at its current average monthly burn rate. If you have $100,000 in the bank and a $10,000 monthly burn rate, your cash runway is ten months.

Cash Runway = Available Cash / Burn Rate

When it comes to seeking investment, startup founder’s use their burn rate to understand how much time a new round of funding will buy. Burn rate can be calculated with or without income factored into the equation. Factoring for income helps business owners understand the long-term viability of their spending habits, while excluding income helps determine a worst-case scenario calculation that tells business owners how long they can survive if all their income streams were suddenly cut off. Having this figure in the back of your mind can help you frame your growth plan and justify the amounts you’re going after— good to have when you’re negotiating with a potential investor.

How to pick an investor in good or bad times

How can entrepreneurs ensure they are picking the right investors for their company? Last year I wrote an article about this subject called “5 red flags your startup should be cautious of when choosing potential investors.”

Choosing the right VC investor is one of the most important decisions startup founders will ever have to make. In good times, the choice can make or break a startup. When times are bad, it’s even more likely that the wrong VC partner could be the catalyst that starts a downward spiral. With many funds still looking to make investments before the end of the year and startups are lining up for cash, founders need to know how to find the right investor.

Mike Myer is CEO and founder of Quiq, wrote an article in Techcrunch in December 2020 where he said “It’s not about simply choosing an investor — you are hiring your next boss. The investor should be someone you feel comfortable working with and working for.”

He further explained that “you don’t want an investor who is checked out, but too much focus isn’t good, either. And, you don’t want an investor who is completely agreeable since your best outcome will be driven by a constructively demanding advisor.”

He went into details about his own fundraising experience, that his startup Quig, had received a few different terms sheets from different investors, for his Series B fundraising round. He said the financial terms were close enough, so their selection criteria came down to two important questions:

- How can the investor help the business?

- What’s the risk that the investor will hurt the business?

Mr Myer, said that he ended up going with a specific investor “because they had prior experience as a CEO with a very successful exit.” He added “they had a firsthand understanding of the challenges involved in running a business and would apply that experience to improving our company.”

As opposed to some investors who only have second hand experience gained from being a board member not running a startup themselves.

Personal connections and vibes matter. Mr. Myer feels that if you don’t feel like you hit off or made a personal connection to the investor at the first meeting, then trust your gut and move on.

Mr Myer’s also suggested that a startup founder should also be asking the question: How well does the VC know your market? He also said that “at the beginning of the pandemic, our investors counseled us to prepare for the worst.” We analyzed what could go wrong with the business and made a worst-case plan as our baseline. In March 2020 the famous VC firm Sequoia Capital, sent an email note to its portfolio startup companies founders warning that the risks of the coronavirus outbreak as Black Swan Event could bring a lengthy global economic slowdown and fundamentally alter the current business environment.

In a possible worst-case scenario like COVID, your VC partner’s knowledge of your business and market is absolutely an advantage. A VC firm’s marque reputation, (Bessemer Venture Partners, SV Angel, Kleiner Perkins, Andreessen Horowitz, Greycroft Partners, etc) is often considered by founders to be the most important factor in their choice of an investor, but Mr Myer’s also considers market knowledge and personality to be also important qualities to think about when choosing a VC partner.

Do your research about what the is VC firm’s investing “sweet spot” or niche

Some VCs are great partners to early-stage companies while others may be best tapped in later stages. Founders should ask:

- What size company do they invest in?

- How much do they typically invest?

- What percentage of ownership do they expect?

If the size of your company and the round isn’t close to the bullseye of the investor’s target model, move on.

Ultimately at the end of the day, investors put money into businesses they understand and founders they trust and respect, but founders need to figure out how to build that trust and respect.

To foster a relationship that could lead to an investment, keep VCs in the loop by sending periodic progress updates regarding deliverables and milestones achieved and personally interact at least twice a year (these days that means a Zoom call most likely.)

Similar to how successful sales or biz dev professionals keep detailed notes about each of their prospects, founders need to keep track of their potential investors. If an investor mentions she was touring colleges with her son on one call, make a note to ask how college is going on the next call.

Mr. Myer’s final word of advice is that entrepreneurs should only spend time with those who react positively and show an interest. Founders need to leverage their network — research investors to see if they share a network connection and ask their connection in common to casually drop a good word about your startup. Be simultaneously ruthless and considerate at being front of mind with their potential investors.

Decoding Investor Questions — What They Really Mean and How You Can Respond

Angel and VC investors are a diverse group of innovators and changemakers. They do, however, have one thing in common: They’re inquisitive. Investors always have questions, but what do they really want to know? Get behind the subtext of each common question and the best way to answer. The Indinero ebook shared a list of investor typical questions, what they mean, and how to respond.

What’s your story?

Translation: Why should an investor care about your company? This basic line of reasoning should inform every fundraising decision you make, starting with the first sentences you use to introduce yourself and your startup. Effective investment seekers understand the rules of storytelling: compelling characters, high stakes, and a clear beginning, middle, and end. Remember that people are more memorable than ideas, so focus on the details and put your founders and customers at the forefront.

How are you improving your customers’ lives?

Translation: Beyond initial market buzz and popular sentiment around your brand, can you explain the ways your company makes a difference to your customers or community at large? This question speaks to your company’s traction among consumers, and ultimately the depth and scope of your vision. Investors need to know that you are a) familiar with and understand the audience you’re selling to, b) putting your customers’ needs first, and c) committed to solving a problem rather than cashing in on an opportunity.

Why does your company need funding, and why now?

Translation: Why are you turning to outside investors rather than taking out a loan or bootstrapping? Do you need money to harness momentum and seize an opening or merely to stay afloat? This is your chance to demonstrate that you understand an investor’s perspective and have thought long and hard about what someone has to gain from helping fund your company. Timing is critical as well. Assess what, if anything, a potential investor has to lose from not backing your company right now.

Who else out there is doing this, and how are you doing it better?

Translation: Who are your competitors, peers, collaborators, and role models? What are you bringing to the table that they don’t—and ieally, can’t—already provide? Take a close look at your product and service offerings, your technological capabilities, and the extraordinary talent on your team. These are your differentiating factors; hone them and incorporate them into the core of your story and value proposition.

What am I paying for?

Translation: What do you plan to give an investor in exchange for their check? It sounds like a simple question, but the “right” answers vary wildly. It sounds like a simple question, but the “right” answers vary wildly. Some investors are looking for startups they can steer to profitability and want to become stakeholders and decision makers. Others would rather take a hands-off approach and just put their money behind companies they think will make it big.

Some may be interested in buying or licensing your intellectual property. Again, think about how all these different types would evaluate your company, and lead your conversation with whatever pieces would represent the highest value to them. Don’t forget to do your research!

How soon will I see returns?

Translation: Can you connect this investment to revenue generation? Investors expect to earn a return on investment (ROI), but they also understand that some investments take longer to pan out than others. The magnitude of that ROI is key here. A longer wait for a bigger payoff may speak to them, but other investors could be the opposite—looking for a short-term loan with quicker returns for maybe fewer margins.

This is why it’s important for you to be absolutely realistic here. Don’t over promise investors and under deliver on the return timeline or size. They’ll see through that. Instead, come prepared to these meetings with projections for your company’s financial future, along with a record of past performance.

Where do you plan to take the company in a year? In five years?

Translation: How aggressive are you? Does your dream resonate with me? Are we aligned in what we value? This classic question tells someone scores about your business and personality. Your response indicates the extent to which you’ve thought about the future, as well as how realistic your ambitions are.

Whenever possible, identify milestones and present numbers. You need to tell an investor you not only know what you want to do but that you’ve designed a game plan to achieve it.

Why am I the right person to invest in your company?

Translation: Did you do your homework on who I am?… This is a great time to stroke the ego. What makes the investor you’re speaking to the perfect partner for your company? What drew you to this person or group in the first place?

Maybe the investor in question isn’t your first (or even 3rd) choice, but they should feel like your presentation was tailor-made for them. Do your due diligence, know what sets your target apart, and help them connect the dots.

Conclusion

At the end of the day, investors want to be part of success stories. A huge part of earning that trust comes from setting the initial tone with an honest, transparent impression of your business. The journey to finding your perfect investor or board of investors can feel long and tiresome, but the beauty is that after that mutual vetting runs its course you will know you found the right fit. If you stay focused on the priorities that mean the most to you and your investors the pieces should naturally fall into place.

According to Chris Myers, 90 percent of small businesses are unable to produce dependable financial statements when prompted. Whether that surprises you or not, it does present a pretty enticing way to differentiate yourself from other startups out there competing for venture capital.

Taking funding from investors means ceding some control over your startup, and committing to hyper-growth, transparency, and accountability. Owning early finance tasks and developing accounting hygiene is a great way to understand the numbers that will drive your business as you start to grow and scale.

Thomas Huckabee CPA offers outsourced CFO, tax and accounting services to startups and small businesses. Our firm uses cloud-based accounting software to help business owners understand their company’s financial health, review key metrics, and avoid compliance issues.

If you own a startup and have any questions about taxes or accounting issues feel free to reach out. Huckabee CPA offers free consultations.