I have written several articles about the startup process of pitching investors to raise Seed Capital or Series A, or VC funding, but not all small businesses or startups are a fit for venture capital or angel investor funding models. So as a startup founder you should ask yourself before beginning on a fundraising journey, “Why am I trying to raise money and what ambition am I trying to achieve?”

Because like it or not, a lot of the narrative on fund raising is driven by venture capital money. So, if you are competing for that, then you need to be prepared for the ride of building a VC style business. And also do a reality check. Does the company fit the profile of a typical VC style business or one that an angel investor would be interested in writing a check to. Recently I came across a website called Pitching Angels, that gives fundraising advice from the perspective of an Angel Investor named DC Palter. He wrote several useful articles, but one titled “How to Fund a Startup If It Isn’t a Rocketship” I found one particularly interesting, because he does not sugarcoat what investors are looking for or expecting when they make an investment into a company. And the article starts out by Mr Palter saying “somewhere around 2/3 of the startups I work with are building a business that isn’t suitable for venture investment.”

The article goes to further explain that the venture model is pretty simple and relatively straightforward— investors put in cash in exchange for a cut of the payout when the company is acquired or goes public. Since venture investors get nothing until the exit, no surprise that’s their only goal. And since startups are valued by revenues and revenue growth rates, accepting venture investor capital funding is a promise to focus exclusively on explosive revenue growth.

An article published by Vishal Chadda titled “Fund raising 101 for early-stage startups” also explains the VC funding model.

VCs are typically driven by large markets and revenue pools which can lead them to oversized outcomes

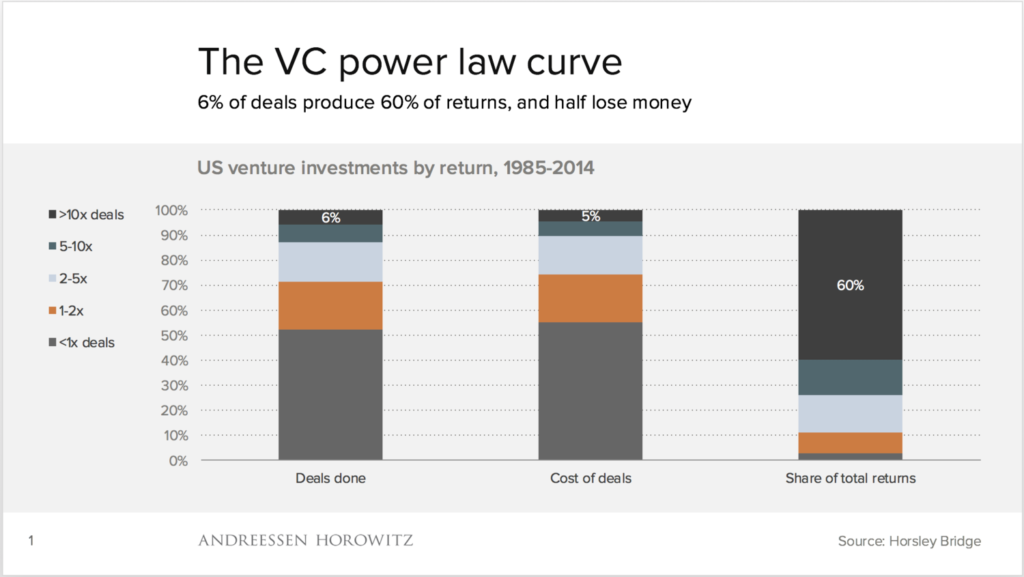

VCs are looking for a winning startup bet that could give a 10x return, that makes up for all the other investments in a fund that don’t pan out, an Angellist article explains more “And the very best early investments offer incredible multiples: Peter Thiel made around $1.1 billion from his half-million dollar early investment in Facebook, a 2,200x return. Grounded in that experience, Thiel is an enthusiastic proponent of venture capital returns being power-law distributed: where the best investments are worth exponentially more than the great investments, which are themselves worth exponentially more than merely good investments.” Abe Othman, Head of Data Science, AngelList Venture

Their potential exit should be meaningful to the overall fund economics. There could be outliers to this definition but the fact is that not every business fits the “VC model”. This venture model works well when your interests are aligned with theirs – the senior team gets paid mostly in equity. When investors get their big payout, you get yours, too. Mr Palter writes “until then, it’s instant noodles and sharing a studio apartment with three roommates.” Venture investing has made some founders outrageously wealthy. But just because you have a great business does not make it a great venture business.

Mr Palter also explains that this model doesn’t work if it’s unlikely to have a 25x acquisition within five years. You may be asking “what does that mean?” He means that that means at an absolute minimum, you’ll need to reach annual revenues of at least $25M; below that threshold, acquisitions are difficult and multiples are low.

In addition to the $25M revenue minimum, there are other reasons your business may not be a great fit for venture capital:

- You don’t intend to sell the business as soon as possible.

- You don’t want to kill yourself for instant noodle wages for the next five years in the hopes of a huge payout later.

- You want to dedicate your efforts to solving a problem instead of focusing exclusively on increasing revenues as fast as possible.

Why Startups Need Projected Revenues Over $25M

In another article by the Pitching Angels author, he states that “startups need projected revenues of at least $25 million by Year 5 for angels to consider investing.“ Like everything else in venture financing, it all comes down to the exit. Until the company is acquired or completes an IPO, the investment has no actual value. It generates no interest, no dividends, no royalties, no rent. That million dollars an investor handed you is nothing but a number on a spreadsheet. Legally, the investor owns a fraction of the business, but since the investor gets no revenue and can’t sell that ownership stake, it’s dead money. So they are usually hoping for an acquisition or IPO as soon as possible, and at a high multiple of what they paid. Now this is not always the case as a Bloomberg Opinion article states ”companies have more access to private capital than ever before, and many are putting off the scrutiny of public markets for as long as possible.” Take Uber, for example which was founded in 2009 and did not finally IPO until 2018.

Now Mr Palter explains that “the usual investment timeframe for venture financing is 5 years. In other words, you need to plan for an acquisition or IPO within 5 years to be an attractive investment. The Social Media startup Snapchat Inc was founded in 2011 but did not go public until March of 2017, so roughly about 6 years for the founders and investors to get a liquidity event and cashout. An article by Kruze Consulting explains that a VC’s return expectations will vary depending on the stage of investment?

Now I’m sure you have heard about these new ways companies can go public besides the traditional IPO route, which is Direct Listings and now what is called a SPAC. An IPO is an outrageously expensive and disruptive process, and once the company is public, there are large, on-going costs associated with being a public company. As a rule of thumb, $100 million in annual revenues is the bare minimum to go public. If you’re not expecting revenues of $100M within 5 years, then an IPO is not a feasible exit.

If you’re projecting less than $100M, the question then is who will acquire the business?

In almost all cases, it’s a large, publicly traded company. The giants have the cash to make acquisitions (and their stock is the equivalent of cash since unlike a private company, it can be freely bought and sold.) Many incumbent giants struggle with innovation, but need growth to support their stock price. Further, if your startup is doing well, you’re starting to steal their customers and they have to respond somehow. Think how Facebook chose to buy their competitors Instagram and Whatsapp to keep its market share dominance and roll these technologies and existing users/ customers into their company.

They may have even tried to build a competing functionality and floundered badly. But they have a huge customer base, a worldwide sales team, a network of distributors and retailers that reach every customer, and a marketing department that’s larger than your entire company. They can increase sales of your product by 10x simply by making it one of their own. They have the cash, the need, and the financial incentive to acquire your business. So the plan of almost every startup is that after a few years to be acquired by one of the giants. At least, that’s the plan. Simple, right?

Mr Palter explains that this is where things can get complicated. You develop a great new product. Your customers love it. You generate $5 million in revenue. Time for Google or Microsoft to acquire the business? Unfortunately, not.

For large corporations to do an acquisition, even a small one, it’s a major undertaking. The diligence process costs millions in legal fees and eats up executives’ time. Once a deal is consummated, integrating your business is a huge distraction across many different departments. If they can turn your $5M business into a $20M business, that seems like a big win but it isn’t. It takes almost the same amount of time and effort to do a $100M deal as a $10M deal, so that’s what the M&A team will focus on.

Typically an M&A team can only do a few acquisitions per year. The bigger acquisitions move the needle financially; the little ones don’t. And let’s not ignore the ego factor—the billion dollar blockbuster acquisition lands the CEO on the front page of the Wall Street Journal where he’s declared a visionary transforming your industry. The $5M acquisition is too small to even disclose in the company’s financial documents. In most industries, $25M is the borderline where your startup becomes interesting to acquirers. Think about the news headlines that came when Salesforce announced its purchase of Slack for $27.7 billion, which they did to compete with Microsoft Teams and enterprise customers.

In addition, $25M is a key metric in a few other ways:

- At $25M revenue growing at 2x per year, it’s easy to see the business quickly reaching $100M.

- The product has been proven useful to a wide audience beyond a small niche.

- The product has reached a level of maturity and stability well beyond beta or MVP and is ready for the big stage. Big holes in functionality have been filled, glitches fixed, suppliers locked in, manufacturing kinks worked out. The software architecture has been rebuilt at least twice for scalability and maintainability, and the back-end infrastructure which used to be held together with duct tape is solid now. You have a QA process and a testing regiment to ensure the software works.

- The company has a full team of executives and employees who can keep the operations running after the founders leave.

In other words, at $25M, you’ve got the type of operation that a big company knows how to integrate without flailing around trying to finish building a half-baked software product. Mr Palter’s final thoughts are that while $25M is a good rule of thumb, the actual minimum depends on the industry. For consumer products, the threshold is $50M while for pharmaceuticals, acquisition is a function of regulatory stage and efficacy data rather than customer revenues.

While angel investors will invest in any business that has a lucrative exit, VCs have their own constraints that require revenues of at least $100M. As an example say a VC fund invests 5 million into a startup and buys 10% of the business (in equity) that sets a minimum valuation of $50M. If they target a minimum of 20x return for an early stage investment, the company needs to be acquired at exit for at least $1B. To get to a billion dollar acquisition, the company needs to have at least $100M of revenue and growing quickly towards $250M.

Scalability / High Operating Leverage

An article published in Toptal, explains that good venture investors are looking for startups that grow exponentially with diminishing marginal costs, wherein the costs of producing additional units continually shrink. The operating leverage effects of this allows companies to scale quicker, more customers can be taken on for little to no operational change, and the increased cash flows can be harvested back into investing for even more growth. How would an investor access this on Day 0? Steve Blank provides a strong definition of a scalable startup:

An article published in Toptal, explains that good venture investors are looking for startups that grow exponentially with diminishing marginal costs, wherein the costs of producing additional units continually shrink. The operating leverage effects of this allows companies to scale quicker, more customers can be taken on for little to no operational change, and the increased cash flows can be harvested back into investing for even more growth. How would an investor access this on Day 0? Steve Blank provides a strong definition of a scalable startup:

“A scalable startup is designed by intent from day one to become a large company. The founders believe they have a big idea—one that can grow to $100 million or more in annual revenue—by either disrupting an existing market and taking customers from existing companies or creating a new market. Scalable startups aim to provide an obscene return to their founders and investors using all available outside resources”

The Toptal article also brings up Tesla and how they decided to open source its patents. This was not intended as a solely benevolent gesture by Elon Musk; instead, it was an attempt by him to accelerate innovation within the electric car space by encouraging external parties to innovate in his arena. More efforts to produce better technology (i.e., longer life batteries) will ultimately help Tesla to reduce its marginal costs faster.

The importance of operating leverage is one of the main reasons, amongst others, why venture capitalists often focus on technology companies. These tend to scale faster and more easily than companies who do not rely on technology.

VCs will look at the timing of startups as part of their investment process

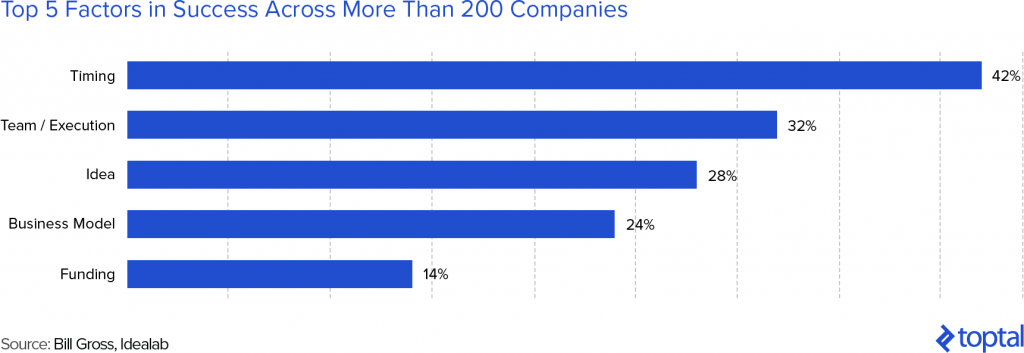

(image credit:Toptal)

Bill Gross of Idealab concluded that timing accounted for 42% of the difference between success and failure. This was the most critical element from his study, which also accounted for team, idea, business model, and funding. In a Ted Talk he explained that “Airbnb was famously passed on by many smart investors because people thought, No one’s going to rent out a space in their home to a stranger. Of course, people proved that wrong. But one of the reasons it succeeded, aside from a good business model, a good idea, great execution, is the timing.”

Using the 2009 recession at the time to frame this, he stated “this was at a time when people really needed extra money, and that maybe, helped people overcome their objection to rent out their own home to a stranger. “

So as part of a VC’s due diligence, they think about “is the deal arriving at the optimal time and is this business model riding a macroeconomic or cultural wave?” The investors in Airbnb will have had the vision to frame this investment away from the prevailing biases of the time and view it as a unique opportunity arriving at the perfect moment. Those that passed on Airbnb may have been thinking within existing paradigms of “accommodation”, with their heart set on finding another Expedia.

Conclusion

So if are building a startup that has a product, that can’t be built without dozens of developers, and requires a large sales team and millions in advertising to reach the target audience, but will eventually generate hundreds of millions (or billions) in revenues, then keep pushing forward, and work on your pitch deck and engaging with VCs. And just to be clear I am not discouraging anyone from pitching VCs, since venture capital is a game of home runs not averages because to the VC firm:

- Failed investments don’t matter (many of the startups won’t make it)

- Every investment you make needs to have the potential to be a home run

The Kruze Accounting article mentions that often VC firms will do big portfolios of startups and 20 to 100 investments in a given venture capital fund. So they know that two or three are going to power most of the returns of the entire portfolio because in the startup world the power law is, the big ones win big. Think about Uber, Facebook, Google. Those types of companies bring the returns to their fund. The fund returns with 10X or 15X all because of, or mostly because of that “homerun” investment.

Finally, while some businesses may not be the typical venture type, they could still be perfectly sound and profitable, giving great satisfaction to the founders and also creating decent long-term wealth along the way for stakeholders. Just because they aren’t VC funded doesn’t make the achievement any less. But if in your heart of hearts you know you have a fantastic product or service for a specialized audience, try to find a way to fund it yourself in the beginning. You’ll save yourself years of stress. You could become CEO of a respected business and an industry leader. And although it may not make you a billionaire, you could eventually become a multi-millionaire and that sounds pretty great to most people.