Rental Real Estate Enterprise = Section 199A “Trade or Business” Safe Harbor Deduction.

Rental Real Estate Enterprise = Section 199A “Trade or Business” Safe Harbor Deduction.

The IRS and the Treasury Department released new guidance and regulations called Notice 2019-07, which details a new “safe harbor” revenue procedure that allows real estate investors that have rental income to be treated as a qualified trade or business eligibility to claim the qualified business income (QBI) deduction (Section 199A deduction).

What is the Section 199A?

The section 199A deduction provides important tax deductions for pass-through entity small business owners and self-employed sole proprietors. When the Tax Cuts and Jobs Act tax reform was passed in December of 2017, a provision was written called Section 199A to give non-corporate business owners a tax deduction of a much as 20% of qualified business income (QBI) from each of the tax-filer’s qualified trades or businesses. The definition of a qualified trade of business is “any trade or business other than a specified service trade, business, or work performed as an employee. Qualified trades or businesses include those operated through partnerships, S-Corps, sole proprietorships (pass-through entities), and dividends from qualified REIT’s or publicly traded partnerships.”

To qualify for the real estate safe harbor, the tax-filer needs to maintain separate records for each rental real estate enterprise, perform at least 250 hours of real estate services as well keeping accurate and contemporaneous records of the performance (below we will dive into the qualifying details further). Eligible taxpayers can also deduct up to 20% of their qualified real estate investment trust (REIT) dividends and publicly traded partnership income. Small business owners that do not make income from owning real estate (do not qualify for the safe harbor) may still be able to qualify for the Section 199A deduction if their business activities meet the definition of a “qualified trade or business”. So do you get income from real estate investments? If so this is important for you to know.

Real Estate and Section 199A

Up until this tax law guidance Notice 2019-07 was released, there had been uncertainty around how real estate professionals and specifically rental real estate investing businesses could qualify as a trade or business for the Section 199A purposes. The Notice 2019-07 gives a safe harbor and more clarity. Taxpayers may rely on this safe harbor for tax years ending after December 31, 2017. So the 2018 tax filing year coming up is eligible.

The Safe Harbor Provision

![]() The safe harbor provision ruling clarifies the qualifying process for rental real estate investors to take advantage of the 20% QBI deduction. Previously the Trump Tax reform law stated that income that comes from a “trade or business” qualifies for the 20% write-off. But because the TCJA was drafted so quickly, some things were not so clear for tax advisors who have clients that own rental real estate, such as determining which rental properties were just investments and which could actually be considered a business enterprise. So now San Diego real estate investors have the guidance rules to be able to take advantage of the 20% deduction by spending at least 250 hours per year (mentioned earlier) on maintaining and repairing property, collecting rent, paying expenses and conducting other typical landlord activities. For the rental real estate enterprise to qualify for the safe harbor and be treated as Section 199A eligible trade or business, it must comply with these 3 rules:

The safe harbor provision ruling clarifies the qualifying process for rental real estate investors to take advantage of the 20% QBI deduction. Previously the Trump Tax reform law stated that income that comes from a “trade or business” qualifies for the 20% write-off. But because the TCJA was drafted so quickly, some things were not so clear for tax advisors who have clients that own rental real estate, such as determining which rental properties were just investments and which could actually be considered a business enterprise. So now San Diego real estate investors have the guidance rules to be able to take advantage of the 20% deduction by spending at least 250 hours per year (mentioned earlier) on maintaining and repairing property, collecting rent, paying expenses and conducting other typical landlord activities. For the rental real estate enterprise to qualify for the safe harbor and be treated as Section 199A eligible trade or business, it must comply with these 3 rules:

- The taxpayer maintains separate books and records for each rental real estate enterprise to reflect income and expenses;

- 250-hour requirement:

- For tax years beginning before January 1, 2023, the taxpayer must perform at least 250 hours of rental real estate services (defined below) each year

- For tax years beginning after December 31, 2022, the taxpayer must perform at least 250 hours of rental real estate services (defined below) in three of five consecutive years ending with the current taxable year; and

- The taxpayer must maintain contemporaneous records of: 1) hours of service, 2) descriptions of the service, 3) dates of service, and 4) identification of those that performed the service. (Note: this third requirement will only apply to tax years beginning on or after January 1, 2019).

So by definition a rental real estate organization, has interest in real property which is held for rent, and solely for qualifying for the safe harbor, may consist of an interest in multiple properties. The caveat is, that the taxpayer must either treat each property as its own separate enterprise or then treat all similar properties as one single enterprise. But the taxpayer is not allowed to commingle or mix residential and commercial real estate within the same enterprise.

More on Rental Services

Notice 2019-07 also clarifies that rental services can include:

- advertising to rent or lease real estate,

- negotiating and executing leases,

- verifying information in prospective tenant applications

- rent collection

- daily maintenance, operation, and repair

- supervision of employees and independent contractors.

These types of services can be done or performed by the owner, owners agent or employee. However financial or investment management activities are included in the rental services with the safe harbor provision.

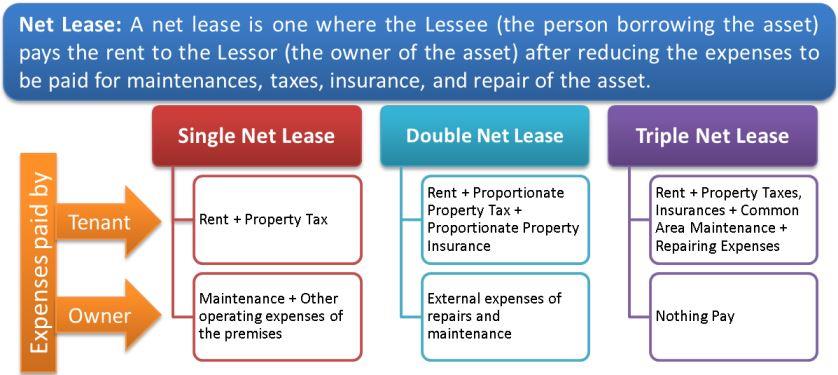

Triple Net Leases

So the Notice 2019-07 gives guidance on triple-net leases, which is real estate that is leased or rented under a triple net lease is not eligible or to qualify for the safe harbor. Triple net lease rentals are not considered “a trade or business.” for qualifying purposes. A triple net lease consists of a lease agreement that makes the tenants or lessees pay the taxes, maintenance and insurance, in addition to rent and utilities. This type of agreement is used in commercial real estate when landlords and investors want a steady stream of income. Leon LaBrecque, an advisor and CPA with Sequoia Financial Group, noted “investors in a triple-net lease will now have to reform their lease agreement or lose the 20% deduction. We’re wondering if large triple-net portfolios might be better off in a private REIT.” Also, another thing worth mentioning if you use the real estate as your personal residence at any part of the year then it disqualifies it from safe harbor eligibility deduction.

Takeaways

- Taxpayers can rely on the safe harbor until a final revenue procedure is issued.

- The safe harbor is strictly limited to the application of section 199A

- Although the safe harbor applies solely for purposes of section 199A, clients should be reminded that treating rental properties as a trade or business may require filing Form 1099 to report rental expenses and treating mortgage interest as business interest expense subject to the new limitations on the business interest expense deduction.

Conclusion

One final qualifying requirement for real estate investors wanting to get the safe harbor 20% deduction is that the taxpayer must include a signed statement with the tax return stating that all of the requirements have been met. The taxpayer or an authorized representative can sign it, but they must have personal knowledge of the specific facts and circumstances.

Thomas Huckabee, CPA of San Diego, California recognizes that many options exist when it comes to choosing the right CPA. And, the right CPA is essential and needed to guide your business through all the new legislation that has been introduced. Operating a full-service accounting firm, Tom also guides clients through the complicated process of how Section 199A ramifications affect your business and tax obligations. Are you a California real estate investor? Contact us for a free consultation to ensure your eligibility for and satisfaction of the safe harbor requirements.

</a

</a