People sometimes ask the question, “how long does it take for a startup to become profitable?” There is no exact answer to this question. What kind of business is it? Is it a small business or a venture-backed software app technology startup? An INC Mag contributor Hillel Fuld wrote that “there is an ongoing debate about early profitability and many have called the tech world a bubble because so many “successful” companies are losing money. But that’s a common misconception as it’s totally reasonable to lose money as you build your startup.”

Is it a good idea for all types of startups to focus on growth instead of profitability?

A Forbes Contributor Abdo Riani wrote an article in 2021 about this topic, mentioning the famous example of how Jeff Bezos was running Amazon with ever-growing revenues and zero profits for decades has become legendary in the tech world. The market of businesses that have very low marginal costs (the cost of adding one additional customer) and strong network effects (the offering of the business becomes more valuable the more people participate in it, usually platforms) is a winner-takes-all economy. Think of the rise of food delivery businesses during the pandemic, (Instacart, Grubhub, Doordash, Uber Eats, etc) Where the market leader becomes a monopoly, and direct competitors simply cannot generate enough added value to overcome the accumulated network effects of the leader. If you are a VC-backed startup that is trying to get in front of as many users as possible to gain market share, rapid growth and user expansion are not only desirable but often necessary. If you decide to take it slowly, one step at a time, you are risking that a competitor who is highly capitalized and investing aggressively in growth would surpass you.

Since a lot of startups and their investors realize this, there are plenty of startups that are not only operating with zero profits, but with massive losses in the name of growth and rapid expansion. If you are trying to build a monopoly in a market with strong network effects, this is rational behavior. Some of the world’s largest (and deemed most successful businesses) are not profitable, and others took many years to even see revenue. This doesn’t mean, however, that it is rational for any new business. The Amazons, Squares, Teslas, WeWorks, Ubers, and Airbnbs of the world are few.

Are You a Small Business Instead of a High Growth Startup?

Keep in mind that nowadays the term startup is often used too widely. Not every new business is a startup. On the contrary—most aren’t. As Paul Graham puts it, startup = growth.

For example, an IT consultancy is not a startup—it grows linearly, and because of this, sacrificing profitability for growth doesn’t make a lot of sense. If the IT consultancy were to create a highly scalable digital product (low marginal costs), however, then this is a scalable startup project and investing more aggressively in growth (after product-market fit) makes sense.

If the digital product benefits from strong network effects, however, then investing in growth is not only a good idea, but highly necessary, and then going the VC route to funding the growth is a standard path. Business profitability relies on more than a few factors, including the type of business you own, your operating expenditure, and the strategies you use to grow your business. While it may take time to see real profits, there are steps a small business can take to speed things up.

Does your company have enough cash?

The Forbes article also mentions “if your company is working in a more traditional, competitive market, then sacrificing profitability for fast growth can be dangerous, as it increases your risk exposure. Adverse events on the market can push you over the edge. Moreover, the growth gains you’ve managed to accumulate might not be worthwhile because in the long run they could be overcome by competitors with a better offering.”

In such markets, scale isn’t the only thing that determines success, so it doesn’t make sense to pay a premium to achieve it. It would usually be better to utilize a more conservative financial and marketing strategy. Pete Flint, a General Partner at NFX, a seed-stage investment firm, wrote that “if you’re enduring losses relative to a modest cash position, you don’t have the luxury to heavily invest in growth. Your strategic priority should be to reduce your cash outflow and extend your runway, either by getting to profitability or raising a new round of capital, so you’ll be in a position to respond when the market turns and capital becomes more available.” Even if you don’t feel that you’re in a cash-constrained situation, in an environment of heightened uncertainty, the focus should be on getting to profitability in your unit economics. The last thing you want to be doing is losing money on every transaction.

Profitability can depend on the business type

According to an article published by the bookkeeping firm Bench, your small business will only start making a profit once you’ve paid overhead expenses and taxes. So the less you have to pay to run your business, the quicker you’ll reach profitability.

Think about freelance service providers like graphic designers, virtual assistants, or IT consultants. For these types of businesses, profitability can happen quickly since you aren’t dealing with a lot of overhead.

On the other hand, businesses with high manufacturing costs, commercial spaces, and a handful of employees, can take longer to turn a profit. The same goes for companies in competitive markets or start-ups that spend a lot of money on customer acquisition. For these companies, the expectation is long-term profitability.

Measuring business profitability

Paul Graham, a seed-stage investor, and Y Combinator co-founder explained in 2009 that there’s a big difference between being “ramen profitable,” or netting just enough profit to cover a founder’s basic living expenses, and “corporate profitable,” aka having capital after all expenses, taxes, and salaries are paid. He also stated “in the past, a startup would usually become profitable only after raising and spending quite a lot of money. A company making computer hardware might not become profitable for 5 years, during which they spent $50 million. But when they did they might have revenues of $50 million a year. This kind of profitability means the startup has succeeded.”

To estimate when your small business will actually start making money, you can use a simple formula to find your break-even point analysis. A break-even analysis is a standard part of every business plan, meaning it’s done before the business is even launched. This is the amount of product (or hours of service) you need to sell to cover your expenses. Every sale after that counts as pure profit. Calculate your Break-Even Point with this formula:

Break-even point = Total fixed costs / (Sales price per unit − Variable cost per unit)

The U.S. Department of Commerce recommends this free online calculator to figure out your break-even point.

Here are 4 ways a small business can increase profitability.

- Find ways to reduce overhead – look at every part of your business to find opportunities to lower costs and reduce overhead.

- Focus on selling smarter – keep an eye on monthly revenue trends, to see what is and isn’t working in your business, cross or upselling strategies, raise prices, listen to customer feedback to make improvements.

- Outsource time-consuming tasks – You could spend hours navigating the latest marketing trends, crafting sales emails, or getting in the weeds of financial spreadsheets. Or you can partner with an expert to outsource business bookkeeping, accounting, cash flow forecasting or consult with a part-time CFO to guide you through pivotal moments and crucial decisions.

- When in doubt, pivot – the now-famous enterprise software chat tool Slack (acquired by Salesforce) started out as a different company and pivoted to success. If your product or service isn’t making much headway in the market, it’s always worth trying a different approach or positioning your business in a new market.

How do VCs and Angel investors look at potential businesses?

In early startup days it is common for founders to raise Seed funding, and then a Series A. Typically this will be to assemble the founding team of employees, build out an MVP and start customer acquisition. But how do investors look at a business and decide whether to invest?

Firstly, venture capital is not right for every business. Angel’s and VCs typically will look at businesses with large scaling opportunities. To build out scale, often a lot of investment is required, and more investment that is made usually means profitability is pushed further away. When a VC looks at early-stage investments the most important thing is growth. Admittedly startups with a high burn rate are not attractive for investors either, but they will never continue to fund slow growth.

And most investors are looking to back smart founder-led sustainable revenue startup bets to pour capital into and get a liquidity event exit (IPO, Direct Listing, SPAC, M&A etc) where they will get their money back and a nice profit. It was only a matter of time.

As more tech companies go public, the necessary disclosure has meant that with access to more information on the financial condition of many startups, mainstream investors have begun questioning just how profitable and sustainable these startups actually are.

So ultimately growth vs. profitability is a balancing act throughout the life of a startup. Founders must constantly walk a tightrope between the two as they scale their company.

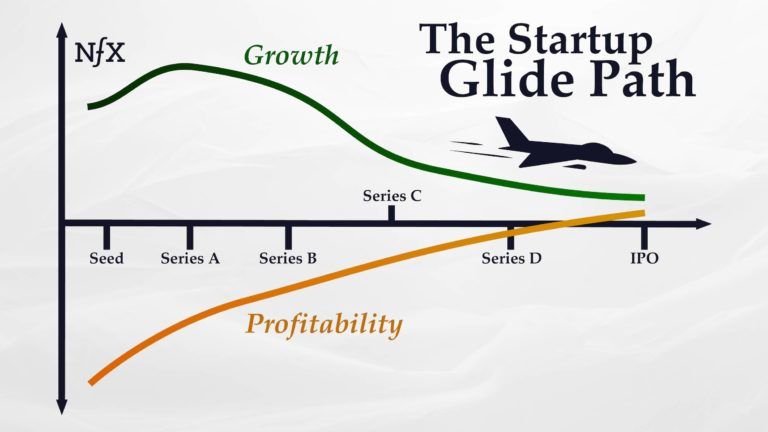

The basic idea is that startups in the early stage should be high growth and the priority is on the unit or cohort profitability economics, not overall company profitability as the company invests in product development and scale. However, they should chart a path “gliding” towards more moderate growth and profitability across the entire business as the business matures and scales.

(image credit: NFX)

(image credit: NFX)

Early Stage (Seed – Series A): Grow Aggressively

Mr. Flint of NFX, explains that if you’re an early-stage startup, you need to be aggressive about growth if you have a strong cash position and fast CAC/LTV payback periods, as mentioned earlier. This is because strong growth is often a key requirement for securing fundraising in the early stages.

So if your startup isn’t fighting for survival because of a downturn, growth is the priority early on. At this stage, it’s about growing rapidly to achieve a certain scale and begin proving out unit economics. There will be time later to more heavily emphasize profitability — although it’s never too early to begin charting a path towards it.

Mr. Flint also states that there are two important metrics to focus on understanding:

- Find product-market fit before spending aggressively on growth. If you’re a seed-stage startup without PMF, you’re likely to be experiencing high churn. Growth is pointless with a leaky bucket. A product needs to be valuable enough to users that it can be retained before paying to acquire customers makes sense.

- Once you have product-market fit, you need 3-5x annual growth. Once you reach this point, demonstrating the ability to scale quickly is mandatory to get to the next stage of funding. You need to show 3-5x+ growth in key metrics for your business: revenue if you’re a SaaS, supply-side users if you’re a 2-Sided Marketplace, businesses or developers building apps if you’re a 2-sided platform, the number of interactions and transactions if you’re a market network, etc.

Even once you have achieved product-market fit as a startup, revenue is rarely emphasized and investors won’t expect profitability if you have sufficient runway. In fact, you as the Founder are often explicitly tasked with not being profitable because, in the vast majority of cases, not spending enough on growth sends the signal to investors that you are not being aggressive enough to capture the market or don’t have a scalable or repeatable plan for how to achieve fast growth.

That being said, none of this means you shouldn’t try to build an efficient business. An efficient model for customer acquisition and understanding your cost of acquiring new customers will help as you grow. Here are some key efficiency indicators that investors look for in an early-stage startup:

Here are some key efficiency indicators that investors look for in an early-stage startup:

- Payback period – The amount of time it takes for a customer’s revenue to pay back their cost of acquisition.

- Retention/churn rate – The lower the churn rate, the better. In the stickiest network effect businesses, churn in the early stages is usually close to zero.

- Business-specific metrics – The efficiency metrics that matter also differ depending on the business model. For example, Net Revenue Retention (NRR) is a key efficiency metric for B2B SaaS, while marketplaces/platforms would focus more on user retention.

- Return on investment – Revenue generated from a sale minus the costs of sales?

Mr. Flint also explains that “the very best companies are able to generate net negative revenue churn, meaning that the expansion in revenue from existing customers exceeds the revenue lost from churned customers.”

For early-stage companies, a singular focus on revenue may not be appropriate as you may be better off building a large number of engaged relationships that are lightly monetized or free where you can expand. It could be strategically important to build out a large number of relationships and ultimately reduce your CAC and strengthen the network.

While profitability remains secondary, having a clear understanding of your unit economics is important, what they are today and what you expect them to be.

Furthermore, every dollar of revenue will be much more valuable if it is recurring with very low churn, paid upfront with a high gross margin, not concentrated on a few customers, and resulting from a business with strong network effects. While not all of these are possible, they are elements that help make Seed and Series A companies more attractive to investors.

Mid-Stage (Series B & C): Create Optionality

In the early stage, growth is paramount. In later stages, profits and efficiency are necessary to show the long-term viability of the business. But in the middle, finding a proper balance is not as obvious. Because of this, creating conditions for optionality enables a startup to control its destiny and ultimate success. The future today for every sector and the economy at large is uncertain, so for scaled businesses options create immense value.

Meaning, find a way such that growth or profitability is a choice and the company’s survival does not depend on which path it chooses or the whims of investors or the market. If capital is available and there is an important strategic or growth opportunity, then you have the option to pursue it, or if you are in a recessionary period, focus on profits to enable you to ride it out and incrementally capture market share.

Founders of early-stage companies should be very aware of this and engineer their customer acquisition and cost structures to give themselves options on how best to capture the opportunity.

One path to optionality is having efficient, scalable customer acquisition. If your efficiency metrics are good by the time you reach the mid-stage, then moving the needle up or down towards either growth or profitability will be relatively easy. It’s simply a matter of the amount of money you are spending to acquire customers.

Late Stage: Gliding Towards an IPO and Greater Profitability

(image credit: Saastr)

For later-stage companies approaching their IPO or another type of liquidity event, growth is still more important than profits. The best case, of course, is when a company is both highly profitable and growing quickly.

In the 2019 IPO class, Zoom and Datadog both fit that description. Zoom, in particular, was growing quickly and showing strong positive free cash flow — a metric that is an even more powerful indicator of profitability than EBITDA. This tends to fit the SaaS profile of business metrics.

Conclusion

In summary, if you decide to sacrifice profits for growth, make sure you’re in the right kind of winner-takes-all market. The pendulum is swinging back to an emphasis on profitability and the environment is forcing companies to focus on efficiency and ingenuity over pure growth.

According to recent reporting from Forbes, a slew of companies that dominated headlines ahead of initial public offerings in the last two years have become some of this year’s biggest stock market losers—exemplifying investors’ growing skepticism toward speculative, and often unprofitable, firms (Peloton, Robinhood, Coinbase etc )as stocks post one of the worst starts to a year ever. If you run a scaling startup and need advisory Huckabee CPA can help you across the board in all areas of accounting financial reporting, and taxation, feel free to contact us for a free consultation.